|

市場調查報告書

商品編碼

2027488

2026 年至 2035 年氣動輸送系統的市場機會、成長要素、產業趨勢分析與預測。Pneumatic Conveying Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

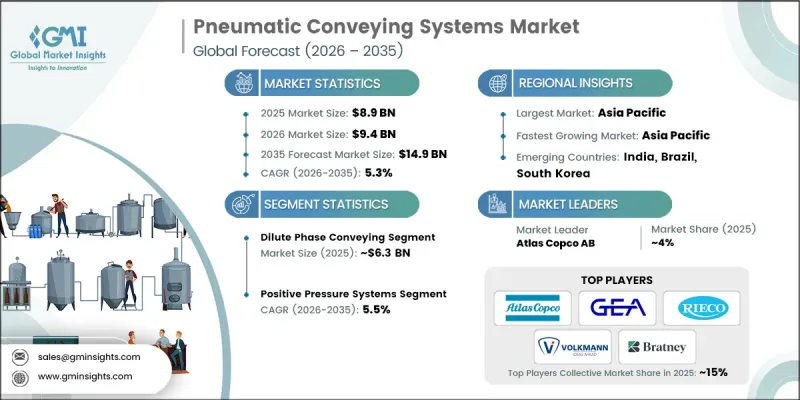

2025年全球氣動輸送系統市值為89億美元,預計2035年將以5.3%的複合年成長率成長至149億美元。

市場成長主要受食品加工、製藥和化學等行業日益成長的需求驅動,這些行業對高效的散裝物料輸送至關重要。工業的持續擴張和現代化推動了對可靠、自動化輸送解決方案的更大需求,這些解決方案能夠提高生產效率並降低營運成本。系統效率的提升、先進的控制技術以及高耐久性管道材料的應用,都促進了輸送解決方案的持續普及。此外,智慧技術的整合提高了製程監控的精確度,並增強了系統效能。設計上的持續創新,例如改進的氣流機制和節能配置,進一步推動了市場成長。製造環境中對自動化的日益重視也加速了氣動輸送系統的應用,因為它們能夠實現穩定、無污染的物料輸送。隨著各行業持續專注於營運效率和流程最佳化,全球市場對先進輸送解決方案的需求預計將穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 89億美元 |

| 預計金額 | 149億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,稀相輸送市場規模將達到63億美元,並在2026年至2035年間以5.4%的複合年成長率成長。該細分市場憑藉其高速輸送物料並維持穩定流動特性的能力,持續佔據主導地位。這項技術適用於長距離輸送和複雜的路徑配置,並可應用於廣泛的工業領域。其多輸入/輸出點處理能力提高了操作柔軟性,並能有效處理各種類型的材料類型,進一步推動了此技術的應用。速度、適應性和可靠性的結合,持續推動市場對稀相輸送系統的需求。

預計到2025年,正壓輸送系統市佔率將達到44.3%,並在2026年至2035年間以5.5%的複合年成長率成長。這些系統在供料點產生壓力,並透過管道將物料輸送到指定的排放點。它們能夠處理長距離輸送和多個排放點,因此成為許多工業領域的首選解決方案。正壓輸送系統也因其相對簡單的設計、易於整合和高效運作備受青睞。它們能夠適應各種物料和配置,從而鞏固了其強大的市場地位。

美國氣動輸送系統市場預計到2025年將達到19億美元,並在2026年至2035年間以5.2%的複合年成長率成長。市場成長主要由食品加工、製藥和化學等成熟產業部門所驅動,這些領域對先進的物料輸送方案有著迫切的需求。對安全性、合規性和營運效率日益成長的關注,推動了封閉式和自動化系統的應用。持續的現代化改造,包括老舊設備的更換和先進技術的應用,也進一步促進了市場擴張。強大的工業基礎設施和對製程最佳化的持續投入,是美國在區域市場保持主導地位的關鍵因素。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 製造業和加工業的擴張

- 自動化和工業4.0實施

- 醫藥、食品和飲料產業的成長

- 產業潛在風險與挑戰

- 較高的初始投資和安裝成本

- 維護的複雜性和特殊要求

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 稀相傳輸

- 高密度交通

第6章 市場估計與預測:依技術分類,2022-2035年

- 正壓系統

- 真空系統

- 複合系統

第7章 市場估計與預測:依材料類型分類,2022-2035年

- 粉末/顆粒

- 顆粒

- 片狀物和纖維

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 化學品

- 製藥

- 食品/飲料

- 水泥與建築

- 礦產和採礦

- 紙漿和造紙

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Atlas Copco AB

- 布拉特尼公司

- Claudius Peters(Americas)Inc.

- Compass Systems &Sales, LLC

- Coperion GmbH

- Delfin Industrial Vacuums

- Dynamic Air Inc.

- GEA Group Aktiengesellschaft

- Gericke AG

- Macawber Engineering, Inc.

- Rieco Industries Limited

- Spiroflow Systems, Inc.

- VAC-U-MAX

- VOLKMANN, Inc.

- Whirl-Air-Flow Corporation

The Global Pneumatic Conveying Systems Market was valued at USD 8.9 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 14.9 billion by 2035.

Market growth is driven by rising demand from industries such as food processing, pharmaceuticals, and chemicals, where efficient bulk material handling is critical. Ongoing industrial expansion and modernization have increased the need for reliable, automated conveying solutions that improve productivity and reduce operational costs. Advancements in system efficiency, enhanced control technologies, and the use of durable pipeline materials are contributing to sustained adoption. In addition, the integration of smart technologies is enabling better process monitoring and improved system performance. Continuous innovation in design, including improved airflow mechanisms and energy-efficient configurations, is further supporting market growth. Increasing emphasis on automation across manufacturing environments is also accelerating adoption, as pneumatic conveying systems provide consistent and contamination-free material transfer. As industries continue to focus on operational efficiency and process optimization, the demand for advanced conveying solutions is expected to rise steadily across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.9 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 5.3% |

The dilute phase conveying segment generated USD 6.3 billion in 2025 and is anticipated to grow at a CAGR of 5.4% from 2026 to 2035. This segment remains dominant due to its ability to transport materials at high velocities while maintaining consistent flow characteristics. The technology supports long-distance conveying and complex routing configurations, making it suitable for diverse industrial applications. Its capability to handle multiple input and output points enhances operational flexibility, while maintaining efficiency across various material types further strengthens its adoption. The combination of speed, adaptability, and reliability continues to drive demand for dilute phase systems.

The positive pressure systems segment accounted for 44.3% share in 2025 and is projected to grow at a CAGR of 5.5% during 2026-2035. These systems operate by generating pressure at the feed point to move materials through pipelines toward designated discharge points. Their ability to support long-distance transportation and multiple discharge locations makes them a preferred solution in many industrial settings. Positive pressure systems are also valued for their relatively simple design, ease of integration, and efficient operation. Their versatility in handling various materials and configurations contributes to their strong market position.

United States Pneumatic Conveying Systems Market reached USD 1.9 billion in 2025 and is expected to grow at a CAGR of 5.2% from 2026 to 2035. Market growth is supported by the presence of well-established industrial sectors, including food processing, pharmaceuticals, and chemicals, all of which require advanced material handling solutions. Increasing focus on safety, regulatory compliance, and operational efficiency is driving the adoption of enclosed and automated systems. Ongoing modernization efforts, including the replacement of legacy equipment and the implementation of advanced technologies, are further contributing to market expansion. Strong industrial infrastructure and continued investments in process optimization are reinforcing the country's leadership in the regional market.

Key players operating in the Global Pneumatic Conveying Systems Market include Atlas Copco AB, Bratney Companies, Claudius Peters (Americas) Inc., Compass Systems & Sales, LLC, Coperion GmbH, Delfin Industrial Vacuums, Dynamic Air Inc., GEA Group Aktiengesellschaft, Gericke AG, Macawber Engineering, Inc., Rieco Industries Limited, Spiroflow Systems, Inc., VAC-U-MAX, VOLKMANN, Inc., and Whirl-Air-Flow Corporation. Companies in the Pneumatic Conveying Systems Market are focusing on innovation, system efficiency, and strategic partnerships to strengthen their competitive position. Investments in advanced control systems, energy-efficient designs, and automation technologies are enhancing product performance and reliability. Manufacturers are also expanding their global footprint through collaborations and distribution network development to reach new markets. Customization of solutions to meet specific industry requirements is becoming a key differentiator. In addition, companies are prioritizing research and development to improve material handling efficiency and reduce operational costs. The integration of digital monitoring and smart technologies is further enabling predictive maintenance and optimized system performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Material type

- 2.2.5 End use industry

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of manufacturing and processing industries

- 3.2.1.2 Automation and industry 4.0 adoption

- 3.2.1.3 Growth in pharmaceutical and food & beverage sectors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront capital and installation costs

- 3.2.2.2 Maintenance complexity and specialized requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Dilute phase conveying

- 5.3 Dense phase conveying

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Positive pressure systems

- 6.3 Vacuum systems

- 6.4 Combination systems

Chapter 7 Market Estimates & Forecast, By Material Type, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Powder & granules

- 7.3 Pellets

- 7.4 Flakes & fibers

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Chemicals

- 8.3 Pharmaceuticals

- 8.4 Food & beverages

- 8.5 Cement & construction

- 8.6 Minerals & mining

- 8.7 Pulp & paper

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Atlas Copco AB

- 11.2 Bratney Companies

- 11.3 Claudius Peters (Americas) Inc.

- 11.4 Compass Systems & Sales, LLC

- 11.5 Coperion GmbH

- 11.6 Delfin Industrial Vacuums

- 11.7 Dynamic Air Inc.

- 11.8 GEA Group Aktiengesellschaft

- 11.9 Gericke AG

- 11.10 Macawber Engineering, Inc.

- 11.11 Rieco Industries Limited

- 11.12 Spiroflow Systems, Inc.

- 11.13 VAC-U-MAX

- 11.14 VOLKMANN, Inc.

- 11.15 Whirl-Air-Flow Corporation