|

市場調查報告書

商品編碼

2019252

豬疫苗市場商機、成長要素、產業趨勢分析及2026-2035年預測。Swine Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

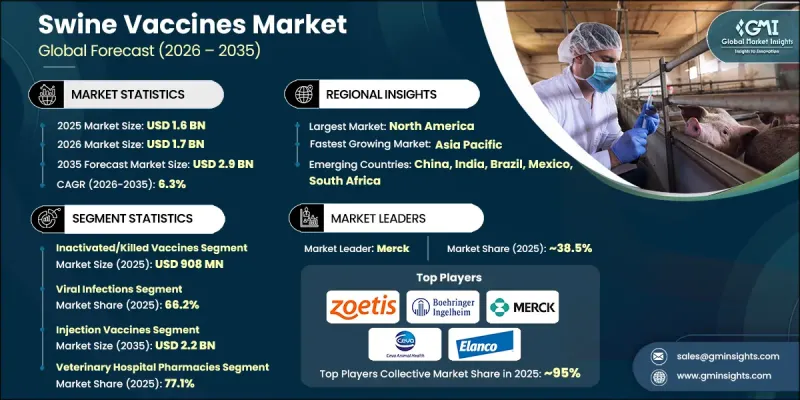

預計到 2025 年,全球豬隻疫苗市場價值將達到 16 億美元,並有望以 6.3% 的複合年成長率成長,到 2035 年達到 29 億美元。

全球市場對豬肉及相關產品的需求不斷成長,推動了市場成長,進而促使人們更加重視維護牲畜健康和提高生產力。豬疫苗在保護豬隻方面發揮著至關重要的作用,它能活化豬的免疫系統,使其免受包括病毒、細菌和其他病原體在內的多種傳染性病原體的侵害。人口成長、都市化進程加快以及飲食習慣的改變,推動了畜牧業的持續擴張,也進一步刺激了對有效動物保健解決方案的需求。隨著生產系統集約化程度的提高,生產者越來越重視動物保健措施。疫苗接種正成為降低疾病風險、提高存活率和保護經濟利益的關鍵策略。此外,對糧食安全的擔憂也促使人們採用先進的疾病預防措施,這進一步推動了豬隻疫苗市場的成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 16億美元 |

| 預測金額 | 29億美元 |

| 複合年成長率 | 6.3% |

去活化疫苗市場地位強勁,2025年銷售額達9.08億美元。這類疫苗因其安全性高、穩定性佳而廣受歡迎。其保存期限長、儲存條件相對簡單,使其適用於大規模免疫接種計劃。因此,去活化疫苗仍然是控制豬群常見疾病的可靠選擇。

預計到2025年,病毒感染疾病細分市場將佔據66.2%的市場佔有率,並在2026年至2035年間以6.4%的複合年成長率成長。該細分市場的成長主要受豬群病毒性疾病的廣泛流行及其經濟影響的驅動。這些感染疾病具有高度傳染性,會對動物健康、生產力和農場整體盈利造成重大影響。在高密度飼養環境中,感染的快速傳播進一步凸顯了疫苗接種作為主要預防措施的重要性,從而鞏固了該細分市場的主導地位。

預計北美豬疫苗市場規模將在2025年達到6.826億美元,到2035年將達到12億美元,2026年至2035年間的複合年成長率(CAGR)為5.8%。該地區的主導地位得益於先進的畜牧管理系統、完善的獸醫基礎設施以及對優質豬肉產品的強勁需求。美國憑藉其大規模的生豬生產能力以及在國內消費和出口方面的重要地位,仍然是該地區的主要貢獻者。持續重視疾病預防以及主要企業的存在,進一步鞏固了該地區強勁的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 通用感染疾病發生率增加

- 畜牧業的擴張以及人們對糧食安全的擔憂

- 疫苗技術的進步

- 動物疾病發生率增加

- 產業潛在風險與挑戰

- 高昂的研發成本和漫長的研發週期

- 低溫運輸基礎設施的限制因素

- 監理複雜性和核准延誤

- 市場機遇

- mRNA和下一代平台的採用

- 耐熱疫苗的研發

- 聯合疫苗創新

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 疫苗技術的演進與創新

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 專利分析(基於初步研究)

- 臨床試驗和研發管線分析(基於初步調查)

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 活病毒疫苗

- 去活化疫苗

- 病毒載體疫苗

- 藥效疫苗

- 其他疫苗

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 細菌感染疾病

- 病毒感染疾病

- 寄生蟲感染疾病

- 其他用途

第7章 市場估計與預測:依給藥途徑分類,2022-2023年

- 注射疫苗

- 口服疫苗

- 浸泡式和噴灑式疫苗

第8章 市場估算與預測:依通路分類,2022-2035年

- 獸藥

- 普通藥房

- 電子商務

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Addison Biological Laboratory

- Bioveta

- Boehringer Ingelheim

- Ceva Sante Animale

- Colorado Serum Company

- Elanco Animal Health Incorporated

- HIPRA SA

- Indian Immunologicals

- Merck

- Biogenesis Bago

- Vaxxinova(EW Group)

- Vibac

- Zoetis

The Global Swine Vaccines Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 2.9 billion by 2035.

Market growth is driven by the increasing demand for pork and related products across global markets, which is placing greater emphasis on maintaining herd health and improving productivity. Swine vaccines play a critical role in protecting pigs by activating their immune systems to defend against a range of infectious agents, including viruses, bacteria, and other pathogens. The ongoing expansion of the livestock sector, fueled by population growth, urbanization, and evolving dietary habits, continues to accelerate demand for effective animal healthcare solutions. As production systems become more intensive to enhance output and efficiency, producers are placing stronger focus on preventive healthcare practices. Vaccination is emerging as a key strategy to reduce disease risks, improve survival rates, and protect economic returns. In addition, concerns related to food security are encouraging the adoption of advanced disease prevention measures, further supporting the growth of the swine vaccines market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.3% |

The inactivated or killed vaccines segment generated USD 908 million in 2025, reflecting its strong position in the market. These vaccines are widely preferred due to their established safety profile and stability. Their extended shelf life and relatively straightforward storage requirements make them suitable for large-scale immunization programs. As a result, they continue to be a reliable option for managing commonly occurring diseases in swine populations.

The viral infections segment accounted for 66.2% share in 2025 and is expected to grow at a CAGR of 6.4% during 2026-2035. This segment's growth is driven by the widespread presence and economic impact of viral diseases affecting swine populations. Such infections are highly transmissible and can significantly affect animal health, productivity, and overall farm profitability. Their rapid spread in high-density farming environments reinforces the importance of vaccination as a primary preventive approach, supporting the segment's dominant position.

North America Swine Vaccines Market captured USD 682.6 million in 2025 and is projected to reach USD 1.2 billion by 2035, growing at a CAGR of 5.8% between 2026 and 2035. The region's leadership is supported by advanced livestock management systems, well-developed veterinary healthcare infrastructure, and strong demand for high-quality pork production. The United States remains a major contributor due to its large-scale swine production capacity and significant role in both domestic consumption and exports. Continued focus on disease prevention and the presence of leading animal health companies further reinforce the region's strong market position.

Key players operating in the Global Swine Vaccines Market include Zoetis, Merck, Boehringer Ingelheim, Elanco Animal Health Incorporated, Ceva Sante Animale, HIPRA S.A., Biogenesis Bago, Vaxxinova (EW Group), Indian Immunologicals, Bioveta, Vibac, Colorado Serum Company, and Addison Biological Laboratory. Companies in the swine vaccines market are strengthening their market position through continuous research and development, strategic partnerships, and expansion into emerging regions. They are focusing on developing advanced vaccines with improved efficacy, broader protection, and enhanced safety profiles. Collaborations with veterinary service providers and livestock producers are helping companies expand their reach and improve product adoption. In addition, manufacturers are investing in production capacity expansion and supply chain optimization to ensure consistent availability. Companies are also emphasizing regulatory compliance and quality standards while exploring innovative vaccine technologies to address evolving disease challenges and maintain a competitive edge in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of zoonotic diseases

- 3.2.1.2 Expanding livestock industry and food security concerns

- 3.2.1.3 Advancements in vaccine technology

- 3.2.1.4 Increasing outbreaks of animal diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D costs & long development timelines

- 3.2.2.2 Cold chain infrastructure limitations

- 3.2.2.3 Regulatory complexity & approval delays

- 3.2.3 Market opportunities

- 3.2.3.1 mRNA & next-generation platform adoption

- 3.2.3.2 Thermostable vaccine development

- 3.2.3.3 Combination vaccine innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Vaccine technology evolution and innovation

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Clinical trial/pipeline analysis (Driven by Primary Research)

- 3.9 Future market trends

- 3.10 Impact of AI & generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Live attenuated vaccines

- 5.3 Inactivated/killed vaccines

- 5.4 Viral vector vaccines

- 5.5 mRNA vaccines

- 5.6 Other vaccines

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Bacterial infections

- 6.3 Viral infections

- 6.4 Parasitic infections

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 203($ Mn)

- 7.1 Key trends

- 7.2 Injection vaccines

- 7.3 Oral vaccines

- 7.4 Immersion/spray vaccines

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 UAE

Chapter 10 Company Profiles

- 10.1 Addison Biological Laboratory

- 10.2 Bioveta

- 10.3 Boehringer Ingelheim

- 10.4 Ceva Sante Animale

- 10.5 Colorado Serum Company

- 10.6 Elanco Animal Health Incorporated

- 10.7 HIPRA S.A.

- 10.8 Indian Immunologicals

- 10.9 Merck

- 10.10 Biogenesis Bago

- 10.11 Vaxxinova (EW Group)

- 10.12 Vibac

- 10.13 Zoetis

豬疫苗市場-2026-2032年全球市場預測

豬疫苗市場-2026-2032年全球市場預測 豬疫苗市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、類型、目標疾病、地區和競爭格局分類,2021-2031年

豬疫苗市場-全球產業規模、佔有率、趨勢、機會和預測:按產品、類型、目標疾病、地區和競爭格局分類,2021-2031年 豬隻疫苗市場規模、佔有率和成長分析:按疫苗類型、疾病類型、給藥途徑、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

豬隻疫苗市場規模、佔有率和成長分析:按疫苗類型、疾病類型、給藥途徑、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 豬隻保健市場規模、佔有率、趨勢和預測:按產品、疾病、給藥途徑、分銷管道和地區分類,2026-2034 年

豬隻保健市場規模、佔有率、趨勢和預測:按產品、疾病、給藥途徑、分銷管道和地區分類,2026-2034 年 全球豬疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)豬保健市場-全球產業規模、佔有率、趨勢、機會及按類型、疾病、地區和競爭格局分類的預測(2021-2031年)

全球豬疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)豬保健市場-全球產業規模、佔有率、趨勢、機會及按類型、疾病、地區和競爭格局分類的預測(2021-2031年) 全球豬隻疫苗市場:市場規模、佔有率、趨勢分析(按產品、類型、給藥途徑和地區)、細分市場預測(2025-2030 年)

全球豬隻疫苗市場:市場規模、佔有率、趨勢分析(按產品、類型、給藥途徑和地區)、細分市場預測(2025-2030 年)