|

市場調查報告書

商品編碼

2027484

丙烯酸纖維市場商業機會、成長要素、產業趨勢分析及2026-2035年預測Acrylic Fibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

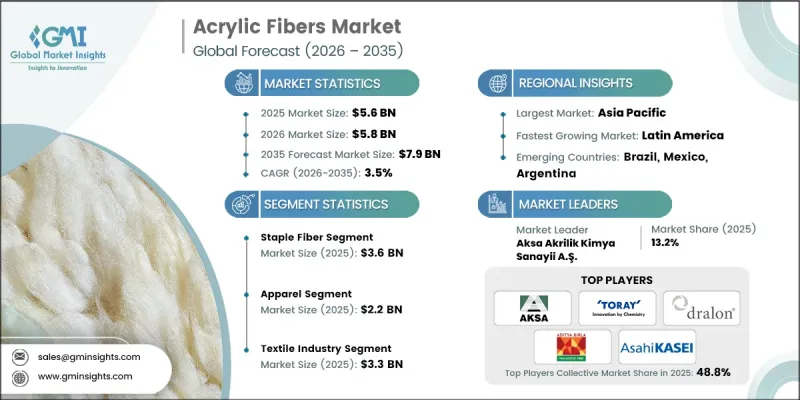

預計到 2025 年,全球丙烯酸纖維市場價值將達到 56 億美元,並預計以 3.5% 的複合年成長率成長,到 2035 年達到 79 億美元。

腈綸纖維是由聚丙烯腈(PAN)製成的合成材料,其組成單元中至少85%為丙烯腈。其生產始於化學工藝,將石油衍生化合物轉化為長鏈聚合物,然後紡成纖維。這些纖維輕盈柔軟,兼具保暖性和耐用性,是羊毛的廣泛替代品。它們耐日光、防黴、抗皺和耐化學腐蝕,使其成為服飾和家用紡織品的理想選擇。腈綸纖維具有良好的保暖性和彈性,能夠有效鎖住體溫,同時其優異的染色性能確保了色彩鮮豔持久。腈綸纖維用途廣泛,適用於毛衣、圍巾、襪子和運動服等服裝產品,以及毯子、地毯、室內裝潢和戶外家具罩等家用紡織品產品,是天然羊毛的經濟實惠的替代品。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 56億美元 |

| 預測金額 | 79億美元 |

| 複合年成長率 | 3.5% |

預計到2025年,短纖維市場規模將達36億美元。這個市場至關重要,因為短纖維易於與棉、羊毛和聚酯混紡,從而生產出柔軟性、性能和舒適度更佳的布料。製造商正利用短腈綸纖維生產兼具柔軟性和保暖性的服裝、毯子、地毯和室內裝飾布料,這些產品與標準紡紗設備相容。

預計到2025年,服裝市場規模將達到22億美元。腈綸纖維因其輕盈、柔軟且保暖性能優異,廣泛應用於服飾和家用紡織品。這種纖維可用於生產毛衣、襪子、圍巾、毯子、床上用品和窗簾,兼具耐用性和易於護理。其彈性也使其適用於地毯和毛毯,並且具有抗褪色和抗污漬的特性。

預計到2025年,美國丙烯酸纖維市場規模將達到7.943億美元。北美市場受益於成熟的生產流程,這些工藝廣泛應用於紡織、工業和汽車內飾領域。推動這一成長的主要因素包括纖維生產技術的進步、對內飾材料需求的成長以及戶外紡織品的日益普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對價格實惠的紡織品的需求不斷成長

- 全球紡織業的成長

- 耐用且易於維護

- 陷阱與挑戰

- 與其他合成纖維的競爭

- 易燃且對熱敏感

- 機會

- 紡織生產中的技術創新

- 混紡織物需求不斷成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依纖維類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依紡織品類型分類,2022-2035年

- 短纖維

- 陶(陶染)纖維

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 家用紡織品

- 不織布

- 工業和技術用紡織品

- 地毯和毛毯

- 戶外及休閒設備

- 家具布料

- 毯子和床上用品

- 工藝和嗜好

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 紡織業

- 汽車產業

- 建設產業

- 過濾和分離

- 航太/國防

- 醫療產業

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Aksa Akrilik Kimya Sanayii AS

- TORAY INDUSTRIES, INC.

- Dralon GmbH

- Thai Acrylic Fibre Co. Ltd.

- TAIRYLAN ACRYLIC FIBER

- Kaneka Corporation

- Exlan Japan Co., Ltd.

- Asahi Kasei Corp.

- Kaltex Fibers

- Indian Acrylics Limited

The Global Acrylic Fibers Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 7.9 billion by 2035.

Acrylic fibers are synthetic materials derived from polyacrylonitrile (PAN), where at least 85% of the units are acrylonitrile. The production begins with chemical processes that transform petroleum derivatives into long-chain polymers, which are then spun into fibers. These fibers are widely used as wool alternatives because they offer a lightweight, soft texture while retaining warmth and durability. Their resistance to sunlight, mildew, wrinkles, and chemicals makes them ideal for both clothing and home textiles. Acrylic fibers maintain insulation and elasticity, preserving body heat, while their excellent dye absorption ensures vibrant, long-lasting colors. The versatility of acrylic fibers allows their use in apparel such as sweaters, scarves, socks, and sportswear, as well as in home textiles like blankets, carpets, upholstery, and outdoor furniture covers, providing affordable alternatives to natural wool.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 3.5% |

The staple fiber segment reached USD 3.6 billion in 2025. This segment is critical because short-length fibers blend easily with cotton, wool, and polyester to produce fabrics with enhanced flexibility, performance, and comfort. Manufacturers rely on staple acrylic fibers to create clothing, blankets, carpets, and upholstery that combine softness, warmth, and compatibility with standard spinning equipment.

The apparel segment captured USD 2.2 billion in 2025. Acrylic fibers are extensively used in garments and home textiles due to their lightweight, soft, and insulating characteristics. The fibers enable the production of sweaters, socks, scarves, blankets, bedding, and curtains, providing durability and low-maintenance convenience. Their resilience also makes them suitable for carpets and rugs, maintaining color longevity and stain resistance.

U.S. Acrylic Fibers Market reached USD 794.3 million in 2025. The North American market benefits from established manufacturing processes that serve textile, industrial, and automotive interior applications. Growth is fueled by technological advancements in fiber production, rising demand for home furnishings, and increasing adoption of outdoor textile products.

Key players in the Acrylic Fibers Market include TORAY INDUSTRIES, INC., Asahi Kasei Corp., Aksa Akrilik Kimya Sanayii A.S., Dralon GmbH, Kaneka Corporation, Thai Acrylic Fibre Co. Ltd., Exlan Japan Co., Ltd., TAIRYLAN ACRYLIC FIBER, Kaltex Fibers, and Indian Acrylics Limited. Companies in the acrylic fibers market strengthen their position through strategies such as expanding production capacities to meet growing global demand, investing in advanced polymerization and spinning technologies to enhance fiber quality, and developing specialized fiber variants for apparel, home textiles, and industrial applications. Firms focus on forming strategic alliances with textile manufacturers and distributors to increase market penetration and improve supply chain efficiency. Marketing initiatives highlight the eco-friendly and cost-effective advantages of acrylic fibers, while research and development efforts target improved durability, dye retention, and thermal performance to differentiate products and capture a larger market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Fiber Type

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for affordable textiles

- 3.2.1.2 Growth of the global textile industry

- 3.2.1.3 Durability and easy maintenance

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Competition from other synthetic fibers

- 3.2.2.2 Flammability and heat sensitivity

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovations in fiber production

- 3.2.3.2 Growing demand for blended fabrics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By fiber type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Fiber Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Staple fiber

- 5.3 Tow (tow-dyed) fiber

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Home textiles

- 6.3 Nonwoven fabrics

- 6.4 Industrial and technical textiles

- 6.5 Carpets and rugs

- 6.6 Outdoor and recreational products

- 6.7 Upholstery

- 6.8 Blankets and bedding

- 6.9 Craft and hobby

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textile industry

- 7.3 Automotive industry

- 7.4 Construction industry

- 7.5 Filtration and separation

- 7.6 Aerospace and defense

- 7.7 Healthcare industry

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Aksa Akrilik Kimya Sanayii A.S.

- 9.2 TORAY INDUSTRIES, INC.

- 9.3 Dralon GmbH

- 9.4 Thai Acrylic Fibre Co. Ltd.

- 9.5 TAIRYLAN ACRYLIC FIBER

- 9.6 Kaneka Corporation

- 9.7 Exlan Japan Co., Ltd.

- 9.8 Asahi Kasei Corp.

- 9.9 Kaltex Fibers

- 9.10 Indian Acrylics Limited

短纖丙烯酸纖維市場:全球市場預測,2026-2032年丙烯酸纖維市場-2026-2032年全球市場預測

短纖丙烯酸纖維市場:全球市場預測,2026-2032年丙烯酸纖維市場-2026-2032年全球市場預測 腈綸纖維市場:依染色方法、纖維形態、混紡方式、最終用戶及地區分類

腈綸纖維市場:依染色方法、纖維形態、混紡方式、最終用戶及地區分類 全球丙烯酸纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球丙烯酸纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 腈綸纖維市場規模、佔有率和成長分析(按纖維類型、染色方法、混紡、最終用戶和地區分類)—產業預測(2026-2033 年)

腈綸纖維市場規模、佔有率和成長分析(按纖維類型、染色方法、混紡、最終用戶和地區分類)—產業預測(2026-2033 年) 2018-2034年全球腈綸市場需求及預測分析

2018-2034年全球腈綸市場需求及預測分析 丙烯酸纖維:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

丙烯酸纖維:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球丙烯酸纖維市場評估:依技術、形狀、混合、最終用途產業、地區、機會、預測(2017-2031)

全球丙烯酸纖維市場評估:依技術、形狀、混合、最終用途產業、地區、機會、預測(2017-2031)