|

市場調查報告書

商品編碼

2019169

真無線立體聲耳機市場機會、成長要素、產業趨勢分析及2026-2035年預測True Wireless Stereo Earbuds Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

預計到 2025 年,全球真無線立體聲耳機市場價值將達到 393 億美元,並將以 17.6% 的複合年成長率成長,到 2035 年達到 1,920 億美元。

智慧型手機、筆記型電腦、平板電腦和穿戴式裝置的普及推動了市場成長,無線音訊解決方案已成為日常生活不可或缺的一部分。消費者越來越依賴真無線耳機 (TWS) 來進行娛樂、通訊、健身和在家工作。消費者對卓越音質、沉浸式體驗以及主動降噪 (ANC) 和空間音訊等先進功能的期望不斷提高,迫使製造商以前所未有的速度進行創新。藍牙技術的進步,包括藍牙 5.0 和 5.1 的應用,提高了連接穩定性、降低了延遲、擴展了傳輸距離並提升了電池效率。此外,人體工學設計、緊湊的外形尺寸和音頻驅動單元的改進,使真無線耳機成為高度便攜、舒適且用途廣泛的產品,適用於各種活動,從而加速了其在全球消費者中的普及。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 393億美元 |

| 預測金額 | 1920億美元 |

| 複合年成長率 | 17.6% |

預計到2025年,入耳式真無線立體聲(TWS)耳機市場規模將達到342億美元,並在2035年之前以17.7%的複合年成長率成長。入耳式耳機因其貼合耳道、提供卓越的被動降噪效果和更沉浸式的音頻體驗而廣受歡迎,相比頭戴式耳機,其優勢顯而易見。輕巧緊湊的設計和極佳的便攜性使其成為日常通勤、運動和外出使用的理想之選,同時也符合消費者對便利無線設備的需求。憑藉舒適性、清晰度和人體工學設計的完美平衡,入耳式耳機持續引領市場,吸引了從一般使用者到追求卓越音質的發燒友等各類使用者。

預計到2025年,藍牙連接市佔率將達到74.4%,並在2026年至2035年間維持17.7%的複合年成長率。藍牙已成為無線音訊的通用標準,幾乎相容於所有現代智慧型手機、筆記型電腦、平板電腦和穿戴式裝置。包括藍牙5.0和5.1在內的持續技術改進,帶來了更高的穩定性、更低的延遲、更遠的傳輸距離和更最佳化的電源效率。這些升級使真無線耳機(TWS)能夠在音樂播放、語音通話、遊戲和混合辦公場景中提供高品質音訊、無縫設備切換和穩定的性能。藍牙技術的優勢在於其便捷性、廣泛的設備相容性和可靠性,使其成為消費者和製造商的首選。

美國真無線立體聲 (TWS) 耳機市場預計到 2025 年將達到 94 億美元,並在 2035 年前以 18% 的複合年成長率成長。智慧型手機、平板電腦、智慧型手錶和筆記型電腦的日益普及推動了無線音訊解決方案的快速發展,其中許多設備都取消了 3.5 毫米耳機介面。美國消費者也十分重視高音質、主動降噪 (ANC)、空間聲學和高解析度無線播放,這進一步提升了高階 TWS 耳機的受歡迎程度。此外,串流媒體服務、行動娛樂和混合辦公環境的興起也增加了對通話清晰、隔音效果好、音效沉浸感強的設備的需求,使得 TWS 耳機成為日常溝通、休閒和提高工作效率的必備配件。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 智慧型手機和智慧型裝置的普及率不斷提高

- 先進的音訊功能和廣泛的主動降噪功能

- 無線和藍牙技術的進步

- 產業潛在風險與挑戰

- 連線性和延遲問題

- 電池的限制以及小型化帶來的權衡取捨

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 貿易數據分析

- 進出口數量和價值的變化趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- Genai 各細分市場的應用案例與實施藍圖

- 風險、限制和監管考量

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 入耳式

- 耳罩式

第6章 市場估算與預測:以連結方式分類,2022-2035年

- Bluetooth

- RF

- NFC

- 其他(Wi-Fi 等)

第7章 市場估價與預測:依電池壽命分類,2022-2035年

- 12小時或更短

- 12-24小時

- 超過24小時

第8章 市場估計與預測:依價格分類,2022-2035年

- 低的

- 中等的

- 高的

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 音樂與娛樂

- 溝通

- 遊戲

- 健身與運動

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 企業網站

- 電子商務

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(例如,大型超市)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- Apple

- Belkin

- Blaupunkt

- Bose

- Creative Technology

- Havit

- House of Marley

- Jabra

- Jays Headphones

- Masimo

- Master & Dynamic

- Samsung

- Skullcandy

- Sonova

- Sony

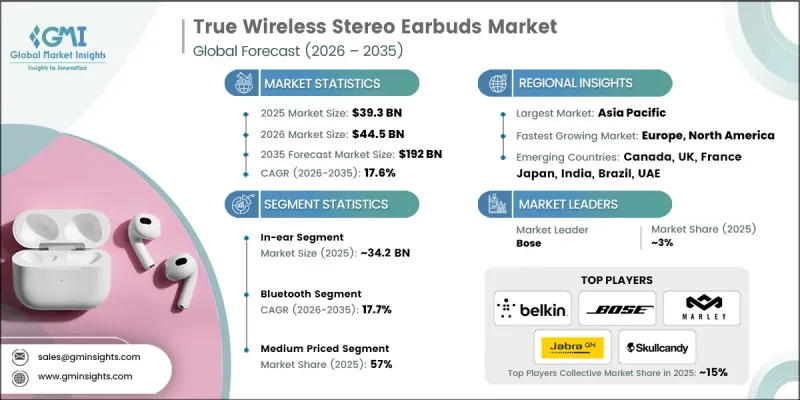

The Global True Wireless Stereo Earbuds Market was valued at USD 39.3 billion in 2025 and is estimated to grow at a CAGR of 17.6% to reach USD 192 billion by 2035.

Market growth is fueled by the widespread penetration of smartphones, laptops, tablets, and wearable devices, which have made wireless audio solutions an essential part of everyday life. Consumers increasingly rely on TWS earbuds for entertainment, communication, fitness, and work-from-home setups. Rising expectations for superior sound quality, immersive experiences, and advanced features such as Active Noise Cancellation (ANC) and spatial audio are pushing manufacturers to innovate at an unprecedented pace. Technological improvements in Bluetooth, including the adoption of Bluetooth 5.0 and 5.1, have enhanced connection stability, reduced latency, increased wireless range, and improved battery efficiency. Additionally, advancements in ergonomic design, compact form factors, and improved audio drivers have made TWS earbuds highly portable, comfortable, and versatile for a range of activities, driving broader consumer adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.3 Billion |

| Forecast Value | $192 Billion |

| CAGR | 17.6% |

In 2025, the in-ear TWS earbuds generated USD 34.2 billion and are expected to grow at a CAGR of 17.7% through 2035. In-ear variants are highly popular due to their snug fit within the ear canal, offering superior passive noise isolation and a more immersive audio experience compared to over-ear models. Their lightweight, compact design and portability make them ideal for daily commuting, workouts, and on-the-go use, aligning with the increasing consumer preference for wire-free and convenient devices. The segment continues to dominate due to its ability to balance comfort, sound clarity, and ergonomic functionality, catering to both casual listeners and audiophiles seeking premium performance.

The Bluetooth connectivity segment held a 74.4% share in 2025 and is expected to maintain a CAGR of 17.7% from 2026 to 2035. Bluetooth has become the universal standard for wireless audio, compatible with nearly all modern smartphones, laptops, tablets, and wearable devices. Continuous technological enhancements, including Bluetooth 5.0 and 5.1, have improved stability, reduced latency, extended transmission range, and optimized power efficiency. These upgrades have enabled TWS earbuds to deliver high-fidelity audio, seamless device switching, and stable performance during music playback, voice calls, gaming, and hybrid work scenarios. The dominance of Bluetooth technology reflects its convenience, broad device compatibility, and reliability, making it the preferred choice for consumers and manufacturers alike.

United States True Wireless Stereo Earbuds Market captured USD 9.4 billion in 2025, and is projected to grow at a CAGR of 18% through 2035. The high adoption of smartphones, tablets, smartwatches, and laptops, many of which have eliminated the 3.5 mm headphone jack, drives the rapid uptake of wireless audio solutions. U.S. consumers also prioritize high-quality audio, ANC, spatial sound, and high-resolution wireless playback, supporting the adoption of premium TWS earbuds. Additionally, the rise of streaming services, mobile entertainment, and hybrid work environments has amplified demand for devices offering clear calls, noise isolation, and immersive sound, making TWS earbuds a staple accessory for daily communication, leisure, and productivity.

Major players operating in the Global True Wireless Stereo Earbuds Market include Apple, Bose, Belkin, Creative Technology, Havit, House of Marley, Jabra, Jays Headphones, Masimo, Master & Dynamic, Samsung, Skullcandy, Sony, Sonova, and Blaupunkt. Companies in the true wireless stereo earbuds market are strengthening their market presence through several strategic initiatives. They invest heavily in research and development to enhance audio performance, battery efficiency, and connectivity stability. Firms are forming partnerships with smartphone and wearable device manufacturers to ensure seamless integration and broad compatibility. Marketing campaigns emphasize premium features such as ANC, spatial sound, and customizable EQ settings to attract tech-savvy consumers. Expanding global distribution networks, including e-commerce platforms and flagship retail stores, helps increase accessibility and brand visibility. Additionally, companies focus on product differentiation through collaborations with audio engineers, limited-edition releases, and user-centric design improvements. Continuous software updates, bundled apps, and loyalty programs further enhance customer engagement and retention, solidifying their foothold in the competitive TWS earbuds market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Connectivity

- 2.2.4 Battery Life

- 2.2.5 Price

- 2.2.6 Application

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising smartphone & smart device penetration

- 3.2.1.2 Enhanced audio features & ANC adoption

- 3.2.1.3 Advancements in wireless & bluetooth technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Connectivity & latency issues

- 3.2.2.2 Battery limitations & miniaturization trade-offs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Trade data analysis

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Impact of ai & generative ai on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 Genai use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirements

- 3.9.2 Regional regulatory frameworks

- 3.9.3 Certification standards

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 In-ear

- 5.3 Over-ear

Chapter 6 Market Estimates & Forecast, By Connectivity, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Bluetooth

- 6.3 RF

- 6.4 NFC

- 6.5 Others (Wi-Fi etc.)

Chapter 7 Market Estimates & Forecast, By Battery Life, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Up to 12 hours

- 7.3 12 to 24 hours

- 7.4 Above 24 hours

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Music & entertainment

- 9.3 Communication

- 9.4 Gaming

- 9.5 Fitness & sports

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 Company websites

- 10.2.2 E-commerce

- 10.3 Offline

- 10.3.1 Supermarket/hypermarket

- 10.3.2 Specialty stores

- 10.3.3 Others (mega retail store etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Apple

- 12.2 Belkin

- 12.3 Blaupunkt

- 12.4 Bose

- 12.5 Creative Technology

- 12.6 Havit

- 12.7 House of Marley

- 12.8 Jabra

- 12.9 Jays Headphones

- 12.10 Masimo

- 12.11 Master & Dynamic

- 12.12 Samsung

- 12.13 Skullcandy

- 12.14 Sonova

- 12.15 Sony

耳機與耳塞市場:2026-2032年全球市場預測(依產品類型、連接方式、降噪功能、電池續航力、應用及銷售管道)

耳機與耳塞市場:2026-2032年全球市場預測(依產品類型、連接方式、降噪功能、電池續航力、應用及銷售管道) 全球即時翻譯耳機銷售市場報告、競爭分析及區域機會(2026-2032年)耳機市場:2026-2032年全球市場預測(依產品類型、價格範圍、應用、連結技術及通路分類)

全球即時翻譯耳機銷售市場報告、競爭分析及區域機會(2026-2032年)耳機市場:2026-2032年全球市場預測(依產品類型、價格範圍、應用、連結技術及通路分類) 全球耳機和耳塞市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球耳機和耳塞市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026-2030年全球真無線立體聲(TWS)耳機市場

2026-2030年全球真無線立體聲(TWS)耳機市場 耳機市場分析及預測(至2035年):依類型、產品類型、技術、應用、形狀、材質、設備、最終用戶、功能及模式分類

耳機市場分析及預測(至2035年):依類型、產品類型、技術、應用、形狀、材質、設備、最終用戶、功能及模式分類 耳機市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、連接方式、應用、地區和競爭格局分類),2021-2031年入耳式監聽耳機市場按類型、技術、應用和分銷管道分類,全球預測(2026-2032年)睡眠耳機市場按產品類型、技術、價格範圍、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

耳機市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、連接方式、應用、地區和競爭格局分類),2021-2031年入耳式監聽耳機市場按類型、技術、應用和分銷管道分類,全球預測(2026-2032年)睡眠耳機市場按產品類型、技術、價格範圍、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 耳機市場規模、佔有率及成長分析(依產品類型、技術、價格範圍、通路、最終用戶及地區分類)-2026-2033年產業預測

耳機市場規模、佔有率及成長分析(依產品類型、技術、價格範圍、通路、最終用戶及地區分類)-2026-2033年產業預測