|

市場調查報告書

商品編碼

2019183

水下造粒市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Underwater Pelletizing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

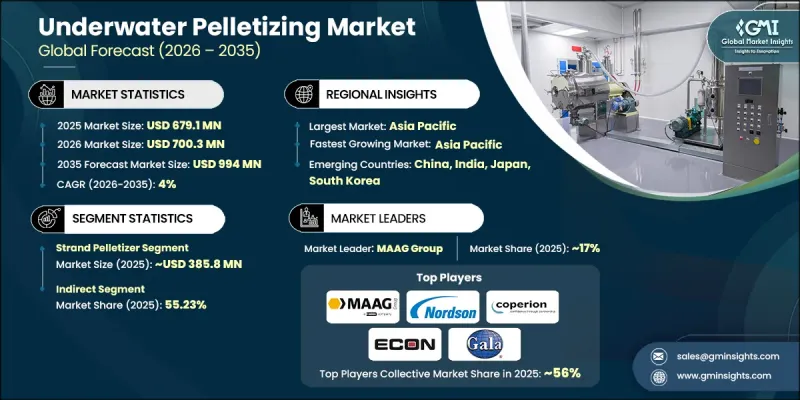

全球水下造粒市場預計到 2025 年將價值 6.791 億美元,預計到 2035 年將以 4% 的複合年成長率成長至 9.94 億美元。

塑膠產業對高效混煉和擠出製程日益成長的需求推動了市場擴張。製造商越來越關注能夠提供穩定均勻顆粒品質的系統,以滿足下游熔融聚合物處理製程的生產要求。水下造粒系統因其能夠在保持產品一致性的同時實現大量生產,正逐漸成為聚合物製造過程中的首選。工程塑膠和特殊塑膠需求的不斷成長進一步加速了對可靠造粒解決方案的需求。加工商正在投資先進設備,以提高冷卻效率、減少材料浪費並實現對顆粒尺寸的精確控制。此外,聚合物在各行業的廣泛應用也增強了對高品質顆粒的需求。造粒機設計的不斷改進提高了運作效率和可靠性,而再生材料的日益普及則推動了對先進造粒技術的進一步投資。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 6.791億美元 |

| 預測金額 | 9.94億美元 |

| 複合年成長率 | 4% |

預計到2025年,條狀晶片市場規模將達到3.858億美元,並在2026年至2035年間以4.2%的複合年成長率成長。該細分市場因其成本效益高且能夠加工多種熱塑性材料而廣泛應用。其製造過程透過將熔融聚合物成型為連續條狀,並在冷卻後切割成均勻的顆粒,從而確保穩定的產量。條狀造粒系統通常用於對產能和操作柔軟性要求適中的應用場合。其結構簡單、易於維護的特點使其成為眾多加工廠的可靠選擇。

到2025年,半自動化系統將佔據最大的市場佔有率。這些系統能夠自動完成顆粒切割和冷卻功能,同時結合人工監控,使操作人員能夠管理關鍵的運作參數。這種自動化與柔軟性的平衡,使得半自動化系統成為那些希望在不進行大量資本投資的情況下實現高效生產的工廠的理想選擇。它們廣泛應用於那些對顆粒品質的穩定性和對不同物料的適應性要求極高的作業中,使操作人員能夠微調製程並保持穩定的生產。

預計到2025年,中國水下造粒市場規模將達到7,050萬美元,並在2035年之前以5.6%的複合年成長率成長。該地區市場成長的主要驅動力是聚合物製造業的快速擴張以及對高品質塑膠顆粒日益成長的需求。產業企業正投資先進的造粒技術,以提高效率、減少廢棄物並確保產品特性的一致性。系統組件的技術進步正在提升設備在大規模生產環境中的耐用性和性能。聚合物產業產能的持續擴張進一步推動了對先進造粒設備的持續需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 糖尿病和足部併發症的盛行率增加

- 需要整形外科支撐的老年人口不斷增加。

- 擴大足科診所和整形外科護理服務

- 陷阱與挑戰

- 高階整形外科和訂製鞋高成本

- 人們對足部疾病的早期療育意識較低。

- 機會

- 3D列印和訂製足部矯正器具的需求日益成長

- 整合智慧感測器進行步態分析和壓力監測

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 專利趨勢(基於初步調查)

- 主要專利擁有者和技術叢集

- 近期專利申請(2022-2025)

- 專利到期分析及學名藥機遇

- 專利的區域分佈

- 價格分析(基於初步調查)

- 貿易數據分析(基於付費資料庫)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 最高可達每小時 100 公斤

- 100 kg/h~500 kg/h

- 500 kg/h~5000 kg/h

- 5,000公斤/小時或以上

第6章 市場估計與預測:依產能分類,2022-2035年

- 鞋

- 涼鞋

- 其他

第7章 市場估算與預測:依自動化程度分類,2022-2035年

- 手動的

- 半自動

- 全自動

第8章 市場估算與預測:依材料類型分類,2022-2035年

- 一般塑膠

- 塑膠工程

- 高性能聚合物

- 生質塑膠

- 彈性體和熱可塑性橡膠(TPE)

- 添加劑母粒和填料

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 塑膠和聚合物製造

- 紡織品及紡織品生產

- 食品包裝

- 回收和廢棄物管理

- 混煉和母粒生產

- 其他

第10章 市場估價與預測:依最終用途產業分類,2022-2035年

- 車

- 纖維

- 製藥

- 建造

- 電子學

- 其他

第11章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第13章:公司簡介

- Coperion GmbH

- Cowell Extrusion

- Cowin Extrusion

- Davis-Standard

- ECON GmbH

- Farrel Pomini

- Gala Industries

- IPS Intelligent Pelletizing Solutions

- Jieya Machinery

- MAAG Group

- Nordson Corporation

- Trendelkamp Technologie GmbH

- USEON Nanjing Extrusion Machinery

- Wuxi Huachen

- Xinda Corporation

The Global Underwater Pelletizing Market was valued at USD 679.1 million in 2025 and is estimated to grow at a CAGR of 4% to reach USD 994 million by 2035.

Market expansion is driven by the rising demand for efficient compounding and extrusion processes within the plastics industry. Manufacturers are increasingly prioritizing systems that deliver consistent and uniform pellet quality to support downstream production requirements involving molten polymers. Underwater pelletizing systems enable high-volume processing while maintaining product consistency, making them a preferred choice across polymer manufacturing operations. The growing demand for engineered and specialty plastics is further accelerating the need for reliable pelletizing solutions. Processors are investing in advanced equipment to enhance cooling efficiency, reduce material waste, and achieve precise pellet size control. In addition, the expansion of polymer applications across multiple industries is strengthening demand for high-quality pellets. Continuous improvements in pelletizer design are enhancing operational efficiency and reliability, while increased availability of recycled materials is encouraging further investment in advanced pelletizing technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $679.1 Million |

| Forecast Value | $994 Million |

| CAGR | 4% |

The strand pelletizer segment generated USD 385.8 million in 2025 and is expected to grow at a CAGR of 4.2% from 2026 to 2035. This segment is widely utilized due to its cost-effectiveness and adaptability in processing a broad range of thermoplastic materials. The production process involves forming continuous strands of molten polymer that are cooled and then cut into uniform pellets, ensuring consistent output. Strand pelletizing systems are commonly adopted for applications requiring moderate production capacity and operational flexibility. Their straightforward design and ease of maintenance make them a reliable choice for many processing facilities.

The semi-automatic segment held the largest share in 2025. These systems combine automated pellet cutting and cooling functions with manual oversight, allowing operators to maintain control over key operational parameters. This balance between automation and flexibility makes semi-automatic systems particularly attractive for facilities seeking efficient production without significant capital investment. They are widely used in operations where consistent pellet quality and adaptability across different materials are essential, enabling operators to fine-tune processes and maintain stable output.

China Underwater Pelletizing Market accounted for USD 70.5 million in 2025 and is projected to grow at a CAGR of 5.6% through 2035. Market growth in the region is supported by the rapid expansion of polymer manufacturing and increasing demand for high-quality plastic pellets. Industrial players are investing in advanced pelletizing technologies to improve efficiency, minimize waste, and ensure consistent product characteristics. Technological advancements in system components are enhancing durability and performance in large-scale production environments. Ongoing capacity expansions within the polymer sector are further contributing to sustained demand for advanced pelletizing equipment.

Key companies operating in the Global Underwater Pelletizing Market include Coperion GmbH, Cowell Extrusion, Cowin Extrusion, Davis-Standard, ECON GmbH, Farrel Pomini, Gala Industries, IPS Intelligent Pelletizing Solutions, Jieya Machinery, MAAG Group, Nordson Corporation, Trendelkamp Technologie GmbH, USEON Nanjing Extrusion Machinery, Wuxi Huachen, and Xinda Corporation. Companies in the Global Underwater Pelletizing Market are strengthening their position through technological innovation, strategic partnerships, and expansion into emerging markets. A key focus is being placed on developing advanced systems that enhance efficiency, reduce energy consumption, and improve pellet quality. Manufacturers are investing in research and development to introduce durable and high-performance equipment capable of handling diverse polymer materials. Collaborations with polymer producers and recycling companies are helping expand application areas and customer reach. Firms are also optimizing production processes and supply chains to remain competitive. Additionally, expanding product portfolios and targeting growing demand in recycling and specialty plastics segments are key strategies supporting long-term market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Production Capacity

- 2.2.4 Level of Automation

- 2.2.5 Material Type

- 2.2.6 Application

- 2.2.7 End Use Industry

- 2.2.8 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes and foot-related complications

- 3.2.1.2 Growing geriatric population requiring orthopedic support

- 3.2.1.3 Expansion of podiatry clinics and orthopedic care services

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High cost of premium orthopedic and custom-made footwear

- 3.2.2.2 Low awareness of early intervention for foot disorders

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for 3D-printed and customized foot orthotics

- 3.2.3.2 Integration of smart sensors for gait analysis and pressure monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent Landscape (Driven by Primary Research)

- 3.10.1 Key Patent Holders & Technology Clusters

- 3.10.2 Recent Patent Filings (2022-2025)

- 3.10.3 Patent Expiry Analysis & Generic Opportunities

- 3.10.4 Geographic Patent Distribution

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.12 Trade Data Analysis (Driven by Paid Data Base)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Up to 100 kg/hr

- 5.3 100 kg/hr to 500 kg/hr

- 5.4 500 kg/hr to 5000 kg/hr

- 5.5 More than 5000 kg/hr

Chapter 6 Market Estimates & Forecast, By Production Capacity, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Shoes

- 6.3 Sandals

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Level of Automation, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By Material Type, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Commodity plastics

- 8.3 Plastics Engineering

- 8.4 High-performance polymers

- 8.5 Bioplastics

- 8.6 Elastomers and thermoplastic elastomers (TPEs)

- 8.7 Additive masterbatch and fillers

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Plastics and polymers manufacturing

- 9.3 Textile and fiber production

- 9.4 Food packaging

- 9.5 Recycling and waste management

- 9.6 Compounding and masterbatch production

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Textile

- 10.4 Pharmaceutical

- 10.5 Construction

- 10.6 Electronics

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Coperion GmbH

- 13.2 Cowell Extrusion

- 13.3 Cowin Extrusion

- 13.4 Davis-Standard

- 13.5 ECON GmbH

- 13.6 Farrel Pomini

- 13.7 Gala Industries

- 13.8 IPS Intelligent Pelletizing Solutions

- 13.9 Jieya Machinery

- 13.10 MAAG Group

- 13.11 Nordson Corporation

- 13.12 Trendelkamp Technologie GmbH

- 13.13 USEON Nanjing Extrusion Machinery

- 13.14 Wuxi Huachen

- 13.15 Xinda Corporation

2026-2030年全球塑膠加工機械市場

2026-2030年全球塑膠加工機械市場 塑膠加工機械市場規模、佔有率、趨勢和預測:按產品類型、塑膠類型、最終用途產業和地區分類,2026-2034年

塑膠加工機械市場規模、佔有率、趨勢和預測:按產品類型、塑膠類型、最終用途產業和地區分類,2026-2034年 水下造粒系統市場:依系統類型、材料、技術、應用和最終用途產業分類-全球預測,2026-2032年吹膜機市場:按塑膠類型、技術、層類型、產量和應用分類-全球預測,2026-2032年氣泡膜校準器市場按技術、校準類型、頻率、形式、精度、應用和最終用途分類,全球預測(2026-2032年)薄膜整理機市場:依部署模式、產品類型、技術、定價模式、最終用戶和通路分類,全球預測,2026-2032年

水下造粒系統市場:依系統類型、材料、技術、應用和最終用途產業分類-全球預測,2026-2032年吹膜機市場:按塑膠類型、技術、層類型、產量和應用分類-全球預測,2026-2032年氣泡膜校準器市場按技術、校準類型、頻率、形式、精度、應用和最終用途分類,全球預測(2026-2032年)薄膜整理機市場:依部署模式、產品類型、技術、定價模式、最終用戶和通路分類,全球預測,2026-2032年 全球聚氨酯加工機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚氨酯加工機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球塑膠加工機械市場報告2026年全球塑膠加工設備市場報告2026年全球聚氨酯加工機械市場報告

2026年全球塑膠加工機械市場報告2026年全球塑膠加工設備市場報告2026年全球聚氨酯加工機械市場報告