|

市場調查報告書

商品編碼

2019212

無線印表機市場商機、成長要素、產業趨勢分析及2026-2035年預測。Wireless Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

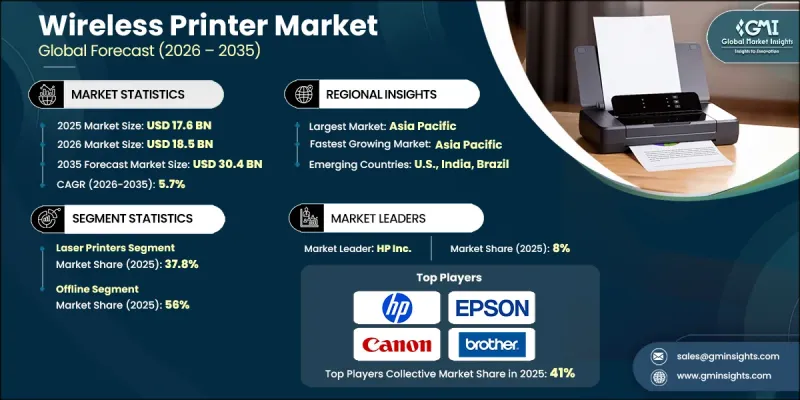

預計到 2025 年,全球無線印表機市場規模將達到 176 億美元,並以 5.7% 的複合年成長率成長,到 2035 年將達到 304 億美元。

市場成長的驅動力在於連接性、行動整合和成像技術的持續創新。領先的印表機製造商正在將高速 Wi-Fi 6/7、低功耗藍牙和 NFC 整合到其噴墨、雷射和熱敏產品中,從而在商用和工業應用中實現無線操作和高速資料傳輸。產業重組,包括併購以及與軟體和雲端解決方案供應商的合作,也在推動市場擴張。這些合作關係為企業級無線列印和託管列印服務提供了支援。從傳統的有線列印轉向雲端按需數位解決方案正在改變企業的營運方式,而人工智慧驅動的列印管理、多裝置同步和混合雲端列印正在重新定義工作流程的效率和可自訂性,從而滿足高印量辦公環境和工業列印的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 176億美元 |

| 預測金額 | 304億美元 |

| 複合年成長率 | 5.7% |

到2025年,雷射印表機市場佔有率將達到37.8%。雷射印表機憑藉其高速列印、在大規模辦公室和企業營運中的成本效益以及強大的無線安全協議,持續保持主導地位,成為高印量企業的理想之選。此外,雷射印表機還能與行動和雲端解決方案整合,進一步增強了其對尋求可靠高效列印解決方案的企業的吸引力。

線下銷售通路佔56%,市場規模達98億美元。線下通路表現依然強勁,尤其是在商業和企業環境中,這得益於現場演示、專業安裝服務以及訂閱式墨水和碳粉填充計劃等優勢。此外,客戶更傾向於離線購買,因為他們可以立即獲得產品和個人化支持,從而提升整體購買體驗。

預計到2025年,美國無線印表機市佔率將達到80.5%。該地區正受益於混合辦公模式、雲端整合辦公室基礎設施和行動優先列印解決方案的日益普及。企業辦公室、教育機構和醫療機構對無線印表機的日益青睞,以及其對雲端列印、行動裝置連接和安全遠端管理的支持,正在推動該地區強勁的需求,並鞏固美國作為無線印表機普及領先市場中心的地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 勞動力短缺加劇和製造業回流

- 人工智慧、衍生設計和軟體整合

- IT/OT在印刷作業中的整合

- 產業潛在風險與挑戰

- 高整合複雜性

- 資料隱私和網路安全

- 機會

- Printing-as-a-Service(PaaS)

- 印刷電子和智慧包裝的成長

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 專利趨勢(基於初步調查)

- 無線技術專利(Wi-Fi、藍牙、NFC)

- 與印刷安全和加密相關的專利

- 與雲端列印基礎設施相關的專利

- 與多功能設備整合相關的專利

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的列印管理和預測性維護

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 基礎設施和實施情況(基於初步調查)

- 按地區和購買者群體分類的採用率和滲透率(基於初步調查)

- 基礎設施投資的可擴展性限制和趨勢(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 噴墨印表機

- 雷射印表機

- 3D印表機

- 其他(熱感式印表機、熱昇華印表機、可攜式/行動印表機等)

第6章 市場估計與預測:依功能分類,2022-2035年

- 單功能印表機

- 多功能印表機

第7章 市場估計與預測:以連結方式分類,2022-2035年

- Wi-Fi

- Bluetooth

- 雲端列印

- 其他(近距離場通訊 (NFC) 相容印表機、AirPrint 等)

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 公司總部

- 衛生保健

- 教育

- 飯店業

- 政府

- 其他(旅館業、活動策劃公司等)

- 工業的

第9章 市場估計與預測:依價格分類,2022-2035年

- 低的

- 中等的

- 高的

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 公司經營的網站

- 離線

- 量販店

- 品牌自營店

- 其他(百貨公司)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Brother USA

- Canon

- Dell

- Epson

- HP

- Fujifilm

- Konica Minolta

- Kyocera

- Lexmark

- Oki

- Ricoh

- Roland

- Sharp

- Toshiba

- Xerox

The Global Wireless Printer Market was valued at USD 17.6 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 30.4 billion by 2035.

The market's growth is fueled by continuous innovation in connectivity, mobile integration, and imaging technologies. Leading printer manufacturers are incorporating high-speed Wi-Fi 6/7, Bluetooth Low Energy, and NFC into their inkjet, laser, and thermal products, enabling cable-free operation and fast data transfer for professional and industrial applications. Market expansion is also driven by industry consolidation, including mergers, acquisitions, and partnerships with software and cloud solution providers. These collaborations support enterprise-class wireless printing and managed print services. The shift from traditional cabled printing to cloud-enabled and on-demand digital solutions is reshaping operations, while AI-driven print management, multi-device synchronization, and hybrid cloud printing are redefining workflow efficiency and customization, catering to both high-volume office settings and industrial printing needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.6 Billion |

| Forecast Value | $30.4 Billion |

| CAGR | 5.7% |

In 2025, the laser printers segment accounted for a 37.8% share. Laser printers continue to lead because they offer high-speed printing, cost efficiency for large-scale office and enterprise operations, and robust wireless security protocols, making them the preferred choice for organizations handling high-volume printing tasks. Their ability to integrate with mobile and cloud-based solutions further strengthens their appeal among businesses seeking reliable and efficient printing solutions.

The offline sales segment held 56% share, valued at USD 9.8 billion. Offline channels continue to perform strongly, particularly in commercial and enterprise settings, due to the availability of hands-on demonstrations, professional installation services, and subscription-based ink and toner replenishment programs. Customers also favor offline purchases for immediate product access and personalized support, which enhances the overall buying experience.

United States Wireless Printer Market accounted for 80.5% share in 2025. The region benefits from widespread adoption of hybrid work models, cloud-integrated office infrastructure, and mobile-first printing solutions. Corporate offices, educational institutions, and healthcare facilities are increasingly deploying wireless printers that support cloud printing, mobile device connectivity, and secure remote management, driving strong regional demand and solidifying the U.S. as a key market hub for wireless printer adoption.

Key players in the Global Wireless Printer Market include Canon, HP, Lexmark, Fujifilm, Ricoh, Brother USA, Dell, Epson, Konica Minolta, Kyocera, Oki, Roland, Sharp, Toshiba, and Xerox. Companies in the Wireless Printer Market are strengthening their positions by investing heavily in R&D to integrate advanced connectivity, mobile solutions, and AI-enabled print management. Strategic partnerships with cloud service providers, mergers, and acquisitions help expand product portfolios and enterprise-grade managed printing services. OEMs are focusing on customer experience through subscription-based ink services, hybrid cloud integration, and multi-device compatibility. Innovation in wireless security, high-speed printing, and scalable solutions ensures a competitive edge, while direct-to-consumer and professional installation services improve brand visibility and market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Functionality

- 2.2.4 Connectivity

- 2.2.5 Price

- 2.2.6 Application

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Labor Shortages & Manufacturing Reshoring

- 3.2.1.2 AI, Generative Design & Software Integration

- 3.2.1.3 IT/OT Convergence in Printing Operations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Integration Complexity

- 3.2.2.2 Data Privacy & Cybersecurity

- 3.2.3 Opportunities

- 3.2.3.1 Printing-as-a-Service (PaaS)

- 3.2.3.2 Growth in Printed Electronics & Smart Packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.7 Patent Landscape (Driven by Primary Research)

- 3.7.1 Wireless Technology Patents (Wi-Fi, Bluetooth, NFC)

- 3.7.2 Print Security & Encryption Patents

- 3.7.3 Cloud Printing Infrastructure Patents

- 3.7.4 Multi-Function Device Integration Patents

- 3.8 Regulatory landscape

- 3.8.1 Standards and compliance requirements

- 3.8.2 Regional regulatory frameworks

- 3.8.3 Certification standards

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by Primary Research)

- 3.11.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Print Management & Predictive Maintenance

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.13.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.13.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Inkjet printer

- 5.3 Laser printer

- 5.4 3D printer

- 5.5 Others (Thermal printer, Dye-sublimation printer, Portable/Mobile printer, etc.)

Chapter 6 Market Estimates & Forecast, By Functionality, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Single-function printer

- 6.3 Multi-function printer

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wi-Fi

- 7.3 Bluetooth

- 7.4 Cloud printing

- 7.5 Others (Near Field Communication (NFC) Enabled printer, AirPrint, etc.)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Corporate offices

- 8.3.2 Healthcare

- 8.3.3 Educational

- 8.3.4 Hospitality

- 8.3.5 Government

- 8.3.6 Others (Hospitality, Events planners etc.)

- 8.4 Industrial

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce website

- 10.2.2 Company owned website

- 10.3 Offline

- 10.3.1 Electronics stores

- 10.3.2 Brand stores

- 10.3.3 Others (department stores)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Brother USA

- 12.2 Canon

- 12.3 Dell

- 12.4 Epson

- 12.5 HP

- 12.6 Fujifilm

- 12.7 Konica Minolta

- 12.8 Kyocera

- 12.9 Lexmark

- 12.10 Oki

- 12.11 Ricoh

- 12.12 Roland

- 12.13 Sharp

- 12.14 Toshiba

- 12.15 Xerox