|

市場調查報告書

商品編碼

2019201

2026 年至 2035 年肉類和家禽加工設備市場的商業機會、成長要素、產業趨勢和預測。Meat and Poultry Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

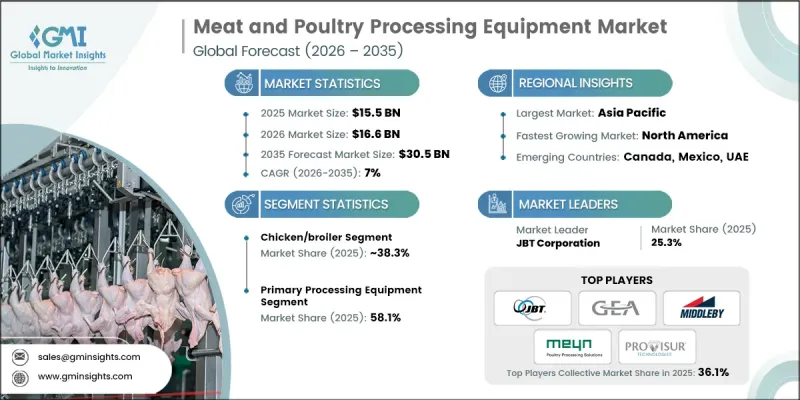

預計到 2025 年,全球肉類和家禽加工設備市場價值將達到 155 億美元,並預計以 7% 的複合年成長率成長,到 2035 年達到 305 億美元。

全球肉品消費量的成長以及對現代化、先進加工設備的需求推動了市場成長,這些設備能夠確保效率、安全性和合規性。肉類加工機械涵蓋從屠宰和初級加工到包裝和保鮮的整個流程,使生產商能夠滿足更高的生產需求。亞太地區憑藉著不斷壯大的中產階級、日益成長的可支配收入以及飲食結構向以肉類為主的轉變,成為全球市場的主要驅動力。北美是成長最快的市場,自動化和技術進步正在緩解勞動力短缺問題,並確保符合嚴格的食品安全標準。投資自動化機器人和智慧加工系統對於提高營運效率、保持衛生以及滿足大規模生產需求至關重要。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 155億美元 |

| 預測金額 | 305億美元 |

| 複合年成長率 | 7% |

截至2025年,雞肉/肉雞產業將佔38.3%的市場佔有率,預計到2035年將以7.1%的複合年成長率成長。雞肉的高消費量、多功能性和成本效益是推動去骨機、分切機和包裝機等專用加工設備發展的主要因素,這些設備能夠提高效率和安全性。至2025年,初級加工設備將佔市場佔有率的58.1%,涵蓋屠宰、內臟移除和胴體分割等關鍵工序。在此階段,自動化對於提高加工能力、衛生管理以及遵守安全法規至關重要。

預計2026年至2035年,北美肉類和家禽加工設備市場將以7.4%的複合年成長率成長。對永續加工實踐(例如廢水回收和管理)的重視正在推動先進設備的應用。消費者對環境影響的日益關注,以及對放養肉類和家禽需求的成長,促使製造商投資於環保且高效的加工技術。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球肉類消費量增加及生產規模擴大

- 勞動力短缺和自動化需求

- 食品安全和品質法規的嚴格性

- 產業潛在風險與挑戰

- 需要大量資金投入。

- 對維護和服務成本的擔憂

- 市場機遇

- 維修和升級市場

- 新興品種和產品類型

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依肉類種類

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依肉品類型分類,2022-2035年

- 牛肉

- 豬肉

- 雞/肉雞

- 土耳其

- 鴨子

- 羊肉

- 山羊

- 其他

第6章 市場估算與預測:依加工階段分類,2022-2035年

- 初級加工設備

- 屠宰和摘取器官

- 冷卻和胴體加工

- 二次加工設備

- 切割、去骨、修整

- 分份和加工

第7章 市場估算與預測:依自動化程度分類,2022-2035年

- 手動設備

- 半自動化設備

- 全自動設備

- 智慧/人工智慧系統

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Alberk Poultry Processing Equipment

- BAADER

- Bayle SA

- Cantrell Gainco

- Frontmatec

- GEA Group

- Jarvis Canada

- JBT Corporation

- Mayekawa

- Meyn

- Middleby Corporation

- Provisur Technologies

- Tomra Food

The Global Meat and Poultry Processing Equipment Market was valued at USD 15.5 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 30.5 billion by 2035.

The market growth is fueled by rising global meat consumption and the demand for modernized advanced processing equipment that ensures efficiency, safety, and regulatory compliance. Meat processing machinery covers all stages, from slaughtering and primary processing to packaging and preservation, allowing producers to meet higher production demands. Asia-Pacific leads the global market due to a growing middle-class population, rising disposable incomes, and shifts toward meat-based diets. North America is the fastest-growing market as automation and technological advancements address labor shortages while ensuring compliance with stringent food safety standards. Investment in automated robots and intelligent processing systems has become essential to improve operational efficiency, maintain hygiene, and meet large-scale production requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.5 Billion |

| Forecast Value | $30.5 Billion |

| CAGR | 7% |

The chicken/broiler segment held a 38.3% share in 2025 and is expected to grow at a CAGR of 7.1% through 2035. The high consumption, versatility, and cost-effectiveness of chicken make it a major driver for specialized processing equipment, including deboning, portioning, and packaging machines that increase efficiency and safety. Primary processing equipment accounted for 58.1% of the market in 2025, as it covers crucial stages like slaughtering, evisceration, and carcass splitting. Automation at this stage is critical for high throughput, hygiene, and compliance with safety regulations.

North America Meat and Poultry Processing Equipment Market is expected to grow at a CAGR of 7.4% between 2026 and 2035. Emphasis on sustainable processing practices, such as wastewater recycling and effluent management, is supporting the adoption of advanced equipment. Consumer awareness of environmental impact, coupled with rising demand for naturally produced meat and poultry, encourages manufacturers to invest in eco-friendly and efficient processing technologies.

Key players in the Global Meat and Poultry Processing Equipment Market include Alberk Poultry Processing Equipment, BAADER, Bayle SA, Cantrell Gainco, Frontmatec, GEA Group, Jarvis Canada, JBT Corporation, Mayekawa, Meyn, Middleby Corporation, Provisur Technologies, and Tomra Food. Companies in the Meat and Poultry Processing Equipment Market strengthen their foothold by investing in R&D to develop automated, high-throughput, and safety-compliant machinery. They expand portfolios to include energy-efficient and sustainable solutions, while forming strategic partnerships with meat producers to enhance market reach. Focused marketing campaigns, after-sales service, and training programs for operators improve product adoption. Regional expansion into high-growth markets, customization to local processing needs, and integration of smart monitoring systems enhance operational efficiency and customer satisfaction, solidifying market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Meat type

- 2.2.3 Processing stage

- 2.2.4 Automation level

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global meat consumption & production expansion

- 3.2.1.2 Labor shortage & automation imperative

- 3.2.1.3 Food safety & quality regulations stringency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements

- 3.2.2.2 Maintenance & service cost concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit & upgrade market

- 3.2.3.2 Emerging species & product categories

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By meat type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Meat Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Beef

- 5.3 Pork

- 5.4 Chicken/broiler

- 5.5 Turkey

- 5.6 Duck

- 5.7 Lamb

- 5.8 Goat

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Processing Stage, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Primary processing equipment

- 6.2.1 Slaughter & evisceration

- 6.2.2 Chilling & carcass handling

- 6.3 Secondary processing equipment

- 6.3.1 Cutting, deboning & trimming

- 6.3.2 Portioning & fabrication

Chapter 7 Market Estimates and Forecast, By Automation Level, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Manual equipment

- 7.3 Semi-automated equipment

- 7.4 Fully automated equipment

- 7.5 Intelligent/AI-enabled systems

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Alberk Poultry Processing Equipment

- 9.2 BAADER

- 9.3 Bayle SA

- 9.4 Cantrell Gainco

- 9.5 Frontmatec

- 9.6 GEA Group

- 9.7 Jarvis Canada

- 9.8 JBT Corporation

- 9.9 Mayekawa

- 9.10 Meyn

- 9.11 Middleby Corporation

- 9.12 Provisur Technologies

- 9.13 Tomra Food

肉類和家禽加工設備市場:2026-2032年全球市場預測(按設備類型、半自動設備、肉類類型、應用、最終用戶和銷售管道)

肉類和家禽加工設備市場:2026-2032年全球市場預測(按設備類型、半自動設備、肉類類型、應用、最終用戶和銷售管道) 全球家禽加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家禽加工消毒系統市場(按系統類型、技術、運作規模、安裝方式和應用分類),全球預測(2026-2032)

全球家禽加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家禽加工消毒系統市場(按系統類型、技術、運作規模、安裝方式和應用分類),全球預測(2026-2032) 2026年全球家禽加工設備市場報告2026年全球肉類和家禽加工設備市場報告

2026年全球家禽加工設備市場報告2026年全球肉類和家禽加工設備市場報告 家禽加工設備市場-全球產業規模、佔有率、趨勢、機會及預測(依設備類型、家禽類型、產品類型、地區及競爭格局分類,2021-2031年)

家禽加工設備市場-全球產業規模、佔有率、趨勢、機會及預測(依設備類型、家禽類型、產品類型、地區及競爭格局分類,2021-2031年) 家禽加工設備:全球市佔率及排名、總收入及需求預測(2025-2031年)

家禽加工設備:全球市佔率及排名、總收入及需求預測(2025-2031年) 肉類和家禽加工設備市場規模、佔有率和成長分析(按類型、肉類類型、產品類型和地區)- 產業預測 2025-2032

肉類和家禽加工設備市場規模、佔有率和成長分析(按類型、肉類類型、產品類型和地區)- 產業預測 2025-2032 2024-2028年全球肉類及家禽加工設備市場全球家禽加工設備市場:到 2033 年的機會與策略

2024-2028年全球肉類及家禽加工設備市場全球家禽加工設備市場:到 2033 年的機會與策略