|

市場調查報告書

商品編碼

2019179

氰乙基乙酸酯市場機會、成長要素、產業趨勢分析及2026-2035年預測。Ethyl Cyanoacetate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

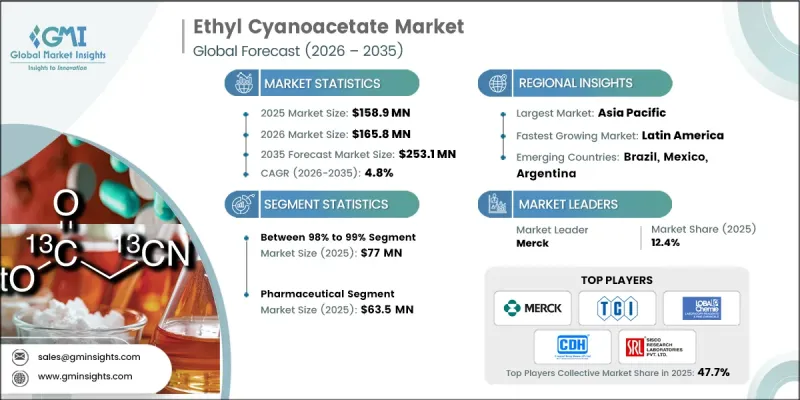

2025 年全球乙基氰基乙基乙酸酯市值為 1.589 億美元,預計到 2035 年將達到 2.531 億美元,年複合成長率為 4.8%。

氰基乙酸乙酯因其多樣的反應活性,被公認為許多產業的重要化學中間體。作為一種含有高反應活性亞甲基的氰基乙酸酯,它能夠促進多種縮合和取代反應,使其成為藥物、農業化學品和特殊化學品合成中不可或缺的原料。在各個產業中,該物質均被用作建構複雜化學結構和多步驟合成路線的基本單元。由於其能夠支持化學製造過程中所需的各種反應機制,因此其工業價值仍然很高。市場擴張主要由其在製藥和作物保護領域的核心應用所驅動,在這些領域,它是合成中間體的重要原料。該物質的成長受原料供應波動的影響較小,而更多地受到研發進展、產能提升和區域製造基礎設施建設的影響,這些因素共同提高了生產的擴充性和穩定性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1.589億美元 |

| 預測金額 | 2.531億美元 |

| 複合年成長率 | 4.8% |

到2025年,純度為98%至99%的產品市場規模將達到7,700萬美元,憑藉其穩定的反應性能和較低的製程變異性,佔據市場主導地位。高純度產品因其能為多步驟合成提供穩定的中間體,確保可預測的產率和高品質的結果,而日益受到製藥、農業化學品和特種化學品製造商的青睞。隨著工業生產技術的進步,對高純度產品的需求預計將穩定成長,凸顯其在可控化學製程的關鍵作用。

預計到2025年,製藥業市場規模將達6,350萬美元。該行業持續需要可靠的中間體,以支持精確的多步驟合成,並在各種反應條件下保持穩定性。化學品和特種化學品產業充分利用乙基氰基乙酸的多功能性,將其應用於需要可控反應路徑的製程。紡織業也使用這些中間體,以確保整個生產線上物料處理的一致性和最終產品的成品效果。

預計北美乙基氰基乙酸市場規模將從2025年的4,760萬美元成長至2035年的7,450萬美元,反映出醫藥、特種化學品和塗料產業對中間體的穩定需求。這一成長得益於先進的合成方法、研發舉措以及對工業基礎設施的持續投資,這些因素共同促成了高品質、高穩定性中間體的生產。美國仍然是主要貢獻國,憑藉配方開發和多步驟化學加工能力的持續創新,確保了工業應用中間體的可靠供應。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對支持先進藥物合成的中間體的需求日益成長。

- 在多種農業化學配方中穩定使用

- 在特種化學品和精細化學品生產中日益重要

- 陷阱與挑戰

- 原料的波動會影響全球生產的穩定性。

- 嚴格的操作要求增加了營運和合規方面的工作量。

- 機會

- 複雜反應中對高純度中間體的需求日益成長。

- 新興工業區精細化工製造業的擴張

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 純度

- 未來市場趨勢

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依純度分類,2022-2035年

- 低於98%

- 98%~99%

- 超過99%

第6章 市場估計與預測:依最終用途產業分類,2022-2035年

- 製藥

- 化學

- 纖維

- 化妝品和個人護理

- 其他

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章:公司簡介

- Pravin Dychem

- SimSon Pharma

- Central Drug House

- Tokyo Chemical Industry

- Emco Dyestuff

- Merck

- Shandong Xinhua Pharma

- Loba Chemie

- Tiande Chemical

- Sisco Research Laboratories

- HeBei ChengXin

The Global Ethyl Cyanoacetate Market was valued at USD 158.9 million in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 253.1 million by 2035.

Ethyl cyanoacetate is recognized as a vital chemical intermediate across multiple industries due to its versatile reactivity. As a cyanoacetate ester with a reactive methylene group, it facilitates a range of condensation and substitution reactions, making it indispensable for the synthesis of pharmaceuticals, agrochemicals, and specialty chemicals. Industries rely on it as a building block to construct complex chemical structures and multi-step synthesis pathways efficiently. Its industrial relevance remains strong because it supports diverse reaction mechanisms required in chemical manufacturing processes. Market expansion is driven by its core applications in the pharmaceutical and crop protection sectors, where it serves as a primary raw material for intermediates. Growth is less affected by fluctuations in raw material supply and more influenced by research developments, production capabilities, and regional manufacturing infrastructure, which collectively enhance production scalability and consistency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $158.9 Million |

| Forecast Value | $253.1 Million |

| CAGR | 4.8% |

The Purity levels between 98% and 99% accounted for USD 77 million in 2025, dominating in value due to their consistent reaction performance and reduced process variability. High-purity grades are increasingly preferred by pharmaceutical, agrochemical, and specialty chemical manufacturers because they provide stable intermediates for multi-step synthesis, ensuring predictable yields and high-quality outputs. As industrial production techniques advance, demand for refined purity grades is projected to grow steadily, underscoring their critical role in controlled chemical processing.

The pharmaceutical segment reached USD 63.5 million in 2025. This sector continues to demand reliable intermediates that support precise multi-step synthesis and maintain stability under varying reaction conditions. Chemical and specialty chemical segments benefit from ethyl cyanoacetate's versatility, using it in processes that require controlled reaction pathways. The textiles sector also leverages these intermediates for processes that ensure uniform material treatment and consistent finishing results across production lines.

North America Ethyl Cyanoacetate Market is anticipated to grow from USD 47.6 million in 2025 to USD 74.5 million in 2035, reflecting steady demand for pharmaceutical, specialty chemical, and coating intermediates. Growth is supported by continuous investments in advanced synthesis methods, research initiatives, and industrial infrastructure capable of producing consistent, high-quality intermediates. The United States remains a major contributor, driven by ongoing innovation in formulation development and multi-step chemical processing capabilities, ensuring the availability of reliable intermediates for industrial applications.

Key players in the Global Ethyl Cyanoacetate Market include Sisco Research Laboratories, Merck, Central Drug House, Loba Chemie, Tokyo Chemical Industry, Emco Dyestuff, Shandong Xinhua Pharma, Hebei ChengXin, Tiande Chemical, Pravin Dychem, and SimSon Pharma. Companies in the Ethyl Cyanoacetate Market are adopting multiple strategies to strengthen their market position. They focus on expanding production capacities to meet growing industrial demand and improve supply chain reliability. Strategic partnerships and collaborations with pharmaceutical and agrochemical manufacturers help secure long-term contracts and consistent off-take agreements. Investments in research and development support the creation of high-purity grades and innovative chemical intermediates, enhancing product differentiation. Companies also emphasize regulatory compliance, safety management, and sustainable manufacturing practices to build trust with clients and improve brand reputation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Purity

- 2.2.2 End Use Industry

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising need for intermediates supporting advanced pharmaceutical synthesis

- 3.2.1.2 Steady usage in agrochemical formulations across multiple applications

- 3.2.1.3 Increasing relevance in specialty chemical and fine chemical production

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Variability in raw materials affecting production consistency globally

- 3.2.2.2 Strict handling requirements increasing operational and compliance efforts

- 3.2.3 Opportunities

- 3.2.3.1 Growing preference for high purity intermediates in complex reactions

- 3.2.3.2 Expansion of fine chemical manufacturing across emerging industrial regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By purity

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Purity, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Less than 98%

- 5.3 Between 98% to 99%

- 5.4 More than 99%

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pharmaceutical

- 6.3 Chemical

- 6.4 Textiles

- 6.5 Cosmetics & Personal Care

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Pravin Dychem

- 8.2 SimSon Pharma

- 8.3 Central Drug House

- 8.4 Tokyo Chemical Industry

- 8.5 Emco Dyestuff

- 8.6 Merck

- 8.7 Shandong Xinhua Pharma

- 8.8 Loba Chemie

- 8.9 Tiande Chemical

- 8.10 Sisco Research Laboratories

- 8.11 HeBei ChengXin

氰乙基市場:依純度等級、生產流程、終端應用產業及通路分類-2026-2032年全球市場預測

氰乙基市場:依純度等級、生產流程、終端應用產業及通路分類-2026-2032年全球市場預測 氰基乙酸乙酯市場規模及佔有率分析:趨勢、驅動因素、競爭格局及預測(2026-2032)

氰基乙酸乙酯市場規模及佔有率分析:趨勢、驅動因素、競爭格局及預測(2026-2032) 全球氰乙酸乙酯市場

全球氰乙酸乙酯市場 2030 年氰乙酸乙酯市場預測:按等級、功能、應用和地區進行的全球分析

2030 年氰乙酸乙酯市場預測:按等級、功能、應用和地區進行的全球分析