|

市場調查報告書

商品編碼

2027481

露營帳篷市場機會、成長要素、產業趨勢分析及2026-2035年預測Camping Tent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

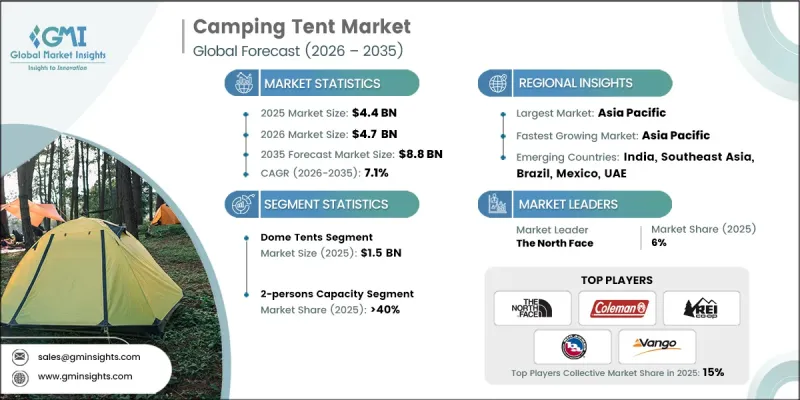

預計到 2025 年,全球露營帳篷市場價值將達到 44 億美元,並預計以 7.1% 的複合年成長率成長,到 2035 年達到 88 億美元。

受疫情後生活方式改變的影響,體驗式旅行和以健康為導向的戶外活動日益受到青睞,推動了露營裝備市場的蓬勃發展。消費者被親近大自然的休閒體驗所吸引,這些體驗既能保持社交距離,又能改善社交距離健康,也能增進家庭感情。人們對健行、健行和觀賞野生動物等探險旅行的興趣日益濃厚,也帶動了對耐用、輕巧、多功能露營裝備的需求成長。政府對戶外休閒的支持,包括對公共土地開發和生態旅遊計畫的資助,也促進了市場的擴張。帳篷設計、材料和組裝便利性不斷創新,而兼具便攜性和高性能的解決方案正變得越來越受歡迎。隨著露營在都市區和鄉村地區越來越受歡迎,製造商在產品開發中更加重視舒適性、耐用性和效率,以滿足不斷變化的消費者需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 44億美元 |

| 預測金額 | 88億美元 |

| 複合年成長率 | 7.1% |

由於其多功能性和人性化設計,圓頂帳篷市場預計到2025年將達到15億美元的市場規模。其弧形桿結構提供了穩定性、出色的抗風性和輕盈的便攜性,使其適用於各種露營場景。最常見的類型是三季圓頂帳篷,它在溫暖的天氣裡通風良好,提供適度的防雨保護,並能抵禦常見的風力條件。其易於搭建且相對輕巧(雙人款式通常重4-7磅),使其適合從新手到經驗豐富的露營者使用,而其實惠的價格也進一步提升了其市場受歡迎程度。

到2025年,雙人帳篷將佔據40%的市場。這類帳篷深受尋求更大空間存放裝備的單人露營者、追求舒適住宿的情侶以及需要緊湊實用解決方案的小家庭的青睞。它們兼具寬敞的內部空間和便攜性,背包式帳篷重量為3-6磅,自駕露營式帳篷重量為8-12磅。居住占地面積通常長7-8英尺,寬4.5-5.5英尺,足以容納兩名成人,或一名成人攜帶大量裝備。憑藉輕巧的重量、易於搭建和多功能性,這類帳篷始終處於消費者的首選地位。

預計到2025年,中國露營帳篷市場規模將達到4億美元,並在2035年之前以8.4%的複合年成長率成長。自從新冠疫情爆發以來,隨著國內消費者越來越接受露營這種安全休閒的活動,市場成長速度加快。主要城市的年輕都市區白領推動了對高品質帳篷的需求,而社群媒體平台也對人們追求理想露營的趨勢產生了顯著影響。中國消費者展現出對高階裝備的投資意願,為國內外品牌拓展市場佔有率創造了機會。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 帳篷設計和材料的技術進步

- 可支配所得增加與消費者生活方式的改變

- 豪華露營和高階露營市場的擴張

- 產業潛在風險與挑戰

- 季節性需求波動和對天氣的依賴

- 激烈的市場競爭和價格敏感性

- 機會

- 豪華露營市場的擴張

- 永續環保的帳篷創新

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 過去價格趨勢分析(2019-2024)

- 按玩家類型(高階/超值/經濟型)分類的定價策略

- 區域價格波動分析

- 需求價格彈性

- 監理情勢

- 波特的分析

- PESTEL 分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 生成式人工智慧的應用案例(設計最佳化、客戶服務、需求預測)

- 針對特定領域的實施藍圖

- 風險、限制和監管考量

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區與銷售形式(現代零售與傳統零售)分類的通路覆蓋率

- 最後一公里基礎設施差異和不斷變化的管道

- 電子商務滲透率與履約網路分析

- 專業零售店擴張現況及市場覆蓋率

- 消費者購買行為分析

- 人口趨勢(年齡、收入、地區)

- 心理細分(冒險型、家庭露營者、極簡主義者)

- 影響購買決策的因素(價格、重量、安裝便利性、品牌)

- 產品導入生命週期

- 首選分銷管道的分析

- 品牌忠誠度與轉換行為

- 網路評論和社群媒體的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 圓頂帳篷

- 隧道帳篷

- 測地帳篷

- 帳篷小屋

- 輕便背包帳篷

- 彈出式/速開帳篷

- 其他

第6章 市場估計與預測:依產能分類,2022-2035年

- 1人份

- 2人

- 3-4人

- 5-8人

- 8人或以上

第7章 市場估計與預測:依價格分類,2022-2035年

- 價格低廉(100美元以下)

- 中價位(100-300美元)

- 高級版(300-600美元)

- 豪華/高性能(超過 600 美元)

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 個人

- 商業的

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場

- 專賣店

- 其他(百貨公司等)

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Big Agnes

- Coleman Company, Inc.

- Decathlon/Quechua

- Heimplanet

- Hyperlite Mountain Gear

- iKamper

- Lotus Belle

- Marmot

- MSR

- Naturehike

- Nemo Equipment, Inc.

- Ozark Trail

- REI Co-op

- Snow Peak

- The North Face

- Vango

- Zpacks

The Global Camping Tent Market was valued at USD 4.4 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 8.8 billion by 2035.

The market is benefiting from an increased focus on experiential travel and wellness-oriented outdoor activities, fueled by post-pandemic lifestyle shifts. Consumers are gravitating toward socially distanced, nature-based leisure experiences that enhance mental well-being and foster family connections. Rising interest in adventure travel, including hiking, trekking, and wildlife exploration, has created higher demand for durable, lightweight, and versatile camping gear. Government support for outdoor recreation, including funding for public lands and eco-tourism initiatives, has also contributed to market expansion. The market is witnessing innovation in tent designs, materials, and ease of assembly, while portable and performance-driven solutions are increasingly preferred. As camping becomes more popular across urban and rural populations, manufacturers are emphasizing comfort, durability, and efficiency in product offerings to meet evolving consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.4 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 7.1% |

The dome tents segment generated USD 1.5 billion in 2025, owing to their versatile, user-friendly design. Their curved pole structure provides stability, effective wind resistance, and lightweight portability, making them suitable for a wide range of camping scenarios. Three-season dome tents are the most common, offering ventilation for warm weather, moderate rain protection, and structural durability for typical wind conditions. Their ease of setup and relatively low weight, typically 4-7 pounds for 2-person models, make them accessible to novice and experienced campers alike, while their affordability strengthens adoption across the market.

The 2-person tent segment held a 40% share in 2025. These tents appeal to solo campers seeking extra space for gear, couples looking for comfortable accommodations, and small families needing compact yet functional solutions. They offer a practical balance between livable interior space and portability, with backpacking models weighing 3-6 pounds and car camping variants weighing 8-12 pounds. Floor dimensions generally range from 7-8 feet in length and 4.5-5.5 feet in width, providing adequate room for two adults or one adult with substantial gear. The combination of manageable weight, ease of setup, and versatile usage keeps this segment at the forefront of consumer preference.

China Camping Tent Market generated USD 400 million in 2025 and is expected to grow at a CAGR of 8.4% through 2035. Market growth accelerated after the COVID-19 pandemic as domestic consumers increasingly embraced camping as a safe and leisure-oriented activity. Young urban professionals in major cities have driven demand for high-quality tents, while social media platforms significantly influence aspirational camping trends. Chinese consumers are showing a willingness to invest in premium equipment, creating opportunities for both international and domestic brands to expand their market presence.

Key players in the Global Camping Tent Market include Coleman Company, Inc., MSR, Marmot, Heimplanet, Naturehike, Nemo Equipment, Inc., Big Agnes, Snow Peak, Vango, Hyperlite Mountain Gear, REI Co-op, Ozark Trail, Lotus Belle, Zpacks, The North Face, Decathlon / Quechua, and iKamper.Companies in the Camping Tent Market are leveraging product innovation, brand differentiation, and expanded distribution to strengthen their market foothold. Manufacturers focus on developing lightweight, modular, and high-durability tents while integrating new materials and performance-enhancing technologies. Strategic collaborations, partnerships with outdoor retailers, and e-commerce channel expansion enable broader reach to urban and adventure-focused consumers. Firms are investing in marketing campaigns emphasizing lifestyle and wellness benefits, supported by social media influencers and experiential events to boost brand engagement. Product diversification, including specialized tent designs for backpacking, family camping, and adventure sports, along with premium and eco-friendly offerings, further enhances competitiveness and market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Capacity

- 2.2.4 Price

- 2.2.5 End use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in tent design and materials

- 3.2.1.2 Rising disposable incomes and changing consumer lifestyles

- 3.2.1.3 Expansion of glamping and premium camping segments

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Seasonal demand fluctuations and weather dependence

- 3.2.2.2 Intense market competition and price sensitivity

- 3.2.3 Opportunities

- 3.2.3.1 Glamping market expansion

- 3.2.3.2 Sustainable & eco-friendly tent innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2019-2024)

- 3.6.2 Pricing strategy by player type (premium/value/budget)

- 3.6.3 Regional price variation analysis

- 3.6.4 Price elasticity of demand

- 3.7 Regulatory landscape

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases (design optimization, customer service, demand forecasting)

- 3.10.3 Adoption roadmap by segment

- 3.10.4 Risks, limitations & regulatory considerations

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs. traditional trade)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.11.3 E-commerce penetration & fulfillment network analysis

- 3.11.4 Specialty retail footprint & market coverage

- 3.12 Consumer buying behavior analysis

- 3.12.1 Demographic trends (age, income, geography)

- 3.12.2 Psychographic segmentation (adventure seekers, family campers, minimalists)

- 3.12.3 Factors affecting buying decisions (price, weight, setup ease, brand)

- 3.12.4 Product adoption lifecycle

- 3.12.5 Preferred distribution channel analysis

- 3.12.6 Brand loyalty & switching behavior

- 3.12.7 Online review & social media influence

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Dome tents

- 5.3 Tunnel tents

- 5.4 Geodesic tents

- 5.5 Cabin tents

- 5.6 Backpacking/lightweight tents

- 5.7 Pop-up/instant tents

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Solo (1 Person)

- 6.3 2 Persons

- 6.4 3-4 Persons

- 6.5 5-8 Persons

- 6.6 Above 8 Persons

Chapter 7 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (Under $100)

- 7.3 Mid-range ($100-$300)

- 7.4 Premium ($300-$600)

- 7.5 Luxury/high-performance ($600+)

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Supermarkets

- 9.3.2 Specialty Stores

- 9.3.3 Others (departmental stores, etc.)

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Big Agnes

- 11.2 Coleman Company, Inc.

- 11.3 Decathlon / Quechua

- 11.4 Heimplanet

- 11.5 Hyperlite Mountain Gear

- 11.6 iKamper

- 11.7 Lotus Belle

- 11.8 Marmot

- 11.9 MSR

- 11.10 Naturehike

- 11.11 Nemo Equipment, Inc.

- 11.12 Ozark Trail

- 11.13 REI Co-op

- 11.14 Snow Peak

- 11.15 The North Face

- 11.16 Vango

- 11.17 Zpacks

露營帳篷市場:2026-2032年全球市場預測(依產品類型、容量、季節性、材料、搭建方式、銷售管道及應用分類)帳篷配件市場:按產品類型、材料、最終用戶、分銷管道和應用分類-2026-2032年全球預測

露營帳篷市場:2026-2032年全球市場預測(依產品類型、容量、季節性、材料、搭建方式、銷售管道及應用分類)帳篷配件市場:按產品類型、材料、最終用戶、分銷管道和應用分類-2026-2032年全球預測 露營帳篷市場規模、佔有率、趨勢和預測:按帳篷類型、容量、應用、銷售管道和地區分類,2026-2034年露營拖車帳篷市場:全球預測(2026-2032 年),按季節性、產品類型、搭建方式、材料和銷售管道管道分類

露營帳篷市場規模、佔有率、趨勢和預測:按帳篷類型、容量、應用、銷售管道和地區分類,2026-2034年露營拖車帳篷市場:全球預測(2026-2032 年),按季節性、產品類型、搭建方式、材料和銷售管道管道分類 全球露營帳篷市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球露營帳篷市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 露營帳篷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、銷售管道、地區和競爭格局分類,2021-2031年帳篷市場按產品類型、容量、最終用戶、通路和材料分類-2026-2032年全球預測沙灘帳篷市場依產品類型、通路、材料及產能分類-2026年至2032年全球預測

露營帳篷市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、銷售管道、地區和競爭格局分類,2021-2031年帳篷市場按產品類型、容量、最終用戶、通路和材料分類-2026-2032年全球預測沙灘帳篷市場依產品類型、通路、材料及產能分類-2026年至2032年全球預測 全球充氣穹頂市場

全球充氣穹頂市場 軟硬混合車頂帳篷市場報告:2031 年趨勢、預測與競爭分析

軟硬混合車頂帳篷市場報告:2031 年趨勢、預測與競爭分析