|

市場調查報告書

商品編碼

2019163

孕婦裝市場商機、成長要素、產業趨勢分析及2026-2035年預測。Maternity Apparel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

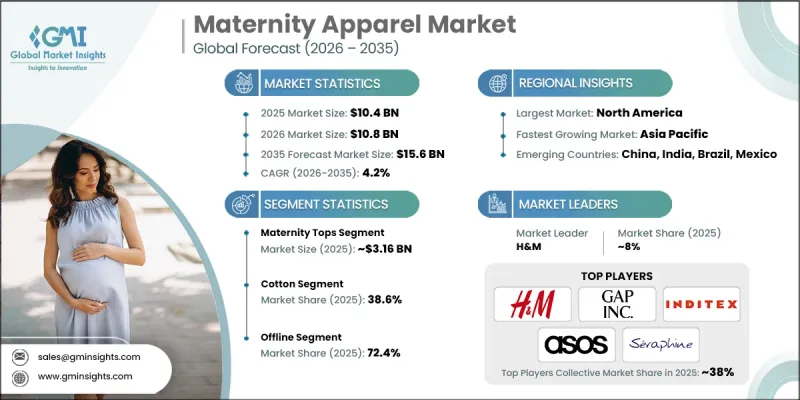

2025年全球孕婦裝市場價值104億美元,預計2035年將達到156億美元,年複合成長率為4.2%。

孕婦裝產業的成長主要得益於孕婦對兼具舒適性和時尚感的服裝的偏好日益成長。孕婦勞動參與率的提高,以及她們保持個人時尚風格的強烈願望,支撐著各地穩定的市場需求。孕婦積極尋找既能適應懷孕期間體型變化,也適合日常穿著和職場的服裝。產品類型也不斷發展,以滿足包括日常穿著、工作服和健康相關活動在內的多樣化生活方式需求。紡織技術的進步使品牌能夠提供柔軟性、透氣性和支撐性的布料,從而提升整體舒適度。此外,身體正向概念的傳播和人們對孕期時尚觀念的轉變也增強了市場的發展動能。數位零售平台和線下通路的拓展進一步提升了產品的可近性。涵蓋上衣、下裝、睡衣和內衣等各種孕婦裝產品,持續推動著消費者的參與和市場的永續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 104億美元 |

| 預測金額 | 156億美元 |

| 複合年成長率 | 4.2% |

預計到2025年,孕婦上衣市場規模將達到31.6億美元,並在2035年之前以4.6%的複合年成長率成長。該細分市場憑藉其多功能性、成本績效和頻繁的更換週期,保持主導地位。這些服裝的設計旨在透過彈性布料和靈活剪裁等適應性功能,適應孕期身體的變化。消費者需要為不同場合準備多套服裝,這推動了重複購買。這些上衣可以與現有服裝搭配,進一步提升了其實用性。不斷創新的設計,包括多樣化的剪裁和款式,支撐著消費者的濃厚興趣和持續的需求。

預計到2025年,棉織物市場佔有率將達到38.6%,並在2035年之前以4.6%的複合年成長率成長。棉織物因其柔軟、透氣和天然特性而備受青睞。即使是敏感肌膚也能感受到棉織物的舒適,棉織物也有助於體溫調節,因此適合長時間穿著。人們對織物安全性的日益關注以及對天然和有機材料興趣的不斷成長,進一步推動了棉織物的需求。棉混紡布料因其兼具舒適性和彈性,正被擴大應用於各種產品類型。

美國孕婦裝市場預計到2025年將達到28億美元,並在2026年至2035年間以4.8%的複合年成長率成長。市場擴張的促進因素包括孕婦就業率的提高、時尚偏好的轉變以及成熟的零售生態系統。兼具功能性和時尚感的服裝需求持續成長,尤其是在工作服和休閒領域。消費者越來越追求舒適與現代設計兼具的產品。由於完善的零售網路和不斷發展的電子商務平台,產品的供應情況正在改善。製造商正致力於提升服裝的合身度、提供更全面的尺寸選擇以及創新布料,以滿足消費者不斷變化的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 孕婦勞動參與率提高

- 人們越來越關注孕期舒適和健康。

- 電子商務和線上孕婦裝零售的擴張

- 產業潛在風險與挑戰

- 該產品的使用壽命較短,而且在衣櫥方面的投資有限。

- 與具有拉伸功能的普通服飾競爭。

- 機會

- 對永續和有機孕婦裝布料的需求日益成長。

- 大尺碼和包容性孕婦裝的擴張。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 交易數據分析(基於初步調查)

- 進出口量和進出口額趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- HS編碼分類及貿易流量分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和通路形式(現代通路與傳統通路)分類的通路覆蓋率(基於初步調查)

- 最後一公里基礎設施的不足和新分銷管道的變化(基於初步研究)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 估價與預測:依產品類型分類,2022-2035年

- 孕婦上衣

- T恤

- 女式襯衫

- 其他(束腰外衣等)

- 孕婦褲

- 褲子

- 貼身褲

- 裙子

- 概述

- 孕婦外套

- 夾克

- 外套

- 其他(毛衣等)

- 孕婦內衣

- 哺乳胸罩

- 女用貼身內衣

- 其他物品(例如吊帶背心)

- 孕婦睡衣

- 罩衣

- 睡衣

- 休閒褲

- 其他物品(睡衣套裝、睡袍等)

第6章 估算與預測:依材料分類,2022-2035年

- 棉布

- 聚酯纖維

- 氨綸

- 模態

- 其他

第7章 估價與預測:依價格區間分類,2022-2035年

- 低價位(50美元以下)

- 中價位(50-100美元)

- 高價位(超過100美元)

第8章 估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 批發和分銷代理商

- 大賣場/超級市場

- 專賣店

- 多品牌商店

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Adidas AG

- ASOS Maternity

- Cake Maternity

- Gap Inc

- H&M

- Hatch Collection LLC

- Inditex(Zara)

- Ingrid &Isabel, LLC

- Isabella Oliver Limited

- JoJo Maman Bebe

- Maternal America, Inc.

- Nike, Inc.

- Old Navy(Gap Inc)

- PinkBlush Maternity

- Seraphine

The Global Maternity Apparel Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 15.6 billion by 2035.

Growth in the maternity clothing industry is driven by a rising preference for apparel that blends comfort with modern styling during pregnancy. Increasing workforce participation among pregnant women, along with a strong desire to maintain personal fashion identity, is supporting steady demand across regions. Expectant mothers are actively seeking garments that adapt to changing body shapes while remaining suitable for everyday wear and professional settings. Product categories are evolving to meet diverse lifestyle needs, including options for daily use, workwear, and wellness-related activities. Advancements in textile innovation are enabling brands to deliver flexible, breathable, and supportive fabrics that enhance overall comfort. Additionally, the growing influence of body positivity and evolving perceptions around pregnancy-related fashion are strengthening market momentum. The expansion of digital retail platforms and organized offline channels is further improving product accessibility. A wide assortment of maternity clothing options, including tops, bottoms, sleepwear, and intimates, continues to support consistent consumer engagement and sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $15.6 Billion |

| CAGR | 4.2% |

The maternity tops segment generated USD 3.16 billion in 2025 and is anticipated to grow at a CAGR of 4.6% through 2035. This segment maintains a leading position due to its versatility, cost-effectiveness, and frequent replacement cycle. These garments are designed to accommodate physical changes during pregnancy through adaptive features such as stretchable materials and flexible fits. Consumers require multiple wardrobe options for different occasions, which increases repeat purchases. The ability to pair these tops with existing clothing further enhances their practicality. Continuous innovation in design, including varied cuts and styles, supports strong consumer interest and ongoing demand.

The cotton segment accounted for 38.6% share in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Cotton remains the preferred material due to its softness, breathability, and natural composition. It offers comfort for sensitive skin and supports temperature regulation, making it suitable for extended wear. Demand is further supported by growing awareness of fabric safety and increasing interest in natural and organic materials. Blended cotton fabrics also provide elasticity while maintaining comfort, strengthening their adoption across product categories.

United States Maternity Apparel Market reached USD 2.80 billion in 2025 and is projected to grow at a CAGR of 4.8% between 2026 and 2035. Market expansion is supported by strong participation of pregnant women in the workforce, evolving fashion preferences, and a well-established retail ecosystem. Demand for functional yet stylish apparel continues to rise, particularly in workwear and athleisure segments. Consumers are increasingly seeking products that combine comfort with contemporary design. The presence of advanced retail networks, along with expanding e-commerce platforms, is enhancing product availability. Manufacturers are focusing on improved fit, inclusive sizing, and fabric innovation to meet evolving consumer expectations.

Key companies operating in the Global Maternity Apparel Market include Adidas AG, ASOS Maternity, Cake Maternity, Gap Inc, H&M, Hatch Collection LLC, Inditex (Zara), Ingrid & Isabel, LLC, Isabella Oliver Limited, JoJo Maman Bebe, Maternal America, Inc., Nike, Inc., Old Navy (Gap Inc), PinkBlush Maternity, and Seraphine. Companies in the maternity apparel market are strengthening their market position through product innovation, digital expansion, and brand differentiation strategies. Many manufacturers are investing in advanced fabric technologies that enhance stretchability, breathability, and comfort while maintaining style. Businesses are expanding their online presence through direct-to-consumer platforms and partnerships with e-commerce retailers to improve reach and customer engagement. Brands are also focusing on inclusive sizing and versatile designs that cater to diverse body types and lifestyle needs. Collaborations with influencers and targeted marketing campaigns are increasing brand visibility. Additionally, companies are introducing sustainable materials and eco-friendly production methods to align with evolving consumer preferences and regulatory expectations, reinforcing long-term competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Material

- 2.2.4 Price Range

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing workforce participation of pregnant women

- 3.2.1.2 Rising awareness of comfort and wellness during pregnancy

- 3.2.1.3 Expansion of e-commerce and online maternity retail

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Short product usage period and limited wardrobe investment

- 3.2.2.2 Competition from regular clothing with stretch features

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for sustainable and organic maternity fabrics

- 3.2.3.2 Expansion of plus-size and inclusive maternity fashion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.10.3 HS Code Classification & Trade Flow Analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Maternity Tops

- 5.1.1 T-shirts

- 5.1.2 Blouses

- 5.1.3 Others (Tunics, etc)

- 5.2 Maternity Bottoms

- 5.2.1 Pants

- 5.2.2 Leggings

- 5.2.3 Skirts

- 5.2.4 Shorts

- 5.3 Maternity Outerwear

- 5.3.1 Jackets

- 5.3.2 Coats

- 5.3.3 Others (Sweaters, etc)

- 5.4 Maternity Intimates

- 5.4.1 Nursing bras

- 5.4.2 Lingerie

- 5.4.3 Others (Camisoles, etc)

- 5.5 Maternity sleepwear

- 5.5.1 Nightgowns

- 5.5.2 Sleep Shirts

- 5.5.3 Lounge Pants

- 5.5.4 Others (Pajama Sets, robes, etc)

Chapter 6 Estimates & Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Cotton

- 6.2 Polyester

- 6.3 Spandex

- 6.4 Modal

- 6.5 Others

Chapter 7 Estimates & Forecast, By Price range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Low (Upto $50)

- 7.2 Medium ($50 - $100)

- 7.3 High (Above $100)

Chapter 8 Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Online

- 8.1.1 E-Commerce

- 8.1.2 Company Website

- 8.2 Offline

- 8.2.1 Wholesales/Distributors

- 8.2.2 Hypermarkets/Supermarkets

- 8.2.3 Specialty Stores

- 8.2.4 Multi-Brand Stores

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Adidas AG

- 10.2 ASOS Maternity

- 10.3 Cake Maternity

- 10.4 Gap Inc

- 10.5 H&M

- 10.6 Hatch Collection LLC

- 10.7 Inditex (Zara)

- 10.8 Ingrid & Isabel, LLC

- 10.9 Isabella Oliver Limited

- 10.10 JoJo Maman Bebe

- 10.11 Maternal America, Inc.

- 10.12 Nike, Inc.

- 10.13 Old Navy (Gap Inc)

- 10.14 PinkBlush Maternity

- 10.15 Seraphine