|

市場調查報告書

商品編碼

2019164

互鎖鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測Interlocked Armored Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

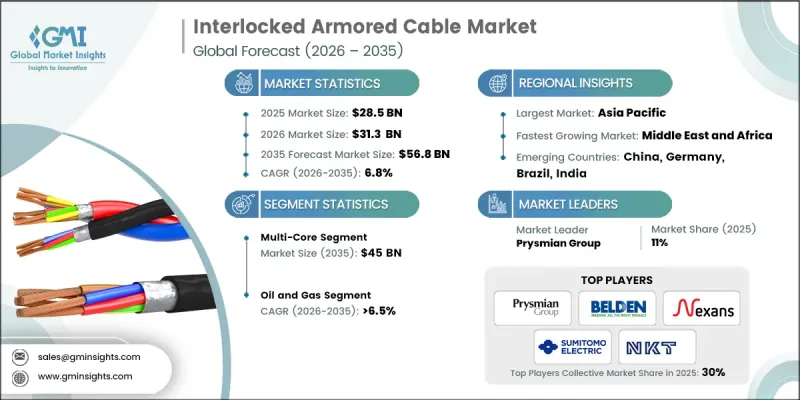

2025 年全球連鎖鎧裝電纜市場規模預計為 285 億美元,預計到 2035 年將以 6.8% 的複合年成長率成長至 568 億美元。

這一成長主要源於對能夠承受機械應力、惡劣環境和長運作的電纜日益成長的需求。這些電纜廣泛應用於關鍵領域,因為它們能夠在複雜的安裝環境中提供高水準的保護、可靠性和安全性。新興經濟體的快速城市化和持續工業化正在創造對先進配電系統的持續需求。此外,對高效能電力傳輸和安全連接解決方案日益成長的需求也進一步推動了市場擴張。各行各業對即使在惡劣條件下也能保證不間斷運作的堅固耐用的電纜解決方案越來越感興趣。除了對基礎設施現代化建設的持續投資外,自動化和數位系統的整合正在加速互鎖鎧裝電纜在多個領域的應用,進一步提升了其在現代電力網路中的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 285億美元 |

| 預測金額 | 568億美元 |

| 複合年成長率 | 6.8% |

隨著能源密集產業的擴張,對穩健電力系統的需求持續成長,進而推動了對互鎖鎧裝電纜的需求。電力基礎設施和電網現代化改造投資的增加,創造了市場成長機會。可再生能源系統和大規模能源網路的日益普及也促進了這一成長。這些電纜具有極強的抗外部應力和環境侵蝕能力。即使在惡劣條件下,它們也能保持穩定的性能,使其成為大規模裝置的理想選擇。此外,工業和商業環境中嚴格的安全標準和監管要求也推動了保護性電纜系統的使用,促進了其在各個高需求行業的廣泛應用。

預計到2035年,多芯電纜市場規模將達到450億美元,這主要得益於工業活動的活性化以及電纜設計和製造流程的不斷進步。這些電纜之所以備受關注,是因為它們能夠在單一結構內傳輸多個電路,從而提高效率並降低安裝複雜性。其緊湊的結構有助於最佳化空間利用率,同時降低系統總成本。在複雜的基礎設施環境中,對結構化、高容量佈線解決方案的需求不斷成長,進一步推動了該市場的成長。此外,這些電纜的耐用性和性能特性使其適用於嚴苛的運作環境,從而支援其在各種工業應用中的廣泛使用。

預計到2035年,石油和天然氣產業將以6.5%的複合年成長率成長,這主要得益於在嚴苛的運作環境下對高可靠性和長壽命電氣解決方案的需求。互鎖鎧裝電纜因其能夠承受機械應力、腐蝕和環境侵蝕,確保關鍵運作中的穩定性能而被廣泛採用。能源生產活動的持續擴張以及對營運效率日益成長的關注,都進一步推動了對互鎖鎧裝電纜的需求。此外,對能夠最大限度減少停機時間並支援連續運作的可靠基礎設施的需求,也進一步鞏固了互鎖鎧裝電纜在能源相關應用中的重要地位。

預計到2035年,美國互鎖鎧裝電纜市場規模將達80億美元,主要得益於各行業對先進、高可靠性電氣系統需求的不斷成長。基礎設施建設、電網現代化以及先進技術的整合是該地區市場成長的關鍵促進因素。隨著各行業將安全、效率和長期可靠性置於優先地位,對高性能電纜解決方案的需求日益成長。這些電纜因其強度高、耐溫差大以及能夠在惡劣環境下有效運作等優點而被廣泛應用,使其成為大規模工業和商業應用中不可或缺的組件。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 區域價格趨勢分析(美元/單位)

- 新機會和趨勢

- 數位化和物聯網整合

- 進入新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 互鎖鎧裝電纜市場規模及預測:依芯線類型分類,2022-2035年

- 單核

- 多核心

第6章 聯鎖鎧裝電纜市場規模及預測:依最終用戶分類,2022-2035年

- 石油和天然氣

- 製造業

- 礦業

- 建造

- 其他

第7章 互鎖鎧裝電纜市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- Anixter

- AT&T

- Atkore

- Belden

- Finolex

- Furukawa Electric

- Havells

- Helukabel

- KEI Industries

- Leoni Cables

- LS Cable & System

- Nexans

- NKT

- Okonite

- Omni Cables

- Polycab

- Prysmian

- Riyadh Cables

- RR Kabel

- Southwire

- Sumitomo Electric

The Global Interlocked Armored Cable Market was valued at USD 28.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 56.8 billion by 2035.

Growth is driven by the increasing need for cables that can tolerate mechanical stress, harsh environments, and long operational lifecycles. These cables are widely utilized in critical applications due to their ability to provide enhanced protection, reliability, and safety in complex installations. Rapid urban development and ongoing industrialization across emerging economies are creating sustained demand for advanced electrical distribution systems. Additionally, the rising need for efficient power transmission and secure connectivity solutions is further strengthening market expansion. Industries are increasingly focusing on robust cable solutions that ensure uninterrupted performance under demanding conditions. Continuous investments in infrastructure modernization, along with the integration of automation and digital systems, are accelerating the adoption of interlocked armored cables across multiple sectors, reinforcing their importance in modern electrical networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28.5 Billion |

| Forecast Value | $56.8 Billion |

| CAGR | 6.8% |

Demand for interlocked armored cables continues to rise as energy-intensive industries expand and require resilient electrical systems. Growing investments in power infrastructure and grid modernization are creating long-term opportunities for market growth. The increasing deployment of renewable energy systems and large-scale energy networks is contributing to higher adoption, as these cables offer strong resistance to external stress and environmental exposure. Their capability to maintain performance stability in challenging conditions makes them highly suitable for large-scale installations. Furthermore, stringent safety standards and regulatory requirements in industrial and commercial environments are encouraging the use of protected cable systems, supporting widespread adoption across various high-demand sectors.

The multi-core segment is expected to reach USD 45 billion by 2035, supported by rising industrial activities and continuous advancements in cable design and manufacturing processes. These cables are gaining traction due to their ability to carry multiple circuits within a single structure, improving efficiency and reducing installation complexity. Their compact configuration helps optimize space utilization while lowering overall system costs. Increasing demand for organized and high-capacity wiring solutions in complex infrastructure environments is further strengthening segment growth. Additionally, improvements in durability and performance characteristics make these cables suitable for challenging operating environments, supporting their expanding use across a wide range of industrial applications.

The oil and gas segment is projected to grow at a CAGR of 6.5% through 2035, driven by the need for highly reliable and long-lasting electrical solutions in demanding operational settings. Interlocked armored cables are widely adopted due to their ability to withstand mechanical stress, corrosion, and environmental exposure, ensuring consistent performance in critical operations. Ongoing expansion in energy production activities and increased focus on operational efficiency are contributing to higher demand. The need for dependable infrastructure that minimizes downtime and supports continuous operations further strengthens the role of these cables in energy-related applications.

U.S. Interlocked Armored Cable Market is anticipated to reach USD 8 billion by 2035, supported by rising demand for advanced and resilient electrical systems across key industries. Infrastructure development, modernization of electrical networks, and increasing integration of advanced technologies are key factors driving regional growth. The demand for high-performance cabling solutions is increasing as industries prioritize safety, efficiency, and long-term reliability. These cables are widely utilized due to their strength, resistance to temperature variations, and ability to perform effectively in challenging conditions, making them essential for large-scale industrial and commercial applications.

Key companies operating in the Global Interlocked Armored Cable Market include Prysmian, Nexans, Belden, Polycab, KEI Industries, RR Kabel, Southwire, Sumitomo Electric, Furukawa Electric, LS Cable & System, NKT, Leoni Cables, Helukabel, Havells, Finolex, Riyadh Cables, Okonite, Omni Cables, Atkore, Anixter, and AT&T. Companies in the Interlocked Armored Cable Market are focusing on strengthening their competitive position through product innovation, capacity expansion, and strategic collaborations. Manufacturers are investing in advanced materials and improved insulation technologies to enhance cable durability and performance. Expanding production capabilities and optimizing supply chains help meet growing global demand while maintaining cost efficiency. Strategic partnerships with infrastructure developers and energy companies enable wider market reach and project integration. Firms are also prioritizing compliance with international safety and quality standards to build trust and credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis, by region (USD/Unit)

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Mergers & acquisitions

- 4.3.2 Partnerships & collaborations

- 4.3.3 New product launches

- 4.3.4 Expansion plans and funding

Chapter 5 Interlocked Armored Cable Market Size and Forecast, By Core Type, 2022 - 2035 (USD Million & '000 Tonnes)

- 5.1 Key trends

- 5.2 Single Core

- 5.3 Multi-Core

Chapter 6 Interlocked Armored Cable Market Size and Forecast, By End User, 2022 - 2035 (USD Million & '000 Tonnes)

- 6.1 Key trends

- 6.2 Oil & Gas

- 6.3 Manufacturing

- 6.4 Mining

- 6.5 Construction

- 6.6 Others

Chapter 7 Interlocked Armored Cable Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Tonnes)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Anixter

- 8.2 AT&T

- 8.3 Atkore

- 8.4 Belden

- 8.5 Finolex

- 8.6 Furukawa Electric

- 8.7 Havells

- 8.8 Helukabel

- 8.9 KEI Industries

- 8.10 Leoni Cables

- 8.11 LS Cable & System

- 8.12 Nexans

- 8.13 NKT

- 8.14 Okonite

- 8.15 Omni Cables

- 8.16 Polycab

- 8.17 Prysmian

- 8.18 Riyadh Cables

- 8.19 RR Kabel

- 8.20 Southwire

- 8.21 Sumitomo Electric

石油及天然氣鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測多芯鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測。CCW鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測

石油及天然氣鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測多芯鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測。CCW鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測鎧裝電纜市場機會、成長要素、產業趨勢分析及2026-2035年預測 鎧裝電纜市場 - 全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)

鎧裝電纜市場 - 全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年) 耐油電纜市場(按絕緣材料、電壓、導體材料和應用)—2025-2030 年全球預測

耐油電纜市場(按絕緣材料、電壓、導體材料和應用)—2025-2030 年全球預測 全球互鎖鎧裝電纜市場全球多芯鎧裝電纜市場全球鎧裝電纜市場鎧裝電纜市場按鎧裝類型、安裝類型、分銷管道、最終用途行業分類 - 2025-2030 年全球預測

全球互鎖鎧裝電纜市場全球多芯鎧裝電纜市場全球鎧裝電纜市場鎧裝電纜市場按鎧裝類型、安裝類型、分銷管道、最終用途行業分類 - 2025-2030 年全球預測