|

市場調查報告書

商品編碼

2019180

從 2026 年到 2034 年,對電線電纜用聚合物市場的商業機會、成長要素、產業趨勢分析和預測進行了分析。Wire and Cable Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2034 |

||||||

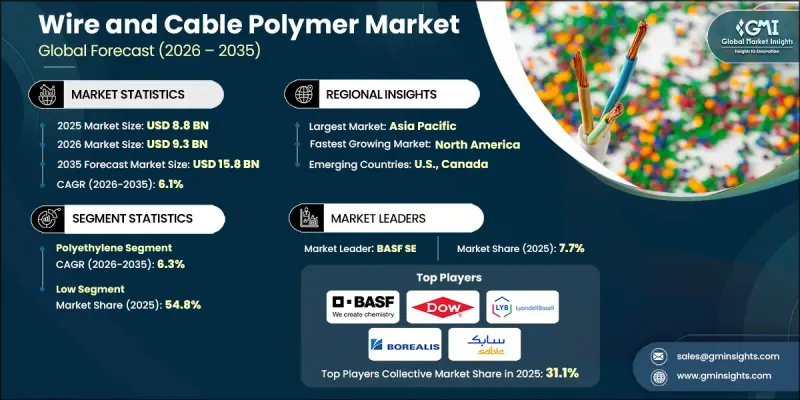

2025年全球電線電纜用聚合物市場價值為88億美元,預計2035年將以6.1%的複合年成長率成長至158億美元。

受建築、汽車、電信和能源等產業需求成長的推動,市場正經歷強勁成長。主要市場趨勢包括從傳統聚合物材料轉向先進的高性能聚合物,例如交聯聚乙烯 (XLPE)、熱可塑性橡膠(TPE) 和阻燃塑膠,這些聚合物具有卓越的耐久性、柔軟性和安全性。這些現代聚合物因其優異的電絕緣性、抗環境應力性能以及防止短路和功率損耗的能力而日益普及。它們的應用範圍廣泛,包括建築業的電力和佈線系統、汽車行業的線束和電子元件、電信業的光纖電纜以及可再生能源行業的太陽能和風能電纜。耐化學腐蝕性、輕量化設計、易於加工和長期可靠性等關鍵優勢持續推動聚合物在全球電線電纜應用中的廣泛應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 88億美元 |

| 預測金額 | 158億美元 |

| 複合年成長率 | 6.1% |

低壓電纜(50V–1kV)市佔率佔55.1%,預計2026年至2035年將以6.8%的複合年成長率成長。此細分市場廣泛應用於住宅和商業領域,其成長主要受都市化、智慧建築發展以及節能佈線解決方案的推廣應用所驅動。政府和私人部門對智慧電網現代化和可再生能源併網的投資,進一步推動了對用於低壓電纜的耐用、高性能聚合物的需求,尤其注重安全性、可靠性和環境永續性。

預計到2025年,建築和基礎設施產業將佔據27.2%的市場佔有率,並在2035年之前以6.9%的複合年成長率成長。都市化、智慧城市計畫和大規模基礎設施建設持續推動著對堅固耐用、使用壽命長的佈線系統的需求。此外,太陽能和風能等可再生能源項目的擴張也增加了對具有更高熱穩定性、更優異絕緣性能和更強耐久性的聚合物電纜的需求,以應對惡劣的環境條件並確保可靠的電力傳輸。

預計到2025年,北美電線電纜用聚合物市佔率將達到15.1%。該地區市場擴張的驅動力主要來自基礎設施現代化、可再生能源投資以及電信業的成長。電動車的日益普及和智慧電網計畫的推進,正在推動對兼具卓越絕緣性、阻燃性和柔軟性的高性能聚合物的需求。該地區嚴格的安全和環境法規促使製造商開發環保阻燃聚合物電纜,力求在產品創新、永續性和法規遵循之間取得平衡。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 基礎建設的擴展

- 汽車電氣化

- 技術進步

- 產業潛在風險與挑戰

- 環境法規

- 原物料價格波動

- 市場機遇

- 高性能聚合物的開發

- 向環保聚合物過渡

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依樹脂類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依樹脂類型分類,2022-2035年

- 聚乙烯

- LDPE

- HDPE

- 超高分子量聚乙烯(UHMWPE)

- XLPE

- LLDPE

- 其他

- 聚丙烯

- 聚氯乙烯

- 聚丁烯對苯二甲酸酯(PBT)

- 無鹵阻燃劑(HFFR)

- 彈性體

- 用於太陽能發電的HFFR-XLPE複合材料

- EVA

- 尼龍

- 其他

第6章 市場估算與預測:依電壓分類,2022-2035年

- 低的

- 中等的

- 高的

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 建築用電線

- 中壓配電線路

- 工業電纜

- 專用電纜

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Arkema SA

- BASF SE

- Borealis AG

- Dow Inc.

- Eastman Chemical Company

- ExxonMobil Corporation

- LG Chem Ltd

- LyondellBasell Industries NV

- Mitsui Chemicals, Inc.

- SABIC

- Solvay SA

- Sumitomo Chemical Co., Ltd.

The Global Wire and Cable Polymer Market was valued at USD 8.8 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 15.8 billion by 2035.

The market is experiencing robust growth due to rising demand across sectors such as construction, automotive, telecommunications, and energy. A key trend in the market is the shift from conventional polymer materials to advanced high-performance polymers, including cross-linked polyethylene (XLPE), thermoplastic elastomers (TPE), and flame-retardant plastics, which offer superior durability, flexibility, and safety. These modern polymers are increasingly preferred because of their excellent electrical insulation, resistance to environmental stress, and capacity to prevent short circuits and power loss. Their applications are widespread: in construction for power and wiring systems, in automotive for wiring harnesses and electronic components, in telecommunications for fiber optic cables, and in renewable energy for solar and wind power cabling. Key benefits such as chemical resistance, lightweight design, ease of processing, and long-term reliability continue to drive polymer adoption in wire and cable applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.8 Billion |

| Forecast Value | $15.8 Billion |

| CAGR | 6.1% |

The low voltage cables (50V-1kV) segment held 55.1% share and is expected to grow at a CAGR of 6.8% from 2026 to 2035. This segment is widely used in residential and commercial applications and has been propelled by urbanization, smart building developments, and the increasing integration of energy-efficient wiring solutions. Investments by governments and private enterprises in smart grid modernization and renewable energy integration have further accelerated demand for durable, high-performance polymers in low-voltage cabling while emphasizing safety, reliability, and environmental sustainability.

The construction and infrastructure sector accounted for 27.2% share in 2025 and is anticipated to grow at a CAGR of 6.9% through 2035. Urbanization, smart city projects, and large-scale infrastructure development continue to drive the need for robust, long-lasting wiring systems. Additionally, the growth of renewable energy projects, such as solar and wind power, has increased demand for polymer cables with higher thermal stability, superior insulation, and enhanced durability to withstand harsh environmental conditions and ensure reliable power transmission.

North America Wire and Cable Polymer Market accounted for 15.1% share in 2025. The region's expansion is fueled by infrastructural modernization, renewable energy investments, and the growth of the telecommunications sector. Rising adoption of electric vehicles and smart grid initiatives has created increasing demand for high-performance polymers that combine excellent insulation, fire resistance, and flexibility. Strict safety and environmental regulations in the region are encouraging manufacturers to develop eco-friendly, flame-retardant polymer cables, aligning product innovation with sustainability and regulatory compliance.

Major companies in the Global Wire and Cable Polymer Market include Dow Inc., Arkema SA, LG Chem Ltd, ExxonMobil Corporation, Borealis AG, LyondellBasell Industries N.V., Solvay SA, Mitsui Chemicals, Inc., Eastman Chemical Company, BASF SE, Sumitomo Chemical Co., Ltd., and SABIC. Leading players in the wire and cable polymer market are adopting several strategies to strengthen their presence and expand market share. They are investing heavily in research and development to create high-performance, eco-friendly polymers with superior insulation, fire resistance, and mechanical properties. Strategic partnerships with manufacturers, construction companies, and energy providers help ensure a consistent supply and market penetration. Companies are also focusing on product diversification to meet the needs of low-, medium-, and high-voltage applications across various industries. Expansion into emerging markets and regional production facilities reduces lead times and cost, while sustainability initiatives, such as biodegradable and flame-retardant polymers, help align with regulatory standards and growing consumer demand for safe, environmentally responsible materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infrastructure development

- 3.2.1.2 Automotive electrification

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental regulations

- 3.2.2.2 Volatility in raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 High-performance polymer development

- 3.2.3.2 Shift towards eco-friendly polymers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By resin

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene

- 5.2.1 LDPE

- 5.2.2 HDPE

- 5.2.3 UHMWPE

- 5.2.4 XLPE

- 5.2.5 LLDPE

- 5.2.6 Others

- 5.3 Polypropylene

- 5.4 Polyvinyl Chloride

- 5.5 Polybutylene Terephthalate (PBT)

- 5.6 Halogen Free Fire Retardant (HFFR)

- 5.7 Elastomers

- 5.8 HFFR-XLPE Photovoltaic Compound

- 5.9 EVA

- 5.10 Nylon

- 5.11 Others

Chapter 6 Market Estimates and Forecast, By Voltage, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building wire

- 7.3 Medium voltage distribution lines

- 7.4 Industrial cables

- 7.5 Special cables

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema SA

- 9.2 BASF SE

- 9.3 Borealis AG

- 9.4 Dow Inc.

- 9.5 Eastman Chemical Company

- 9.6 ExxonMobil Corporation

- 9.7 LG Chem Ltd

- 9.8 LyondellBasell Industries N.V.

- 9.9 Mitsui Chemicals, Inc.

- 9.10 SABIC

- 9.11 Solvay SA

- 9.12 Sumitomo Chemical Co., Ltd.