|

市場調查報告書

商品編碼

2027493

發泡玻璃市場機會、成長要素、產業趨勢分析及2026-2035年預測Foam Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

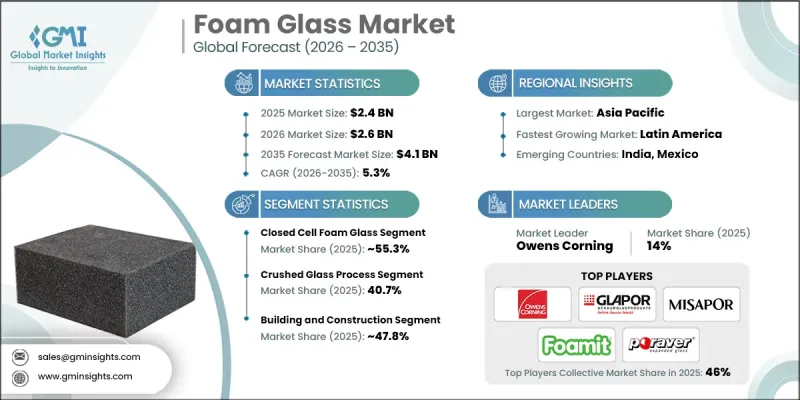

預計到 2025 年,全球發泡玻璃市場價值將達到 24 億美元,並預計以 5.3% 的複合年成長率成長,到 2035 年達到 41 億美元。

隨著建築和工業應用領域對永續、高性能隔熱材料的需求不斷成長,全球發泡玻璃產業正穩步發展。發泡玻璃由回收玻璃製成,具有輕質和高耐久性,是一種堅固的多孔結構。它因其卓越的隔熱性能、隔音性能以及防潮、耐化學腐蝕和防火性能而廣受讚譽。這些特性使其適用於建築圍護結構、屋頂系統以及工業設施、倉儲環境和海洋基礎設施等特殊保溫應用。對永續建築方法和循環材料利用的日益重視正在推動市場普及。監管壓力促使人們推廣節能環保的建材,進一步刺激了市場需求。然而,來自其他隔熱材料的競爭仍在影響市場動態,尤其是在那些優先考慮成本效益和易於安裝的領域。儘管如此,持續的產品創新和性能改進正在擴大發泡玻璃在先進建築和工程應用中的使用範圍。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 24億美元 |

| 預計金額 | 41億美元 |

| 複合年成長率 | 5.3% |

截至2025年,閉孔發泡玻璃市佔率將達到55.3%,預計到2035年將以5.4%的複合年成長率成長。該細分市場的主導地位歸功於其卓越的抗吸水性能、高機械穩定性以及即使在惡劣環境條件下也能保持穩定的隔熱性能。其在嚴苛的建築環境中展現出的可靠性也使其應用範圍得以不斷擴大。

預計到2025年,碎玻璃加工製程將佔據40.7%的市場佔有率,並在2026年至2035年間以5.5%的複合年成長率成長。該製造方法之所以保持主導地位,是因為其成本效益高、回收材料利用率高以及擴充性工業化生產。由於其結構性能和強度均勻,此工藝適用於保溫塊和輕質骨材應用。持續的製程最佳化正在進一步提高生產效率和應用範圍。

預計到2025年,北美發泡玻璃市佔率將達到35.8%,反映出該地區強勁的需求。推動這一市場成長的因素包括:建築規範的進步、對節能建築解決方案日益成長的關注,以及再生材料產品的廣泛應用。市場需求持續成長,尤其是在商業基礎設施和特殊保溫應用領域,特別是對耐久性、安全性和永續性要求極高的專案中。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 建築和基礎設施領域的成長

- 輕量耐用

- 永續性和回收利用

- 產業潛在風險與挑戰

- 替補上場競爭

- 高昂的生產成本

- 市場機遇

- 在建設活動蓬勃發展的新興市場,企業正尋求擴張。

- 積層製造和3D列印領域的創新

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 開孔發泡玻璃

- 閉孔發泡玻璃

- 混合氣泡玻璃

第6章 市場估價與預測:依製造流程分類,2022-2035年

- 玻璃破碎法

- 玻璃粉法

- 直接髮泡法

- 漿液法

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 建築/施工

- 平屋頂

- 立面和外牆

- 地下和地下應用

- 內牆保溫

- 其他

- 工業的

- 罐底保溫

- 管道保溫

- 容器和設備的隔熱材料

- 其他

- 化學

- 耐腐蝕隔熱材料

- 高溫應用

- 船

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Owens Corning

- Glapor Werk Mitterteich GmbH

- Misapor AG

- Veriso GmbH &Co. KG

- Dennert Poraver GmbH

- 北美航空骨材有限公司

- Uusioaines Oy

- Zhejiang Zhenshen Insulation Technology Corp.

- Energocell Kft.

- Glasopor AS

- Glavel Inc.

- Refaglass sro

- Steinbach Schaumglas GmbH &Co. KG

- Foamit Group

The Global Foam Glass Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 4.1 billion by 2035.

The global foam glass industry is gaining steady traction as demand increases for sustainable, high-performance insulation materials across construction and industrial applications. Foam glass is produced by converting recycled glass into a rigid, porous structure that delivers a combination of lightweight characteristics and strong durability. It is widely valued for its thermal insulation efficiency, acoustic control capabilities, and resistance to moisture, chemicals, and fire exposure. These properties make it suitable for use in building envelopes, roofing systems, and specialized insulation applications across industrial facilities, storage environments, and marine-related infrastructure. Growing emphasis on sustainable construction practices and circular material usage is supporting market adoption. Regulatory pressure promoting energy efficiency and environmentally responsible building materials is further strengthening demand. However, competition from alternative insulation materials continues to influence market dynamics, particularly where cost efficiency and installation convenience are prioritized. Despite this, ongoing product innovation and performance improvements are reinforcing foam glass adoption across advanced construction and engineering applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.3% |

The closed-cell foam glass segment accounted for 55.3% share in 2025 and is expected to grow at a CAGR of 5.4% through 2035. This segment leads due to its superior resistance to water absorption, strong mechanical stability, and consistent insulation performance under extreme environmental conditions. Its reliability in demanding construction environments continues to support its widespread use.

The crushed glass process segment held a 40.7% share in 2025 and is projected to grow at a CAGR of 5.5% from 2026 to 2035. This production method remains dominant due to its cost efficiency, high utilization of recycled materials, and scalability for industrial manufacturing. It supports uniform structural properties and strength, making it suitable for insulation blocks and lightweight aggregate applications. Continuous process optimization is further improving production efficiency and application versatility.

North America Foam Glass Market accounted for 35.8% share in 2025, reflecting strong regional demand. The market is supported by advanced construction standards, increasing focus on energy-efficient building solutions, and growing adoption of recycled material-based products. Demand continues to rise across commercial infrastructure and specialized insulation applications, particularly in projects emphasizing durability, safety, and sustainability.

Key companies operating in the Global Foam Glass Market include Owens Corning, Foamit Group, Glapor Werk Mitterteich GmbH, Misapor AG, Dennert Poraver GmbH, Veriso GmbH & Co. KG, AeroAggregates of North America, LLC, Uusioaines Oy, Glasopor AS, Glavel Inc., Energocell Kft., Zhejiang Zhenshen Insulation Technology Corp., Refaglass s.r.o., and Steinbach Schaumglas GmbH & Co. KG. Companies in the Global Foam Glass Market are implementing targeted strategies to strengthen their competitive positioning and expand market share. A major focus is placed on product innovation to enhance thermal performance, durability, and sustainability characteristics. Manufacturers are investing in advanced recycling and production technologies to improve efficiency and reduce operational costs. Strategic partnerships with construction firms and infrastructure developers are being used to expand application reach. Capacity expansion initiatives are supporting increased demand from large-scale construction projects. Companies are also strengthening their distribution networks to improve market accessibility across regions. In addition, sustainability-driven strategies, including increased use of recycled raw materials and low-emission production methods, are helping firms align with environmental regulations and attract eco-conscious customers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Production process

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in Construction and Infrastructure

- 3.2.1.2 Lightweight and Durable

- 3.2.1.3 Sustainability and Recycling

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternatives

- 3.2.2.2 High Production Cost

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing construction activity

- 3.2.3.2 Innovation in additive manufacturing & 3d printing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Open cell foam glass

- 5.3 Closed cell foam glass

- 5.4 Mixed cell foam glass

Chapter 6 Market Estimates and Forecast, By Production Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Crushed glass process

- 6.3 Glass powder process

- 6.4 Direct foaming process

- 6.5 Slurry methods

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building and construction

- 7.2.1 Flat roofs

- 7.2.2 Facades & exterior walls

- 7.2.3 Underground & below grade applications

- 7.2.4 Interior insulation

- 7.2.5 Others

- 7.3 Industrial

- 7.3.1 Tank base insulation

- 7.3.2 Pipe insulation

- 7.3.3 Vessel & equipment insulation

- 7.3.4 Other

- 7.4 Chemical

- 7.4.1 Corrosion resistant insulation

- 7.4.2 High temperature applications

- 7.5 Marine

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Owens Corning

- 9.2 Glapor Werk Mitterteich GmbH

- 9.3 Misapor AG

- 9.4 Veriso GmbH & Co. KG

- 9.5 Dennert Poraver GmbH

- 9.6 AeroAggregates of North America, LLC

- 9.7 Uusioaines Oy

- 9.8 Zhejiang Zhenshen Insulation Technology Corp.

- 9.9 Energocell Kft.

- 9.10 Glasopor AS

- 9.11 Glavel Inc.

- 9.12 Refaglass s.r.o.

- 9.13 Steinbach Schaumglas GmbH & Co. KG

- 9.14 Foamit Group

發泡玻璃市場:全球市場預測,2026-2032年

發泡玻璃市場:全球市場預測,2026-2032年 發泡玻璃市場預測至2034年—按產品類型、形狀、製造流程、密度、應用、最終用戶和地區分類的全球分析

發泡玻璃市場預測至2034年—按產品類型、形狀、製造流程、密度、應用、最終用戶和地區分類的全球分析 發泡玻璃市場:按類型、應用、終端用戶產業和地區分類

發泡玻璃市場:按類型、應用、終端用戶產業和地區分類 發泡玻璃市場:市場規模、佔有率和趨勢分析(按結構、應用和地區分類),細分市場預測(2026-2033 年)

發泡玻璃市場:市場規模、佔有率和趨勢分析(按結構、應用和地區分類),細分市場預測(2026-2033 年) 全球發泡玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球發泡玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 發泡玻璃市場規模、佔有率和成長分析(按類型、製造流程、應用、最終用戶和地區分類)—產業預測(2026-2033)

發泡玻璃市場規模、佔有率和成長分析(按類型、製造流程、應用、最終用戶和地區分類)—產業預測(2026-2033) 泡沫玻璃市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(開孔、閉孔)、按應用(工業、建築和施工、其他)、按地區、按競爭細分,2020-2030 年泡沫玻璃隔熱材料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、製造流程、應用、地區、競爭細分,2020-2030 年)

泡沫玻璃市場-全球產業規模、佔有率、趨勢、機會和預測,按類型(開孔、閉孔)、按應用(工業、建築和施工、其他)、按地區、按競爭細分,2020-2030 年泡沫玻璃隔熱材料市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、製造流程、應用、地區、競爭細分,2020-2030 年) 發泡玻璃市場分析及預測(至2034年):類型、產品、應用、材料類型、最終用戶、製程、技術、安裝類型、設備

發泡玻璃市場分析及預測(至2034年):類型、產品、應用、材料類型、最終用戶、製程、技術、安裝類型、設備