|

市場調查報告書

商品編碼

2027511

甘油市場機會、成長要素、產業趨勢分析及2026-2035年預測。Glycerol Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

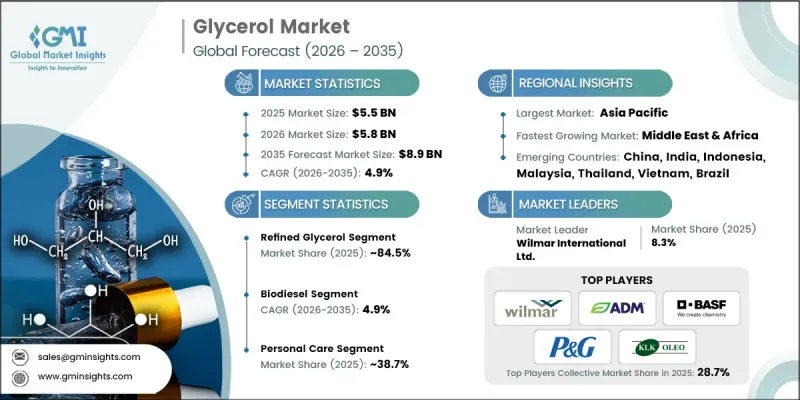

預計到 2025 年,全球甘油市場價值將達到 55 億美元,並有望以 4.9% 的複合年成長率成長,到 2035 年達到 89 億美元。

受個人護理、醫藥、食品飲料和工業應用等領域強勁需求的推動,甘油市場正經歷穩定成長。甘油(也稱為丙三醇)是一種無色、無味、口感甘甜的多元醇,主要來自生物柴油生產以及脂肪酸和醇類的製造。生物柴油的擴張帶來了豐富的粗甘油供應,這些粗甘油經過提煉後可用於高價值應用。順應永續性的趨勢,市場正朝著生物基甘油生產方向發展。消費者對個人保健產品和食品中天然無毒成分的偏好,以及甘油的保濕功效,持續推動著市場成長,使甘油成為眾多產業中用途廣泛且不可或缺的成分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 55億美元 |

| 預測金額 | 89億美元 |

| 複合年成長率 | 4.9% |

在個人護理和化妝品領域,甘油因其保濕、軟化肌膚以及與多種配方相容性而成為一種重要的成分。精製甘油可用作護膚、護髮產品、香皂、刮鬍膏和其他化妝品中的保濕劑,賦予產品柔滑的質地、保濕效果和更佳的感官體驗。在製藥領域,甘油因其在止咳糖漿、酏劑、栓劑和其他藥物製劑中的治療功效和營養價值而備受重視。在食品飲料領域,甘油可用作烘焙點心食品、加工食品、飲料和糖果甜點中的保濕劑、甜味劑、增稠劑和防腐劑,並因其無毒和營養價值而備受推崇。

預計到2025年,精製甘油市佔率將達到84.5%,到2035年將以5%的複合年成長率成長。精製甘油是指經蒸餾、離子交換、活性碳處理和膜過濾方法所獲得的純度高達99.5%至99.7%的甘油。該品類符合製藥、食品飲料和個人護理等行業嚴格的品質要求,這些行業必須最大限度地減少甲醇、脂肪酸甲酯、灰分和氯化物等雜質的含量。符合美國藥典/歐洲藥典(USP/EP)標準的藥用級甘油在注射劑、口服藥物、栓劑和醫療設備管理局(FDA)公認安全(GRAS)標準的食品級甘油在烘焙點心、飲料和糖果甜點中發揮著重要的保濕劑、甜味劑和質地改良劑的作用。

預計到2025年,生質柴油生產將佔據69.7%的市場佔有率,到2035年將以4.9%的複合年成長率成長。甘油是植物油、動物脂肪或廢棄食用油與甲醇或乙醇酯交換反應的產物,通常佔生質柴油產量的10%。可再生燃料強制性要求的不斷提高、碳減排政策的推進以及對能源安全的日益關注,正在推動全球生物柴油的生產,並導致甘油供應量的增加。歐盟、美國、巴西、印尼和阿根廷等地區大量生產粗甘油。粗甘油的品質取決於原料純度、催化劑和製程條件,純度通常在50%至85%之間,而高品質的應用則需要精煉。

預計到2025年,北美甘油市佔率將達到22%。該地區受益於生物柴油產能的擴張、精煉甘油品質標準的提高以及個人護理、製藥和食品行業的強勁需求。美國食品藥物管理局(FDA)的GRAS(公認安全)認證和美國藥典(USP)標準等法規結構確保了品質的穩定性,並促進了市場准入。美國生質柴油產業以大豆和玉米為原料,而加拿大則以菜籽為原料生產生質柴油。消費者對個人保健產品和潔淨標示食品中天然成分的日益關注進一步推動了需求。先進的精煉技術和永續的化學發展使北美成為甘油及其衍生物的創新中心。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 原油

- 純化

第6章 市場估計與預測:依來源分類,2022-2035年

- 生質柴油

- 脂肪酸

- 脂醇類

- 肥皂產業

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 個人護理

- 製藥

- 醇酸樹脂

- 食品/飲料

- 聚醚多元醇

- 菸草加濕器

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- ADM

- BASF SE

- COCOCHEM

- Dow

- Emery Oleochemicals

- Godrej Industries Limited

- Kao Corporation

- KLK OLEO

- Monarch Chemicals Ltd

- Oleon NV

- Procter &Gamble

- Wilmar International Ltd.

- Aemetis, Inc.

The Global Glycerol Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 8.9 billion by 2035.

The market is witnessing steady expansion, driven by strong demand across sectors such as personal care, pharmaceuticals, food & beverages, and industrial applications. Glycerol, also known as glycerine or glycerin, is a colorless, odorless, and sweet-tasting polyol primarily obtained as a by-product of biodiesel production and fatty acid/alcohol manufacturing. The market trend is shifting toward bio-based glycerol production in line with sustainability initiatives, as biodiesel expansion generates ample crude glycerol supply, which is refined for high-value applications. Consumer preference for natural, non-toxic ingredients in personal care and food products, along with glycerol's humectant and moisturizing properties, continues to propel market growth, positioning glycerol as a versatile and essential ingredient across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 4.9% |

In the personal care and cosmetics sector, glycerol is a critical ingredient due to its moisture-retention capabilities, skin-softening properties, and compatibility with various formulations. Refined glycerol functions as a humectant in skincare, hair care, soaps, shaving creams, and other cosmetic products, providing smooth texture, hydration, and improved sensory qualities. In pharmaceuticals, glycerol is valued for its therapeutic and nutritive properties in cough syrups, elixirs, suppositories, and other medicinal formulations. In food & beverages, it serves as a humectant, sweetener, thickener, and preservative in baked goods, processed foods, beverages, and confectionery, appreciated for its non-toxic nature and nutritional value.

The refined glycerol segment held 84.5% share in 2025 and is expected to grow at a CAGR of 5% by 2035. The refined segment represents high-purity glycerol (99.5-99.7%), achieved through distillation, ion exchange, activated carbon treatment, and membrane filtration. It caters to stringent quality requirements in pharmaceuticals, food & beverages, and personal care, where impurities such as methanol, fatty acid methyl esters, ash, and chlorides must be minimized. Pharmaceutical-grade glycerol meeting USP/EP standards commands premium pricing for injectable formulations, oral medications, suppositories, and medical devices. Food-grade glycerol adhering to FCC and FDA GRAS standards is essential for baked goods, beverages, and confectionery, functioning as a humectant, sweetener, and texture enhancer.

The biodiesel production segment accounted for 69.7% share in 2025 and is expected to grow at a CAGR of 4.9% by 2035. Glycerol is generated as a by-product during the transesterification of vegetable oils, animal fats, or waste cooking oils with methanol or ethanol, typically comprising 10% of biodiesel output. Expanding renewable fuel mandates, carbon reduction policies, and energy security concerns have driven biodiesel production globally, increasing glycerol availability. Regions such as the European Union, United States, Brazil, Indonesia, and Argentina produce significant crude glycerol volumes. Quality varies based on feedstock purity, catalyst, and process conditions, generally ranging from 50-85% purity and requiring refining for premium applications.

North America Glycerol Market accounted for 22% share in 2025. The region benefits from expanding biodiesel capacity, high-quality standards favoring refined glycerol, and strong demand from personal care, pharmaceutical, and food industries. Regulatory frameworks such as FDA GRAS and USP standards ensure consistent quality, facilitating market access. The U.S. biodiesel industry relies on soybean and corn feedstock, while Canada contributes with canola-based biodiesel. Growing consumer awareness of natural ingredients in personal care and clean-label foods further drives demand. Advanced refining technologies and sustainable chemical development establish North America as an innovation hub for glycerol and its derivatives.

Key players operating in the Global Glycerol Market include COCOCHEM, ADM, Wilmar International Ltd., Oleon NV, Emery Oleochemicals, KLK OLEO, BASF SE, Procter & Gamble, Aemetis, Inc., Monarch Chemicals Ltd, Dow, Kao Corporation, and Godrej Industries Limited. Companies in the Global Glycerol Market strengthen their position by investing in advanced refining technologies to improve purity, yield, and operational efficiency. Firms collaborate with pharmaceutical, personal care, and food manufacturers to expand application portfolios. Strategic acquisitions and partnerships secure feedstock supply chains and enhance distribution networks. Innovation in bio-based glycerol production, including waste-to-value technologies, improves sustainability credentials. Marketing initiatives focus on highlighting glycerol's non-toxic, natural properties to align with consumer preferences for clean-label products. Companies also prioritize regulatory compliance and product certification to access premium applications, while R&D efforts target derivative products and high-margin formulations to expand market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Source

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Crude

- 5.3 Refined

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Biodiesel

- 6.3 Fatty Acids

- 6.4 Fatty Alcohols

- 6.5 Soap Industry

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Personal Care

- 7.3 Pharmaceutical

- 7.4 Alkyd Resins

- 7.5 Foods & Beverages

- 7.6 Polyether Polyols

- 7.7 Tobacco Humectants

- 7.8 Other

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ADM

- 9.2 BASF SE

- 9.3 COCOCHEM

- 9.4 Dow

- 9.5 Emery Oleochemicals

- 9.6 Godrej Industries Limited

- 9.7 Kao Corporation

- 9.8 KLK OLEO

- 9.9 Monarch Chemicals Ltd

- 9.10 Oleon NV

- 9.11 Procter & Gamble

- 9.12 Wilmar International Ltd.

- 9.13 Aemetis, Inc.

甘油市場:依原料、應用及通路分類-2026-2032年全球市場預測三醋精市場:2026-2032年全球市場預測(依純度等級、生產流程、形態、應用及分銷通路分類)

甘油市場:依原料、應用及通路分類-2026-2032年全球市場預測三醋精市場:2026-2032年全球市場預測(依純度等級、生產流程、形態、應用及分銷通路分類) 全球甘油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球聚甘油癸二酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球甘油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球聚甘油癸二酸酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球甘油衍生物市場報告木質松香甘油酯市場按類型、純度等級、最終用途產業、應用和分銷管道分類,全球預測(2026-2032年)松香和甘油酯市場:依純度等級、形態、最終用途和通路分類,全球預測(2026-2032年)

2026年全球甘油衍生物市場報告木質松香甘油酯市場按類型、純度等級、最終用途產業、應用和分銷管道分類,全球預測(2026-2032年)松香和甘油酯市場:依純度等級、形態、最終用途和通路分類,全球預測(2026-2032年) 甘油市場規模、佔有率和成長分析(按等級、來源、應用和地區分類)-2026-2033年產業預測

甘油市場規模、佔有率和成長分析(按等級、來源、應用和地區分類)-2026-2033年產業預測 三醋精:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

三醋精:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 三醋酸甘油酯市場-全球產業規模、佔有率、趨勢、機會與預測,按等級、產品類型、最終用戶、地區和競爭細分,2020-2030 年

三醋酸甘油酯市場-全球產業規模、佔有率、趨勢、機會與預測,按等級、產品類型、最終用戶、地區和競爭細分,2020-2030 年