|

市場調查報告書

商品編碼

2019207

血球比容測量設備市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Hematocrit Test Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

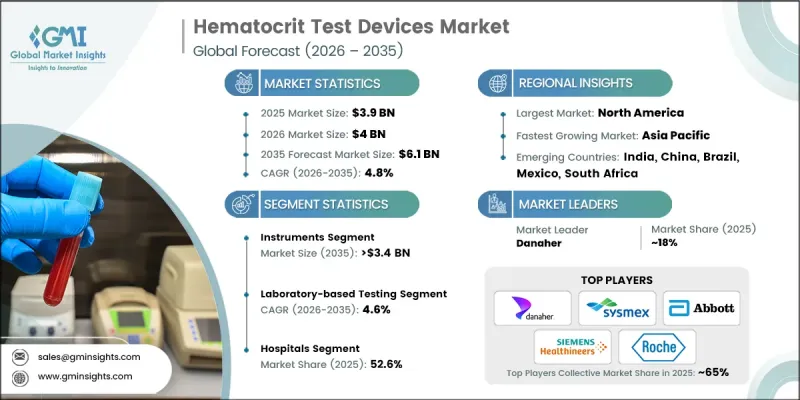

全球血球容積比檢測設備市場預計在 2025 年達到 39 億美元,預計到 2035 年將以 4.8% 的複合年成長率成長至 61 億美元。

市場成長主要受血液疾病盛行率上升、全球人口老化以及即時檢測技術不斷進步的驅動。血球容積比分析儀測量患者血液中紅血球佔總血容量的百分比,廣泛應用於醫院、診斷檢查室和即時檢測機構,用於監測貧血、脫水和其他血液疾病等狀況。現代設備整合了緊湊型設計、數位介面和自動化檢體處理功能,提高了檢測速度、準確性和操作效率。攜帶式和手持式血球容積比分析儀的快速普及使得醫護人員能夠在診所、急診室和門診進行床邊檢測。快速獲得檢測結果有助於臨床決策,支持創傷管理,改善患者預後,同時減少對中心檢查室的依賴。微流體技術和自動化血液檢測平台的創新,以及診斷準確性的不斷提高,進一步推動了該市場的發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 39億美元 |

| 預測金額 | 61億美元 |

| 複合年成長率 | 4.8% |

預計試劑和耗材領域在 2025 年的累計將達到 16 億美元,到 2035 年將以 5.4% 的複合年成長率成長。對試劑、微毛細管和試劑盒的需求受到血球比容檢測頻率增加以及醫院和診斷檢查室患者篩檢計畫擴展的推動,為供應商提供了持續的收入來源。

預計到2025年,檢查室設備市場規模將達到26億美元,並在2035年之前以4.6%的複合年成長率成長。檢查室系統因其高精度和高可靠性而備受青睞,能夠提供診斷貧血和紅血球增多症等疾病所需的精確血球比容值。由於患者病例日益複雜,以及對詳細診斷的需求不斷成長,檢查室檢測仍然被視為標準診斷方法。

美國血球比容檢測設備市場預計到2025年將達到14.5億美元,並在2035年之前以4.3%的複合年成長率成長。美國擁有完善的醫療基礎設施,包括先進的醫院、診斷檢查室以及能夠進行大量、高精度檢測的實驗室。對早期檢測和持續病患監測的重視,以及對尖端血液分析儀的廣泛應用,進一步推動了該地區的市場成長。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 貧血和其他血液疾病的盛行率增加

- 即時診斷檢測的需求日益成長

- 血液分析儀和診斷設備的技術進步

- 擴大醫療基礎設施和診斷檢查室

- 產業潛在風險與挑戰

- 先進的血球比容測量設備高成本

- 因使用不當或環境因素導致結果不準確的風險

- 市場機遇

- 在貧血問題嚴重的新興市場,擴大血球容積比檢測的覆蓋範圍。

- 攜帶式和手持式血球比容測量設備的廣泛應用

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術(基於初步調查)

- 未來市場趨勢(基於初步研究)

- 波特五力分析

- PESTEL 分析

- 客戶洞察(基於初步研究)

- Start-Ups情境(基於初步研究)

- 投資環境(基於初步調查)

- 人工智慧的影響與未來前景

- 價值鏈分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 裝置

- 血球容積比測量裝置

- 血球比容計

- 試劑和耗材

第6章 市場估計與預測:依測試方法分類,2022-2035年

- 檢查室檢測

- 即時偵測 (POC)

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 貧血

- 先天性心臟疾病

- 真性紅血球增多症

- 其他用途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 診斷檢查室

- 門診手術中心

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- A. Menarini

- Abbott

- BIO-RAD

- Boule

- Danaher

- Diatron

- EKF Diagnostics

- HORIBA Medical

- Mindray

- NIHON KOHDEN

- Nova Biomedical

- Roche

- SENSA CORE

- Siemens Healthineers

- Sysmex

The Global Hematocrit Test Devices Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 6.1 billion by 2035.

Market growth is driven by the rising prevalence of blood disorders, an aging global population, and continuous advancements in point-of-care testing technologies. Hematocrit test devices measure the proportion of red blood cells in a patient's blood, expressed as a percentage of total blood volume, and are widely used in hospitals, diagnostic labs, and point-of-care facilities to monitor conditions such as anemia, dehydration, and other hematological disorders. Modern devices integrate compact designs, digital interfaces, and automated sample processing, improving testing speed, accuracy, and operational efficiency. The adoption of portable and handheld hematocrit analyzers is rapidly increasing, enabling healthcare professionals to perform bedside testing in clinics, emergency care, and ambulatory services. Rapid results enhance clinical decision-making, support trauma management, and improve patient outcomes while reducing reliance on centralized laboratories. The market is further supported by innovations in microfluidics, automated hematology platforms, and continuous improvements in diagnostic accuracy.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 4.8% |

The reagents and consumables segment generated USD 1.6 billion in 2025 and is projected to grow at a CAGR of 5.4% through 2035. The demand for reagents, microcapillary tubes, and cartridges is driven by the high frequency of hematocrit testing and expanding patient screening programs across hospitals and diagnostic laboratories, ensuring recurring revenue for suppliers.

The laboratory-based testing devices segment accounted for USD 2.6 billion in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Laboratory systems are favored for their high precision and reliability, offering accurate hematocrit results necessary for diagnosing conditions such as anemia and polycythemia. The increasing complexity of patient cases and demand for detailed diagnostics continue to reinforce laboratory-based testing as the benchmark standard.

U.S. Hematocrit Test Devices Market was valued at USD 1.45 billion in 2025, with a projected CAGR of 4.3% through 2035. The country benefits from a sophisticated healthcare infrastructure comprising advanced hospitals, diagnostic laboratories, and research institutions capable of high-volume, precise testing. The emphasis on early detection, continuous patient monitoring, and the adoption of cutting-edge hematology analyzers further support market growth in the region.

Key players operating in the Global Hematocrit Test Devices Market include Roche, Abbott, Danaher, Siemens Healthineers, Nova Biomedical, EKF Diagnostics, NIHON KOHDEN, Boule, Mindray, Diatron, HORIBA Medical, A. Menarini, BIO-RAD, SENSA CORE, and Sysmex. Companies in the Global Hematocrit Test Devices Market strengthen their presence by investing heavily in research and development to enhance device accuracy, processing speed, and usability. They are expanding their product portfolios to include portable, point-of-care, and automated systems tailored to hospital, laboratory, and emergency settings. Strategic partnerships with healthcare providers, distributors, and diagnostic laboratories help improve market access and reach. Firms focus on expanding geographic coverage, entering emerging markets, and offering training and after-sales support to build customer loyalty. Product differentiation through compact design, digital integration, and workflow optimization ensures sustained adoption, while ongoing technological innovation and marketing initiatives maintain competitive positioning and long-term growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Modality trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of anemia and other blood disorders

- 3.2.1.2 Growing demand for point-of-care (POC) diagnostic testing

- 3.2.1.3 Technological advancements in hematology analyzers and diagnostic devices

- 3.2.1.4 Expansion of healthcare infrastructure and diagnostic laboratories

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced hematocrit testing devices

- 3.2.2.2 Risk of inaccurate results due to improper usage or environmental factors

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of hematocrit testing in emerging markets with high anemia burden

- 3.2.3.2 Growing adoption of portable and handheld hematocrit testing devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Customer insights (Driven by primary research)

- 3.10 Start-up scenarios (Driven by primary research)

- 3.11 Investment landscape (Driven by primary research)

- 3.12 Impact of AI and its future assessment

- 3.13 Value chain analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.2.1 Hematocrit test analyzer

- 5.2.2 Hematocrit test meter

- 5.3 Reagents and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Laboratory-based testing

- 6.3 Point-of-care (POC) testing

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Anemia

- 7.3 Congenital heart diseases

- 7.4 Polycythemia vera

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 A. Menarini

- 10.2 Abbott

- 10.3 BIO-RAD

- 10.4 Boule

- 10.5 Danaher

- 10.6 Diatron

- 10.7 EKF Diagnostics

- 10.8 HORIBA Medical

- 10.9 Mindray

- 10.10 NIHON KOHDEN

- 10.11 Nova Biomedical

- 10.12 Roche

- 10.13 SENSA CORE

- 10.14 Siemens Healthineers

- 10.15 Sysmex