|

市場調查報告書

商品編碼

2019194

肉品研磨機市場機會、成長要素、產業趨勢分析及2026-2035年預測。Meat Grinder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

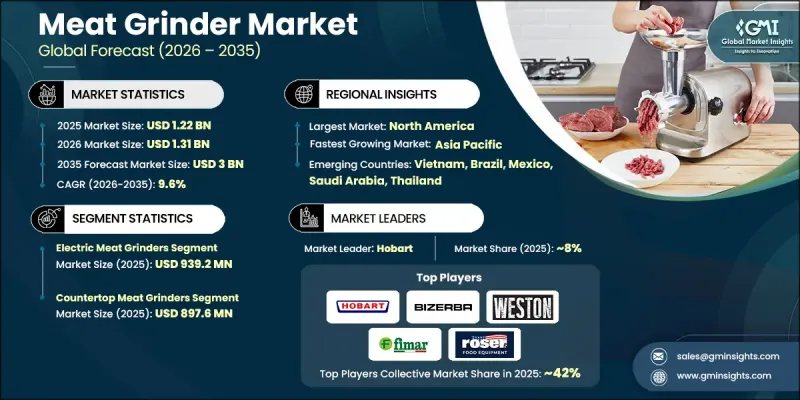

全球研磨機市場預計到 2025 年將達到 12.2 億美元,年複合成長率為 9.6%,到 2035 年將達到 30 億美元。

近年來,受消費者對價格適中、品質優良的加工肉品需求不斷成長的推動,研磨機行業經歷了強勁而穩定的成長。隨著消費者越來越重視食材品質和個人化客製化,家庭烹飪的興起進一步加速了市場擴張。研磨機日益被公認為一種有效保持產品品質穩定並滿足不斷變化的消費者偏好。同時,食品加工技術的進步提高了效率和產品質量,從而支持了住宅和商用應用。儘管存在這些積極趨勢,但成本仍然是一個重大挑戰,尤其是對於工業用戶而言,因為大型設備和先進加工系統需要大量的資本投入。因此,市場正努力在強勁的需求成長與持續提升產品可及性和成本效益之間取得平衡,以確保在各個終端使用者群體中持續擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 12.2億美元 |

| 預測金額 | 30億美元 |

| 複合年成長率 | 9.6% |

隨著自動化系統、高容量絞肉設備和變速運行等先進加工技術的引入,研磨機市場正在不斷發展。這些創新正在提高整個產業的生產效率和營運效率。然而,工業設備所需的高額初始投資仍然限制了中小企業和個人用戶的採用。

預計到2025年,電動研磨機市場規模將達到9.392億美元,並在2026年至2035年間以10%的複合年成長率成長。與手動絞肉機相比,電動絞肉機因其處理速度更快、品質更穩定、使用更便捷而廣受歡迎。馬達效率、系統耐用性和安全性能的不斷提升,正推動著電動絞肉機的進一步普及。此外,成本績效實惠的電動絞肉機型號的日益普及也擴大了其市場覆蓋範圍,使更多消費者能夠使用這類產品。

預計2025年,桌上型研磨機市佔率將達到73%,市場規模將達到8.976億美元,到2035年將以10%的複合年成長率成長。其便攜性、緊湊的設計和易於存放的特點使其成為現代廚房的理想之選。這些產品使用和擺放柔軟性,而改進的設計功能則提升了安全性和便利性,使其對住宅用戶極具吸引力。

美國研磨機市場預計到2025年將達到2.784億美元,並在2026年至2035年間以9.9%的複合年成長率成長。這一成長主要得益於消費者對家庭烹飪和個人化烹飪日益成長的興趣。儘管消費者對高效耐用的廚房電器需求不斷成長,但空間和成本仍然是影響購買決策的重要因素。因此,小巧、中價位的產品正受到廣大用戶的青睞。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 擴大大容量工業系統的應用

- 「潔淨標示」和對新鮮加工肉品的需求

- 技術向電動和“智慧型”研磨機轉變

- 產業潛在風險與挑戰

- 嚴格的衛生和食品安全法規(美國農業部/歐洲食品安全局)

- 商用級設備需要大量的初始投資。

- 產業機遇

- 人工智慧驅動的品質和污染檢測整合

- 拓展電子商務與D2C銷售管道

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 過去價格趨勢分析(基於初步調查)(2022-2024 年)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 產品類型和生產能力所導致的價格波動

- 區域價格基準

- 原物料成本對價格的影響

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於第一次調查)(2019-2024 年)

- 主要貿易路線及關稅的影響(基於初步調查)

- 主要出口國(德國、中國、義大利、美國)

- 主要進口國家和地區的需求趨勢

- 貿易政策對市場動態的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的已安裝產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 手動研磨機

- 電動研磨機

第6章 市場估計與預測:依飼餵方式分類,2022-2035年

- 托盤式進料研磨機

- 垂直進料

- 螺旋送料

- 推式

- 其他(例如,真空供應)

第7章 市場估計與預測:依材料類型分類,2022-2035年

- 鋁

- 鑄鐵

- 不銹鋼

- 其他(碳鋼等)

第8章 市場估算與預測:依結構分類,2022-2035年

- 桌上型研磨機

- 固定式研磨機

- 落地式

- 桌面型

第9章 市場估計與預測:依產能分類,2022-2035年

- 小型(每小時低於 150 磅)

- 中等體型(150-500磅/小時)

- 大型(超過500磅/小時)

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 小型汽車

- 中號

- 大型汽車

第11章 市場估價與預測:依價格區間分類,2022-2035年

- 低價位(500美元以下)

- 中價位(500-1000美元)

- 高價位(超過1000美元)

第12章 市場估計與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業的

- 飯店和餐廳

- 餐飲服務

- 肉店

- 其他

- 工業的

- 肉類加工廠

- 食品製造設施

第13章 市場估計與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 企業網站

- 離線

- 大賣場和超級市場

- 專賣店

- 其他(百貨公司、個體店等)

第14章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第15章:公司簡介

- Hobart

- Bizerba

- Weston Brands

- Fimar Spa

- Roser Group

- ADE Germany

- Dito Sama

- Fatosa, SA

- Dadaux SAS

- Ari Makina

- Amisy

- Nikai Group

- ASGO

- CRM srl

- Clearline

- ABM Company

- AlexanderSolia GmbH

The Global Meat Grinder Market was valued at USD 1.22 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 3 billion by 2035.

The meat grinder industry has experienced strong and consistent expansion in recent years, driven by increasing demand for affordable and high-quality processed meat products. Rising interest in home-based food preparation is further accelerating adoption, as consumers seek greater control over ingredient quality and customization. Meat grinding solutions are increasingly being recognized as an effective way to maintain product consistency while meeting evolving consumer preferences. At the same time, advancements in food processing technology are improving efficiency and output quality, supporting both residential and commercial applications. Despite these positive trends, cost remains a key challenge, particularly for industrial users, as heavy-duty equipment and advanced processing systems require significant capital investment. The market is therefore balancing strong demand growth with ongoing efforts to improve accessibility and cost efficiency, ensuring continued expansion across diverse end-user segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.22 Billion |

| Forecast Value | $3 Billion |

| CAGR | 9.6% |

The meat grinder market is evolving with the adoption of advanced processing technologies, including automated systems, high-capacity grinding equipment, and variable-speed operations. These innovations are enhancing productivity and operational efficiency across the industry. However, the high upfront investment required for industrial-grade equipment continues to limit adoption among smaller businesses and individual users.

The electric meat grinders segment generated USD 939.2 million in 2025 and is expected to grow at a CAGR of 10% from 2026 to 2035. These products are widely preferred due to their high processing speed, consistent output quality, and ease of use compared to manual alternatives. Continuous improvements in motor efficiency, system durability, and safety features are further driving their adoption. Increased availability of cost-effective electric models is also expanding accessibility, allowing a broader range of consumers to adopt these solutions.

The countertop meat grinders segment held a 73% share and was valued at USD 897.6 million in 2025, with a projected CAGR of 10% through 2035. Their portability, compact design, and ease of storage make them well-suited for modern kitchen environments. These units offer flexibility in usage and placement, while improved design features enhance safety and convenience, making them highly appealing to residential users.

U.S. Meat Grinder Market captured USD 278.4 million in 2025 and is expected to grow at a CAGR of 9.9% from 2026 to 2035. Growth is supported by increasing consumer interest in home cooking and customized food preparation. Demand for efficient and durable kitchen appliances is rising, although space and cost considerations continue to influence purchasing decisions. As a result, compact and mid-range products are gaining traction among a wide range of users.

Key companies operating in the Global Meat Grinder Market include Bizerba, Hobart, Weston Brands, Fimar S.p.a., Roser Group, Dadaux SAS, ADE Germany, Dito Sama, Fatosa, S.A., Ari Makina, Amisy, Nikai Group, ASGO, C.R.M. s.r.l., Clearline, ABM Company, and AlexanderSolia GmbH. Companies in the Meat Grinder Market are strengthening their competitive position through product innovation and strategic expansion. They are investing in advanced technologies to improve efficiency, durability, and user safety. Manufacturers are focusing on developing compact and energy-efficient models that cater to both residential and commercial users. Strategic partnerships and distribution network expansion are helping companies reach new markets and enhance brand visibility. Firms are also emphasizing cost optimization and product differentiation to appeal to a broader customer base. Additionally, continuous improvements in design, functionality, and performance are enabling companies to meet evolving consumer demands while maintaining a strong market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Feed Type

- 2.2.4 Material Type

- 2.2.5 Structure

- 2.2.6 Capacity

- 2.2.7 Operation

- 2.2.8 Price Range

- 2.2.9 End-Use

- 2.2.10 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of high-capacity industrial systems

- 3.2.1.2 Demand for "Clean-Label" and Freshly Processed Meat

- 3.2.1.3 Technological pivot to electric and "Smart" grinders

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Strict hygiene and food safety regulations (USDA/EFSA)

- 3.2.2.2 High initial investment for commercial-grade units

- 3.2.3 Industry Opportunities

- 3.2.3.1 Integration of AI-powered quality & contamination detection

- 3.2.3.2 Expansion of E-commerce and D2C sales channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research) (2022-2024)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.6.3 Price Variation by Product Type & Capacity

- 3.6.4 Regional Price Benchmarking

- 3.6.5 Impact of Raw Material Costs on Pricing

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research) (2019-2024)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 Major Exporting Countries (Germany, China, Italy, U.S.)

- 3.10.4 Major Importing Countries & Regional Demand Patterns

- 3.10.5 Trade Policy Impact on Market Dynamics

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Million Units)

- 5.1 Key trends

- 5.2 Manual Meat Grinder

- 5.3 Electric Meat Grinder

Chapter 6 Market Estimates and Forecast, By Feed Type, 2022 - 2035 (USD Million) (Million Units)

- 6.1 Key trends

- 6.2 Tray Feed Grinder

- 6.3 Vertical Feed

- 6.4 Auger Feed

- 6.5 Manual Push Feed

- 6.6 Others (Vacuum Feed, etc.)

Chapter 7 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million) (Million Units)

- 7.1 Key trends

- 7.2 Aluminum

- 7.3 Cast Iron

- 7.4 Stainless Steel

- 7.5 Others (Carbon Steel, etc.)

Chapter 8 Market Estimates and Forecast, By Structure, 2022 - 2035 (USD Million) (Million Units)

- 8.1 Key trends

- 8.2 Countertop Meat Grinder

- 8.3 Mounted Meat Grinder

- 8.3.1 Floor Mounted

- 8.3.2 Table Mounted

Chapter 9 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million) (Million Units)

- 9.1 Key trends

- 9.2 Small (Up to 150 lbs/hour)

- 9.3 Medium (150-500 lbs/hour)

- 9.4 Large (Above 500 lbs/hour)

Chapter 10 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Million) (Million Units)

- 10.1 Key trends

- 10.2 Light-duty

- 10.3 Medium-duty

- 10.4 Heavy-duty

Chapter 11 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Million) (Million Units)

- 11.1 Key trends

- 11.2 Low (Under USD 500)

- 11.3 Medium (USD 500 - USD 1000)

- 11.4 High (Above USD 1000)

Chapter 12 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million) (Million Units)

- 12.1 Key trends

- 12.2 Residential

- 12.3 Commercial

- 12.3.1 Hotels and Restaurants

- 12.3.2 Catering Services

- 12.3.3 Butcher Shops

- 12.3.4 Others

- 12.4 Industrial

- 12.4.1 Meat Processing Plants

- 12.4.2 Food Manufacturing Facilities

Chapter 13 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Million Units)

- 13.1 Key trends

- 13.2 Online

- 13.2.1 E-commerce Website

- 13.2.2 Company Website

- 13.3 Offline

- 13.3.1 Hypermarkets and Supermarkets

- 13.3.2 Specialty Stores

- 13.3.3 Others (Department Stores, Individual Stores, etc.)

Chapter 14 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Million Units)

- 14.1 Key trends

- 14.2 North America

- 14.2.1 U.S.

- 14.2.2 Canada

- 14.3 Europe

- 14.3.1 Germany

- 14.3.2 UK

- 14.3.3 France

- 14.3.4 Italy

- 14.3.5 Spain

- 14.4 Asia Pacific

- 14.4.1 China

- 14.4.2 India

- 14.4.3 Japan

- 14.4.4 South Korea

- 14.4.5 Australia

- 14.4.6 Indonesia

- 14.4.7 Malaysia

- 14.5 Latin America

- 14.5.1 Brazil

- 14.5.2 Mexico

- 14.5.3 Argentina

- 14.6 MEA

- 14.6.1 Saudi Arabia

- 14.6.2 UAE

- 14.6.3 South Africa

Chapter 15 Company Profiles

- 15.1 Hobart

- 15.2 Bizerba

- 15.3 Weston Brands

- 15.4 Fimar S.p.a.

- 15.5 Roser Group

- 15.6 ADE Germany

- 15.7 Dito Sama

- 15.8 Fatosa, S.A.

- 15.9 Dadaux SAS

- 15.10 Ari Makina

- 15.11 Amisy

- 15.12 Nikai Group

- 15.13 ASGO

- 15.14 C.R.M. s.r.l.

- 15.15 Clearline

- 15.16 ABM Company

- 15.17 AlexanderSolia GmbH