|

市場調查報告書

商品編碼

2019162

寵物癌症治療市場商機、成長要素、產業趨勢分析及2026-2035年預測。Pet Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

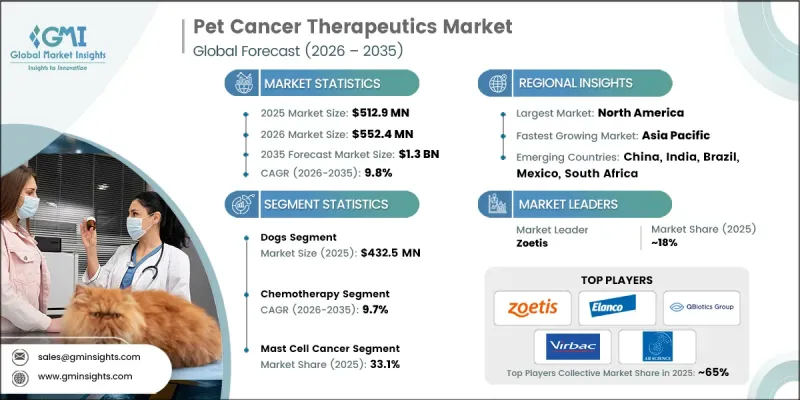

全球寵物癌症治療市場預計到 2025 年將達到 5.129 億美元,並以 9.8% 的複合年成長率成長,到 2035 年將達到 13 億美元。

寵物「擬人化」趨勢的興起推動了市場的快速擴張。隨著飼主越來越將寵物視為家庭成員,對先進醫療保健解決方案的投資也不斷增加。診斷技術的進步、標靶治療和免疫療法的出現,擴大了有效癌症治療的覆蓋範圍。此外,老年寵物癌症發生率的上升進一步刺激了對獸醫腫瘤解決方案的需求。隨著消費者越來越重視高品質的照護和延長生命的治療,從精準診斷到微創治療等獸醫創新在塑造市場成長方面發揮核心作用。先進治療方法的普及、寵物數量的成長以及飼主意識的提高,正在推動全球先進腫瘤治療的普及。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 5.129億美元 |

| 預測金額 | 13億美元 |

| 複合年成長率 | 9.8% |

獸醫癌症治療涵蓋一系列旨在診斷、管理和治療伴侶動物癌症的治療方法。這些治療方法包括化療、免疫療法、標靶治療和聯合治療,其目標是縮小腫瘤、控制症狀並改善寵物的整體健康。獸醫腫瘤學的進步,例如精準醫療、基因組診斷和免疫療法,使得更有效、更微創的治療方法成為可能。這些創新提高了癌症寵物的生存率和生活品質,從而顯著提升了對先進治療方法的需求。由於這些治療方法具有更高的標靶療效和安全性,獸醫擴大採用它們,這也推動了市場的持續擴張。

預計到2025年,犬類市場規模將達到4.325億美元。由於犬類癌症發生率高於其他寵物,因此佔據了最大的市場。淋巴瘤、骨癌和乳房腫瘤等疾病在犬類中較為常見,推動了對專業治療的需求。飼主對犬類癌症的認知不斷提高,以及有效治療方法方案的日益增多,進一步鞏固了犬類在寵物癌症治療市場的主導地位。

預計到2035年,注射劑市場規模將達到8.354億美元。注射劑之所以備受青睞,是因為它們可以將治療藥物直接輸送到血液或腫瘤部位,確保快速吸收和標靶作用。化療藥物、免疫療法和其他注射劑因其能夠實現精準給藥並最大限度地減少副作用,在治療寵物多種癌症方面療效顯著。注射劑給藥系統的持續創新預計將維持該細分市場的強勁需求。

預計到2025年,北美獸醫癌症治療市佔率將達到78.4%。該地區的主導地位得益於寵物擁有率高、先進治療方法的廣泛應用,以及基因組診斷、人工智慧細胞學和成像系統的積極推廣,這些技術能夠實現早期檢測和個人化治療方案的發展。犬貓癌症的高發病率、獸醫保健的高支出以及人們對早期療育和高品質治療方法日益成長的興趣,正在推動北美市場的強勁成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 寵物人性化的進展

- 寵物癌症發生率上升

- 獸醫腫瘤診斷和治療進展

- 意識提高和診斷能力增強

- 產業潛在風險與挑戰

- 高昂的醫療費用

- 副作用和動物耐受性

- 市場機遇

- 為寵物開發個人化癌症疫苗

- 人工智慧驅動的診斷和治療平台的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術(基於初步調查)

- 管道分析(基於初步調查)

- 寵物照護產業的投資和資金籌措趨勢(基於初步調查)

- 各國寵物數量

- 寵物保險的承保範圍和福利狀況(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 未來市場趨勢(基於初步研究)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 狗

- 貓

- 其他物種

第6章 市場估計與預測:依治療方法,2022-2035年

- 化療

- 免疫療法

- 標靶治療

- 聯合治療

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

第8章 市場估計與預測:依癌症類型分類,2022-2035年

- 淋巴瘤

- 肥大細胞癌

- 惡性黑色素瘤

- 乳癌和鱗狀細胞癌

- 其他癌症

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AB Science

- Akston Biosciences

- Boehringer Ingelheim

- CureLab Oncology

- Dechra Pharmaceuticals

- Elanco Animal Health

- ELIAS Animal Health

- Immuvera

- Karyopharm Therapeutic

- NovaVive

- Qbiotics

- VetDC

- Vibrac

- Vivesto

- Zoetis

The Global Pet Cancer Therapeutics Market was valued at USD 512.9 million in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 1.3 billion by 2035.

The market's rapid expansion is driven by the growing trend of pet humanization, with owners increasingly treating pets as family members and investing in advanced healthcare solutions. Improved diagnostic technologies, targeted therapies, and immunotherapies have enhanced access to effective cancer care. Additionally, an aging pet population has led to higher cancer prevalence, further stimulating demand for veterinary oncology solutions. As consumers increasingly prioritize quality care and life-extending treatments, innovations in veterinary medicine, ranging from precision diagnostics to minimally invasive therapies, are playing a central role in shaping market growth. The convergence of advanced therapeutics, increased pet ownership, and rising awareness among pet owners is driving the adoption of sophisticated oncology treatments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $512.9 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 9.8% |

Pet cancer therapeutics encompass a broad range of treatments aimed at diagnosing, managing, and treating cancers in companion animals. These therapies include chemotherapy, immunotherapies, targeted therapies, and combination regimens designed to reduce tumor size, manage symptoms, and improve overall pet health. Advances in veterinary oncology, such as precision medicine, genomic diagnostics, and immunotherapy, are enabling more effective and less invasive treatments. These innovations are improving survival rates and quality of life for pets diagnosed with cancer, creating substantial demand for advanced therapeutics. Veterinary practitioners are increasingly adopting these therapies due to their targeted effects and improved safety profiles, which drive the market's continuous expansion.

The dogs segment reached USD 432.5 million in 2025. Dogs account for the largest share because cancer incidence is higher in this species compared to other pets. Conditions such as lymphoma, osteosarcoma, and mammary tumors are commonly diagnosed in dogs, driving demand for specialized therapeutics. Increased owner awareness about canine cancer and the availability of effective treatment options further support the dominance of the dog segment in the pet cancer therapeutics market.

The injectable therapies segment is projected to reach USD 835.4 million by 2035. Injectables are favored due to their ability to deliver treatment directly into the bloodstream or tumor site, ensuring rapid absorption and targeted action. Chemotherapy agents, immunotherapies, and other injectable formulations offer precise dosing and enhanced control over side effects, making them highly effective for treating various cancers in pets. Continuous innovations in injectable delivery systems are expected to sustain strong market demand for this segment.

North America Pet Cancer Therapeutics Market held a 78.4% share in 2025. The region's leadership is fueled by high pet ownership, widespread use of advanced therapies, and strong adoption of genomic diagnostics, AI-enabled cytology, and imaging systems that enable early detection and personalized treatment planning. The prevalence of cancer in dogs and cats, high veterinary healthcare spending, and growing emphasis on early-stage interventions and premium therapeutics are driving robust market growth in North America.

Key players in the Global Pet Cancer Therapeutics Market include Zoetis, Elanco Animal Health, Virbac, Dechra Pharmaceuticals, AB Science, NovaVive, Karyopharm Therapeutics, Akston Biosciences, CureLab Oncology, VetDC, Boehringer Ingelheim, Vivesto, ELIAS Animal Health, Qbiotics, and Immuvera. Companies in the Global Pet Cancer Therapeutics Market are pursuing several strategies to strengthen their market position. They are investing heavily in R&D to develop innovative targeted and immunotherapy treatments. Strategic partnerships with veterinary clinics, research institutions, and distribution networks are expanding market access. Product pipelines are being diversified to include injectable, oral, and combination therapies. Geographic expansion into emerging markets and the adoption of digital veterinary tools enhance customer reach. Companies emphasize awareness campaigns, clinical education, and after-sales support programs to build trust with pet owners and veterinarians, solidifying brand loyalty and sustaining long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Species trends

- 2.2.3 Therapy trends

- 2.2.4 Route of administration trends

- 2.2.5 Cancer type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet humanization

- 3.2.1.2 Rising cancer incidence in pets

- 3.2.1.3 Advancements in veterinary oncology diagnosis and treatment

- 3.2.1.4 Growing awareness and diagnostic capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Side effects and animal tolerance

- 3.2.3 Market opportunities

- 3.2.3.1 Development of personalized cancer vaccines for pets

- 3.2.3.2 Expansion of AI-powered diagnostic and treatment platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by primary research)

- 3.6 Pipeline analysis (Driven by primary research)

- 3.7 Investment and funding landscape in pet care (Driven by primary research)

- 3.8 Pet population, by country

- 3.9 Pet insurance coverage and reimbursement landscape (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market (Driven by primary research)

- 3.11 Future market trends (Driven by primary research)

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Species, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other species

Chapter 6 Market Estimates and Forecast, By Therapy, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Combination therapy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Cancer Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Lymphoma

- 8.3 Mast cell cancer

- 8.4 Melanoma

- 8.5 Mammary and squamous cell cancer

- 8.6 Other cancer types

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AB Science

- 10.2 Akston Biosciences

- 10.3 Boehringer Ingelheim

- 10.4 CureLab Oncology

- 10.5 Dechra Pharmaceuticals

- 10.6 Elanco Animal Health

- 10.7 ELIAS Animal Health

- 10.8 Immuvera

- 10.9 Karyopharm Therapeutic

- 10.10 NovaVive

- 10.11 Qbiotics

- 10.12 VetDC

- 10.13 Vibrac

- 10.14 Vivesto

- 10.15 Zoetis