|

市場調查報告書

商品編碼

2019246

大型自動駕駛汽車市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Heavy-Duty Autonomous Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球大型自動駕駛汽車市場價值458億美元,預計2035年將以15.7%的複合年成長率成長至1815億美元。

隨著對先進安全系統的需求不斷成長,以及人們對自動駕駛技術的興趣日益濃厚,交通運輸行業正在經歷一場變革,而大型自動駕駛汽車領域也展現出強勁的發展勢頭。先進的車輛擴大配備了精密的感測器和智慧軟體,能夠即時分析周圍環境並快速做出駕駛決策。這些功能預計將顯著減少交通事故,降低傷亡人數,並最大限度地減少對基礎設施和車輛的損害,最終降低營運成本,提高道路安全。自動化技術的持續創新和智慧運輸解決方案的整合進一步推動了市場的擴張。隨著技術的不斷普及,市場正朝著更可靠、高效和擴充性的自動駕駛系統發展,以應對大規模交通應用中的安全和營運挑戰。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 458億美元 |

| 預測金額 | 1815億美元 |

| 複合年成長率 | 15.7% |

大規模自動駕駛汽車市場的發展也得益於業界強力的合作與夥伴關係關係,以支持不斷成長的商業需求。新冠疫情為該行業帶來了挑戰和機遇。 2020年初,封鎖措施、供應鏈中斷和半導體短缺減緩了研發活動,並推遲了先進自動駕駛和電動車解決方案的推出。此外,由於物流業者優先考慮維持基本營運和解決勞動力短缺問題,而非投資新技術,許多試點計畫被迫暫停。

預計到2025年,卡車運輸業將佔據70%的市場佔有率,並在2026年至2035年間以14.8%的複合年成長率成長。卡車在物流、工業和資源相關行業的廣泛應用支撐了這一市場主導地位。卡車運輸自動化解決了人手不足、營運成本高和安全隱患等關鍵挑戰。自動駕駛卡車透過實現連續運作、提高燃油效率和縮短配送週期,從而提高了生產效率。感測器系統和智慧導航技術的進步也提高了在路況良好的道路上的駕駛精度和運行可靠性。

預計2025年,內燃機(ICE)汽車市場規模將達231億美元。由於內燃機汽車初始成本低、加油基礎設施完善,支援在各種環境下進行測試和部署,因此仍被廣泛使用。此外,其長續航里程也使其適用於長途營運和各種測試場景,從而支援自動駕駛汽車領域的持續發展。

預計到2025年,美國大型自動駕駛汽車市場規模將達127億美元。這一成長主要得益於監管機構對自動駕駛汽車測試和部署日益成長的關注,以及旨在實現安全和高效部署的政府框架的發展。除了消費者對安全性和便利性的期望不斷提高外,對更有效率交通系統的需求也推動了市場擴張。此外,人們越來越認知到,這些車輛是緩解道路擁塞和提高整體交通安全的潛在解決方案。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 感測器和感知技術供應商

- 自動駕駛軟體和人工智慧堆疊

- 連接和遠端資訊處理提供者

- 改裝和整合供應商

- 成本結構

- 利潤率

- 每個階段增加的價值

- 垂直整合趨勢

- 顛覆者

- 供應商情況

- 影響因素

- 促進因素

- 5G和高速連線的普及

- 對車輛安全和車載資訊服務的需求日益成長

- 政府關於車輛互聯的法規

- 智慧運輸和數位服務的廣泛應用

- 產業潛在風險與挑戰

- 網路安全和資料隱私問題

- 連接硬體和整合高成本。

- 市場機遇

- 擴大空中下載 (OTA) 軟體更新的範圍

- V2X通訊技術的整合

- 數據驅動型行動平台的成長

- 將人工智慧和雲端平台整合到車輛中

- 促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 新興技術

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 專利分析(基於初步研究)

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按玩家類型分類的定價策略

- 生產統計

- 生產基地

- 消費中心

- 進出口

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 預測性維護和營運最佳化

- 自動化設計最佳化

- 用於需求預測的供應鏈人工智慧

- GenAI 各細分市場的應用案例與部署藍圖

- 胎面花紋設計與生成

- 客戶服務聊天機器人和技術支援

- 行銷內容創作

- 風險、限制和監管考量

- 物聯網智慧產品中的資料隱私

- 人工智慧演算法的透明度要求

- 人工智慧驅動的產品故障責任

- 利用人工智慧改造現有經營模式

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 追蹤

- 七年級

- 八年級

- 公車

第6章 市場估價與預測:依自動駕駛等級分類,2022-2035年

- 一級

- 二級

- 3級

- 4級

第7章 市場估計與預測:依實施法分類,2022-2035年

- 內燃機(ICE)

- 電動車

- 混合動力汽車

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 後勤

- 建築和採礦

- 運輸

- 其他

第9章 市場估計與預測:依最終用途分類,2022-2035年

- OEM

- 售後市場

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 北歐的

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- 世界公司

- Baidu

- Scania

- Daimler Truck

- Einride

- PACCAR

- TRATON

- Volvo

- ZF Friedrichshafen

- Waymo

- 本地球員

- 2getthere

- Navya ARMA

- New Flyer

- FAW

- Aurora

- Embark Trucks

- 新興企業

- Kodiak Robotics

- Oxa Autonomy

- Torc Robotics

- TuSimple

- Zoox

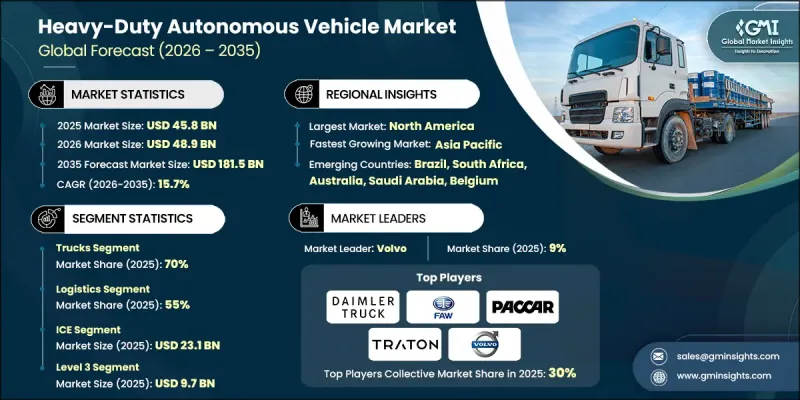

The Global Heavy-Duty Autonomous Vehicle Market was valued at USD 45.8 billion in 2025 and is estimated to grow at a CAGR of 15.7% to reach USD 181.5 billion by 2035.

The heavy-duty autonomous vehicle industry is gaining strong momentum as demand for enhanced safety systems and growing interest in self-driving technologies reshape the transportation landscape. Advanced vehicles are increasingly equipped with sophisticated sensors and intelligent software that can analyze their surroundings in real-time and make rapid driving decisions. These capabilities are expected to significantly reduce accidents, lower the number of injuries and fatalities, and minimize damage to infrastructure and vehicles, ultimately leading to reduced operational costs and improved road safety. Market expansion is further supported by continuous innovation in automation technologies and the integration of smart mobility solutions. As adoption increases, the market is evolving toward more reliable, efficient, and scalable autonomous systems that address both safety and operational challenges across heavy-duty transport applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.8 Billion |

| Forecast Value | $181.5 Billion |

| CAGR | 15.7% |

The heavy-duty autonomous vehicle market is also influenced by the need for strong industry collaboration and partnerships to support rising commercial demand. The COVID-19 pandemic created both challenges and opportunities for the industry. During the early stages of 2020, lockdown measures, supply chain disruptions, and semiconductor shortages slowed development activities and delayed the introduction of advanced autonomous and electric vehicle solutions. In addition, many pilot programs were temporarily halted as logistics providers prioritized maintaining essential operations and managing workforce constraints, rather than investing in new technology initiatives.

The trucks segment held a 70% share in 2025 and is projected to grow at a CAGR of 14.8% from 2026 to 2035. This dominance is driven by the extensive use of trucks across logistics, industrial, and resource-based sectors. Automation in trucking addresses critical challenges such as labor shortages, high operating expenses, and safety concerns. Autonomous trucks offer continuous operation, improved fuel efficiency, and faster delivery cycles, contributing to higher productivity. Advancements in sensor systems and intelligent navigation technologies are also improving driving precision and operational reliability under structured road conditions.

The ICE segment reached USD 23.1 billion in 2025. Internal combustion engine vehicles remain widely used due to their lower initial cost and well-established refueling infrastructure, which supports testing and deployment across multiple environments. Their extended driving range also makes them suitable for long-distance operations and diverse testing scenarios, supporting ongoing development in the autonomous vehicle space.

U.S. Heavy-Duty Autonomous Vehicle Market generated USD 12.7 billion in 2025. Growth is supported by increasing regulatory focus on autonomous vehicle testing and deployment, with government frameworks aimed at enabling safe and efficient adoption. Rising consumer expectations for safety and convenience, along with the need for more efficient transportation systems, are contributing to market expansion. Additionally, these vehicles are being recognized as a potential solution for reducing road congestion and improving overall traffic safety.

Key players operating in the Global Heavy-Duty Autonomous Vehicle Market include PACCAR, Volvo, Daimler Truck, TRATON, FAW, SAIC, JAC, Baidu, Waymo, and ZF Friedrichshafen. Companies in the Heavy-Duty Autonomous Vehicle Market are strengthening their market position through continuous technological advancement and strategic collaboration. They are investing in research and development to enhance autonomous driving capabilities, sensor accuracy, and system reliability. Partnerships with technology providers and logistics companies are enabling faster innovation and real-world deployment. Businesses are also focusing on scalable vehicle platforms and software integration to improve operational efficiency and reduce costs. Expanding testing programs and improving regulatory alignment are key priorities to accelerate commercialization. In addition, companies are enhancing production capabilities and optimizing supply chains to meet growing demand, while aligning product offerings with evolving industry requirements to maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Level of Autonomy

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Sensor & Perception Suppliers

- 3.1.1.2 Autonomous Driving Software & AI Stack

- 3.1.1.3 Connectivity & Telematics Providers

- 3.1.1.4 Retrofit & Integration Suppliers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of 5G and high-speed connectivity

- 3.2.1.2 Growing demand for vehicle safety and telematics

- 3.2.1.3 Government mandates for vehicle connectivity

- 3.2.1.4 Rising adoption of smart mobility and digital services

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Cybersecurity and data privacy concerns

- 3.2.2.2 High cost of connectivity hardware and integration

- 3.2.3 Market opportunities

- 3.2.3.1 Over-the-air (OTA) software updates expansion

- 3.2.3.2 Integration of V2X communication technologies

- 3.2.3.3 Growth of data-driven mobility platforms

- 3.2.3.4 Integration of AI and cloud platforms in vehicles

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 MEA

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.1.1 Predictive Maintenance & Operations Optimization

- 3.13.1.2 Automated design optimization

- 3.13.1.3 Supply chain AI for demand forecasting

- 3.13.1.4 GenAI use cases & adoption roadmap by segment

- 3.13.1.4.1 Tread pattern design generation

- 3.13.1.4.2 Customer service chatbots & technical support

- 3.13.1.4.3 Marketing content creation

- 3.13.1.4.4 Risks, limitations & regulatory considerations

- 3.13.1.4.4.1 Data privacy in IoT-enabled smart products

- 3.13.1.4.4.2 AI algorithm transparency requirements

- 3.13.1.4.4.3 Liability in AI-driven product failures

- 3.13.1 AI-driven disruption of existing business models

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Trucks

- 5.2.1 Class 7

- 5.2.2 Class 8

- 5.3 Buses

Chapter 6 Market Estimates & Forecast, By Level of Autonomy, 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Level 1

- 6.3 Level 2

- 6.4 Level 3

- 6.5 Level 4

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicle

- 7.4 Hybrid vehicle

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Logistics

- 8.3 Construction & Mining

- 8.4 Transportation

- 8.5 Others

Chapter 9 Market Estimates & Forecast By End use, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Nordic

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East & Africa

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Baidu

- 11.1.2 Scania

- 11.1.3 Daimler Truck

- 11.1.4 Einride

- 11.1.5 PACCAR

- 11.1.6 TRATON

- 11.1.7 Volvo

- 11.1.8 ZF Friedrichshafen

- 11.1.9 Waymo

- 11.2 Regional players

- 11.2.1 2getthere

- 11.2.2 Navya ARMA

- 11.2.3 New Flyer

- 11.2.4 FAW

- 11.2.5 Aurora

- 11.2.6 Embark Trucks

- 11.3 Emerging players

- 11.3.1 Kodiak Robotics

- 11.3.2 Oxa Autonomy

- 11.3.3 Torc Robotics

- 11.3.4 TuSimple

- 11.3.5 Zoox

2026年全球大型自動駕駛汽車市場報告

2026年全球大型自動駕駛汽車市場報告 大型自動駕駛汽車市場:按組件、自動駕駛等級、動力傳動系統、部署模式、應用和車輛類型分類-2026-2032年全球市場預測卡車自動駕駛系統市場:按自動駕駛等級、組件、卡車類型、應用和最終用戶產業分類-全球預測,2026-2032年

大型自動駕駛汽車市場:按組件、自動駕駛等級、動力傳動系統、部署模式、應用和車輛類型分類-2026-2032年全球市場預測卡車自動駕駛系統市場:按自動駕駛等級、組件、卡車類型、應用和最終用戶產業分類-全球預測,2026-2032年 重型自動駕駛汽車市場:市場洞察、競爭格局及預測(2033 年)

重型自動駕駛汽車市場:市場洞察、競爭格局及預測(2033 年) 歐洲重型自動駕駛汽車市場按應用、推進系統、車輛類型、自動駕駛等級、感測器類型和國家分類的分析與預測(2024 年至 2033 年)

歐洲重型自動駕駛汽車市場按應用、推進系統、車輛類型、自動駕駛等級、感測器類型和國家分類的分析與預測(2024 年至 2033 年) 重型自動駕駛汽車市場 - 全球和區域分析:按應用、推進系統、車輛類型、自動駕駛水平、感測器類型和區域 - 分析和預測(2024-2033 年)

重型自動駕駛汽車市場 - 全球和區域分析:按應用、推進系統、車輛類型、自動駕駛水平、感測器類型和區域 - 分析和預測(2024-2033 年)