|

市場調查報告書

商品編碼

2027519

臨床試驗市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Clinical Trials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

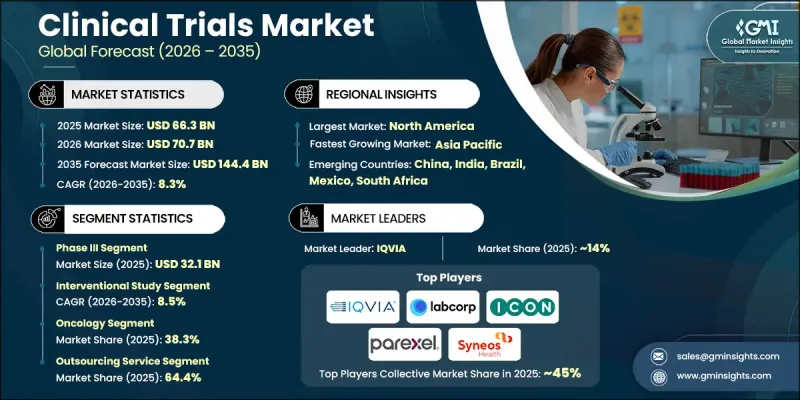

2025年全球臨床試驗市場價值為663億美元,預計到2035年將以8.3%的複合年成長率成長至1,444億美元。

市場成長的促進因素包括慢性疾病和感染疾病的日益普遍、對創新藥物和生技藥品需求的不斷成長,以及製藥和生物技術領域研發投入的持續增加。臨床試驗仍然是藥物研發的關鍵環節,確保所有治療領域新療法的安全性、有效性和監管核准。藥物研發管線的日益複雜化,尤其是在生物製藥、腫瘤學和精準醫療領域,正在推動臨床試驗數量的增加和先進調查方法的應用。同時,數位化工具、分散式試驗模式、人工智慧驅動的分析以及真實世界數據(RWE)整合的日益普及,正在提升受試者招募、數據品質和營運效率,從而增強全球臨床研究生態系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 663億美元 |

| 預測金額 | 1444億美元 |

| 複合年成長率 | 8.3% |

基於研究設計,干預性研究領域預計到2035年將以8.5%的複合年成長率成長,這主要得益於其在監管申報和證據生成中的核心作用。干預性試驗因其前瞻性地分配治療方法並產生可靠、無偏倚的安全性和有效性臨床數據而備受青睞。這些試驗廣泛應用於藥物、生物製藥和醫療設備的研發,並日益融合適應性試驗設計、精準醫療方法和先進的數位化監測技術。電子資料收集(EDC)、遠端監測和人工智慧驅動的分析技術的日益普及,進一步提升了試驗的效率、擴充性和數據完整性,鞏固了干涉性試驗在全球臨床試驗市場的主導地位。

到2025年,腫瘤領域將佔據38.3%的市場佔有率,這主要得益於全球癌症負擔的加重以及人們對抗癌藥物研發日益成長的興趣。癌症發生率的上升、人口老化以及未被滿足的醫療需求不斷湧現,持續推動全球腫瘤研發領域的投資。腫瘤臨床試驗日趨複雜,融合了生物標記、伴隨診斷和精準醫療策略,以實現個人化治療方案。監管方面的利好,包括眾多腫瘤藥物的核准和簡審類,進一步促進了腫瘤臨床試驗的擴展,使其成為臨床試驗市場成長和創新中最具影響力的領域。

預計到2025年,北美臨床試驗市佔率將達到50.7%。這得歸功於先進的研究基礎設施、眾多製藥和生物技術公司的聚集以及完善的法規結構。該地區擁有許多優勢,例如對臨床研究的高度重視、大量合格的臨床實驗研究員以及專業的臨床實驗設施,尤其是在腫瘤和罕見疾病領域。強大的公共資金支持,包括來自美國國立衛生研究院(NIH)的大量投資,以及越來越多的合約研究組織(CRO)外包,正在推動全部區域的穩定成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 影響產業的因素

- 成長促進因素

- 全球慢性病盛行率不斷上升

- 將臨床試驗外包給合約研究組織(CRO)的需求日益成長

- 政府和非政府機構增加對臨床試驗的資助

- 擴大在亞太國家進行臨床試驗的機會

- 產業潛在風險與挑戰

- 保險公司對標準治療的覆蓋範圍不足

- 基礎設施障礙與社會挑戰

- 市場機遇

- 分佈式臨床試驗(DCT)的成長

- 人工智慧與先進分析技術的融合

- 成長促進因素

- 臨床試驗數量分析(基於初步調查)

- 臨床試驗數量分析:依地區分類,2022-2025 年

- 臨床試驗數量分析:依研發階段分類,2022-2025 年

- 臨床試驗數量分析:依適應症分類,2022-2025 年

- 監理情勢(基於初步調查)

- 美國

- 歐洲

- 亞太地區

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 韓國

- 菲律賓

- 臨床試驗-亞太地區優勢(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依階段分類,2022-2035年

- 第一階段

- 第二階段

- 第三階段

- 第四階段

第6章 市場估計與預測:依研究設計分類,2022-2035年

- 干預研究

- 觀察性研究

- 擴展獲取研究

第7章 市場估計與預測:依治療領域分類,2022-2035年

- 自體免疫疾病

- 腫瘤學

- 循環系統

- 感染疾病

- 皮膚科

- 眼科

- 神經病學

- 血液學

- 其他治療領域

第8章 市場估算與預測:依服務類型分類,2022-2035年

- 外包服務

- 內部服務

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 波蘭

- 荷蘭

- 瑞士

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 秘魯

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Cadiya(Clinipace)

- Celerio

- Charles River Laboratories

- ClinChoice

- ICON plc

- IQVIA HOLDINGS

- Labcorp Holding(Covance)

- Medpace

- Parexel International Corporation

- Pharmaceutical Product Development(Thermo Fisher Scientific)

- Qserve

- SGS SA

- Syneos Health

- The Emmes Company

- Veeda

- Worldwide Clinical Trials

- Wuxi AppTec Co.

The Global Clinical Trials Market was valued at USD 66.3 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 144.4 billion by 2035.

Market growth is driven by the rising prevalence of chronic and infectious diseases, increasing demand for innovative drugs and biologics, and sustained growth in pharmaceutical and biotechnology R&D spending. Clinical trials remain a critical component of drug development, ensuring the safety, efficacy, and regulatory approval of new therapies across therapeutic areas. Growing complexity in drug pipelines, particularly in biologics, oncology, and precision medicine, is accelerating trial volumes and driving adoption of advanced trial methodologies. In parallel, the increasing use of digital tools, decentralized trial models, AI-driven analytics, and real-world evidence integration is improving patient recruitment, data quality, and operational efficiency, thereby strengthening the global clinical research ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.3 Billion |

| Forecast Value | $144.4 Billion |

| CAGR | 8.3% |

Based on study design, the interventional study segment will grow at a CAGR of 8.5% through 2035, supported by its central role in regulatory submissions and evidence generation. Interventional trials are widely preferred due to their ability to prospectively assign treatments and generate robust, unbiased clinical data on safety and efficacy. These studies are extensively used across drug, biologic, and medical device development and increasingly incorporate adaptive trial designs, precision medicine approaches, and advanced digital monitoring technologies. The growing use of electronic data capture, remote monitoring, and AI-powered analytics is further enhancing trial efficiency, scalability, and data integrity, reinforcing the dominance of interventional studies within the global clinical trials market.

The oncology segment held 38.3% share in 2025, driven by the rising global cancer burden and increasing focus on cancer drug development. Growing incidence rates, aging populations, and significant unmet clinical needs continue to drive oncology-focused R&D investments worldwide. Oncology trials are becoming more complex, incorporating biomarkers, companion diagnostics, and precision medicine strategies to enable personalized treatment approaches. Regulatory momentum, including a high volume of oncology drug approvals and fast-track designations, further supports the expansion of oncology trials, positioning this segment as the most influential contributor to growth and innovation in the clinical trials market.

North America Clinical Trials Market held 50.7% share in 2025, supported by advanced research infrastructure, a strong concentration of pharmaceutical and biotechnology companies, and a well-established regulatory framework. The region benefits from high awareness of clinical research, access to a large pool of qualified investigators, and the availability of specialized trial sites, particularly for oncology and rare diseases. Strong public funding support, including significant investments from the National Institutes of Health, combined with increasing outsourcing to Contract Research Organizations (CROs), continues to drive steady growth across the region.

Key players operating in the Global Clinical Trials Market include IQVIA Holdings Inc., ICON plc, Laboratory Corporation of America Holdings (Covance Inc.), Charles River Laboratories International, Inc., Parexel International Corporation, Syneos Health, Medpace, SGS SA, WuXi AppTec Co., Ltd., Worldwide Clinical Trials, ClinChoice, Celerion, Veeda, Qserve, The Emmes Company, and Pharmaceutical Product Development (Thermo Fisher Scientific). Companies operating in the Clinical Trials Market are strengthening their market position through strategic outsourcing models, geographic expansion, and technology-driven service innovation. Leading players are investing heavily in decentralized and hybrid trial solutions, leveraging digital platforms, remote patient monitoring, and AI-based analytics to accelerate trial timelines and improve patient engagement. Partnerships and collaborations with pharmaceutical sponsors, biotechnology firms, and academic institutions are widely adopted to expand therapeutic expertise and access diverse patient populations. Additionally, companies are expanding their presence in high-growth regions such as the Asia Pacific to capitalize on cost advantages and faster recruitment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Phase trends

- 2.2.3 Study design trends

- 2.2.4 Therapeutic area trends

- 2.2.5 Service type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases across the globe

- 3.2.1.2 Growing demand for outsourcing clinical trials to CROs

- 3.2.1.3 Rise in government and non-government funding for clinical trials

- 3.2.1.4 Growing opportunities for conducting clinical trials in countries in Asia Pacific

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standard-of-care coverage from insurance providers

- 3.2.2.2 Infrastructural barriers and social hurdles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of decentralized clinical trials (DCTs)

- 3.2.3.2 Integration of artificial intelligence and advanced analytics

- 3.2.1 Growth drivers

- 3.3 Clinical trials volume analysis (Driven by Primary Research)

- 3.3.1 Clinical trials volume analysis, by region, 2022 - 2025

- 3.3.2 Clinical trials volume analysis, by phase of development, 2022 - 2025

- 3.3.3 Clinical trials volume analysis, by indication, 2022 - 2025

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.3.1 Singapore

- 3.4.3.2 Malaysia

- 3.4.3.3 Indonesia

- 3.4.3.4 Thailand

- 3.4.3.5 South Korea

- 3.4.3.6 Philippines

- 3.5 Clinical trials - Asia Pacific advantage (Driven by Primary Research)

- 3.6 Impact of AI and Gen AI on the market

- 3.7 Porters analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Phase, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Phase I

- 5.3 Phase II

- 5.4 Phase III

- 5.5 Phase IV

Chapter 6 Market Estimates and Forecast, By Study Design, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Interventional study

- 6.3 Observational study

- 6.4 Expanded access study

Chapter 7 Market Estimates and Forecast, By Therapeutic Area, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Autoimmune disease

- 7.3 Oncology

- 7.4 Cardiology

- 7.5 Infectious disease

- 7.6 Dermatology

- 7.7 Ophthalmology

- 7.8 Neurology

- 7.9 Hematology

- 7.10 Other therapeutic areas

Chapter 8 Market Estimates and Forecast, By Service Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Outsourcing service

- 8.3 In-house service

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Switzerland

- 9.3.9 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Thailand

- 9.4.10 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.5.5 Peru

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Cadiya (Clinipace)

- 10.2 Celerio

- 10.3 Charles River Laboratories

- 10.4 ClinChoice

- 10.5 ICON plc

- 10.6 IQVIA HOLDINGS

- 10.7 Labcorp Holding (Covance )

- 10.8 Medpace

- 10.9 Parexel International Corporation

- 10.10 Pharmaceutical Product Development (Thermo Fisher Scientific)

- 10.11 Qserve

- 10.12 SGS SA

- 10.13 Syneos Health

- 10.14 The Emmes Company

- 10.15 Veeda

- 10.16 Worldwide Clinical Trials

- 10.17 Wuxi AppTec Co.

臨床研究服務市場:依服務類型、臨床試驗階段、治療領域及最終使用者分類-2026-2032年全球市場預測臨床試驗市場:2026-2032年全球市場預測(依服務、研究設計、臨床階段、服務模式、治療領域及申辦方分類)

臨床研究服務市場:依服務類型、臨床試驗階段、治療領域及最終使用者分類-2026-2032年全球市場預測臨床試驗市場:2026-2032年全球市場預測(依服務、研究設計、臨床階段、服務模式、治療領域及申辦方分類) 人工智慧臨床試驗平台市場預測至2034年—按平台類型、部署模式、技術、應用、最終用戶和地區分類的全球分析

人工智慧臨床試驗平台市場預測至2034年—按平台類型、部署模式、技術、應用、最終用戶和地區分類的全球分析 臨床試驗市場報告:趨勢、預測與競爭分析(至2035年)臨床試驗機構管理市場:按服務類型、階段、技術解決方案和最終用戶分類-2026-2032年全球市場預測臨床試驗分析服務市場:2026-2032年全球市場預測(按階段、服務、治療方法、治療領域、最終用戶和部署模式分類)

臨床試驗市場報告:趨勢、預測與競爭分析(至2035年)臨床試驗機構管理市場:按服務類型、階段、技術解決方案和最終用戶分類-2026-2032年全球市場預測臨床試驗分析服務市場:2026-2032年全球市場預測(按階段、服務、治療方法、治療領域、最終用戶和部署模式分類) 人工智慧(AI)在臨床試驗中的市場:策略性洞察與預測(2026-2031 年)

人工智慧(AI)在臨床試驗中的市場:策略性洞察與預測(2026-2031 年) 人工智慧在臨床試驗最佳化市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署類型、最終用戶、解決方案和階段分類全球臨床試驗市場規模、佔有率、趨勢和成長分析報告(2026-2034)臨床試驗平台市場預測至2034年:按平台類型、臨床試驗階段、研究類型、部署模式、應用、最終用戶和地區分類的全球分析

人工智慧在臨床試驗最佳化市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署類型、最終用戶、解決方案和階段分類全球臨床試驗市場規模、佔有率、趨勢和成長分析報告(2026-2034)臨床試驗平台市場預測至2034年:按平台類型、臨床試驗階段、研究類型、部署模式、應用、最終用戶和地區分類的全球分析