|

市場調查報告書

商品編碼

2019197

2026 年至 2035 年可可豆衍生產品的市場機會、成長要素、產業趨勢與預測。Cocoa Bean Derivatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

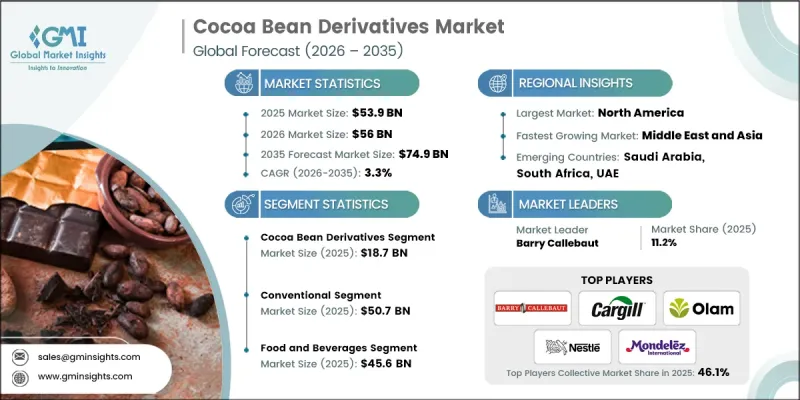

全球可可豆衍生性商品市場預計到 2025 年價值 539 億美元,預計到 2035 年將達到 749 億美元,年複合成長率為 3.3%。

這一成長主要得益於食品飲料、個人護理和工業應用領域對可可製品的需求不斷成長。可可衍生品,包括可可液塊、可可脂、可可粉、可可餅和可可殼,是透過乾燥、烘焙和研磨等後發酵過程生產的。可可液塊是一種由可可固態和可可脂組成的半液體糊狀物,經壓榨將可可脂與可可餅分離,並進一步加工成可可粉。現代加工技術,例如先進的烘焙工藝、液壓和機械壓榨以及精密研磨系統,提高了萃取效率、風味一致性和質地均勻性。這些創新使製造商能夠在保持製程控制和最佳化生產效率的同時,生產出滿足各種工業需求的高品質衍生品。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 539億美元 |

| 預測金額 | 749億美元 |

| 複合年成長率 | 3.3% |

預計到2025年,傳統可可衍生性商品市場規模將達507億美元。這反映了這些產品在全球食品飲料和個人護理行業中的廣泛應用。由於其品質穩定、供應充足且經濟實惠,這些產品仍然是巧克力、烘焙產品、糖果甜點和其他可可食品生產的基礎。傳統可可衍生品的優勢源於成熟的加工工藝,例如烘焙、研磨和壓榨,這些工藝確保了大規模生產中風味、質地和脂肪含量的穩定性。此外,製造商更傾向於使用傳統可可原料,因為它們易於大量採購並融入標準化的配方中。

預計到2025年,食品飲料市場規模將達到456億美元。可可衍生物為巧克力、烘焙食品、乳製品和飲料產品提供必要的風味、質地、色澤和穩定性。在食品領域之外,可可脂廣泛用於個人保健產品,具有保濕和軟化皮膚的功效;可可衍生物也應用於營養保健品、藥品和工業生產中,展現了其在眾多領域的廣泛應用。

預計北美可可豆衍生性商品市場將強勁成長,從2025年的159億美元增至2035年的217億美元。該地區受益於先進的加工基礎設施、強大的零售和電商管道,以及對功能性和高階可可產品日益成長的需求。在美國,專門食品巧克力、潔淨標示產品和有機產品中可可脂和可可粉的日益普及是推動市場成長的主要因素。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 消費者對富含膠原蛋白的機能性食品的興趣日益濃厚。

- 原始人飲食法和生酮飲食法的傳播

- 對不含乳製品的蛋白質替代品的需求

- 產業潛在風險與挑戰

- 高昂的生產和採購成本

- 它對素食者和純素食消費者的吸引力有限。

- 市場機遇

- 開發即飲型及便利商店型產品。

- 風味增強和掩味技術的創新

- 新興健康和保健市場的成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 可可豆

- 可可脂

- 可可粉

- 其他可可衍生產品

第6章 市場估計與預測:依類別分類,2022-2035年

- 有機的

- 傳統的

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 飲食

- 個人護理

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 銷售代理商/批發商

- 零售通路

- 線上管道

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Barry Callebaut

- Cargill

- CEMOI

- Cocoa Touton

- ECOM Agroindustrial

- Ecuakao Group

- Ferrero

- Indcre

- JB Foods

- Mondelez International

- Moner Cocoa

- Natra

- Nestle

- Olam Group

- United Cocoa Processor

The Global Cocoa Bean Derivatives Market was valued at USD 53.9 billion in 2025 and is estimated to grow at a CAGR of 3.3% to reach USD 74.9 billion by 2035.

Growth is driven by the rising demand for cocoa-based products across food, beverage, personal care, and industrial applications. Cocoa derivatives, including cocoa liquor, cocoa butter, cocoa powder, cocoa cake, and cocoa shell by-products, are produced through post-fermentation processes such as drying, roasting, and grinding. Cocoa liquor, a semi-liquid paste of cocoa solids and cocoa butter, is pressed to separate cocoa butter from cocoa cake, which is further processed into cocoa powder. Modern processing technologies, including advanced roasting, hydraulic and mechanical pressing, and precise grinding systems, enhance extraction efficiency, flavor consistency, and texture uniformity. These innovations allow manufacturers to produce high-quality derivatives tailored to diverse industrial needs while maintaining process control and optimizing production efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.9 Billion |

| Forecast Value | $74.9 Billion |

| CAGR | 3.3% |

The conventional cocoa derivatives segment reached USD 50.7 billion in 2025, reflecting their widespread adoption across the global food, beverage, and personal care industries. These products remain the backbone of chocolate manufacturing, bakery items, confectionery, and other cocoa-based foods due to their consistent quality, availability, and cost-effectiveness. The dominance of conventional cocoa derivatives is supported by established processing techniques, including roasting, grinding, and pressing, which ensure reliable flavor, texture, and fat content for large-scale production. Additionally, manufacturers prefer conventional cocoa ingredients because they are easier to source in bulk and integrate into standardized formulations.

The food & beverage segment captured USD 45.6 billion in 2025. Cocoa derivatives contribute to chocolate, bakery, dairy, and beverage products by providing essential taste, texture, color, and stability. Beyond food, cocoa butter is widely used in personal care products for hydration and skin softening, while cocoa derivatives also find applications in nutraceuticals, pharmaceuticals, and industrial processes, demonstrating their versatility across multiple sectors.

North America Cocoa Bean Derivatives Market is projected to witness strong growth from USD 15.9 billion in 2025 to USD 21.7 billion in 2035. The region benefits from advanced processing infrastructure, robust retail and e-commerce channels, and increasing demand for functional and premium cocoa products. The United States drives the market through rising use of cocoa butter and powder in specialty chocolates, clean-label, and organic offerings.

Prominent players in the Global Cocoa Bean Derivatives Market include Barry Callebaut, Ferrero, Mondelez International, Nestle, Cargill, Cocoa Touton, ECOM Agroindustrial, Natra, JB Foods, Moner Cocoa, Indcre, Olam Group, CEMOI, Ecuakao Group, and United Cocoa Processor. Companies in the Cocoa Bean Derivatives Market are focusing on strategies such as expanding production capacity, investing in advanced processing technologies, and enhancing supply chain efficiency to strengthen their market presence. Firms are prioritizing sustainability and traceability initiatives to meet consumer demand for ethically sourced products. Product portfolio diversification, particularly with organic and specialty cocoa derivatives, helps cater to premium and functional product segments. Strategic partnerships with food, beverage, and personal care manufacturers allow market players to secure long-term contracts and improve market penetration. Companies also emphasize research and development to improve extraction efficiency, flavor consistency, and product quality while maintaining compliance with global food safety standards, creating a competitive advantage in the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Type

- 2.2.3 Category

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in collagen-rich functional nutrition

- 3.2.1.2 Increasing adoption of paleo and keto lifestyles

- 3.2.1.3 Demand for dairy-free protein alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and sourcing costs

- 3.2.2.2 Limited appeal among vegetarian and vegan consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into ready-to-drink and convenience formats

- 3.2.3.2 Innovation in flavor enhancement and masking technologies

- 3.2.3.3 Growth in emerging health and wellness markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cocoa beans

- 5.3 Cocoa butter

- 5.4 Cocoa powder

- 5.5 Other cocoa derivatives

Chapter 6 Market Estimates and Forecast, By Category, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.3 Personal care

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Distributors / Wholesalers

- 8.3 Retail Channels

- 8.4 Online Channels

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Barry Callebaut

- 10.2 Cargill

- 10.3 CEMOI

- 10.4 Cocoa Touton

- 10.5 ECOM Agroindustrial

- 10.6 Ecuakao Group

- 10.7 Ferrero

- 10.8 Indcre

- 10.9 JB Foods

- 10.10 Mondelez International

- 10.11 Moner Cocoa

- 10.12 Natra

- 10.13 Nestle

- 10.14 Olam Group

- 10.15 United Cocoa Processor

可可豆市場機會、成長要素、產業趨勢分析及2026-2035年預測。

可可豆市場機會、成長要素、產業趨勢分析及2026-2035年預測。 全球可可豆衍生物市場

全球可可豆衍生物市場 可可豆市場規模、佔有率和成長分析(按產品、豆類、品質、應用、分銷管道和地區)- 2025-2032 年產業預測

可可豆市場規模、佔有率和成長分析(按產品、豆類、品質、應用、分銷管道和地區)- 2025-2032 年產業預測