|

市場調查報告書

商品編碼

2019150

藥品穩定性及儲存服務市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Pharmaceutical Stability and Storage Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

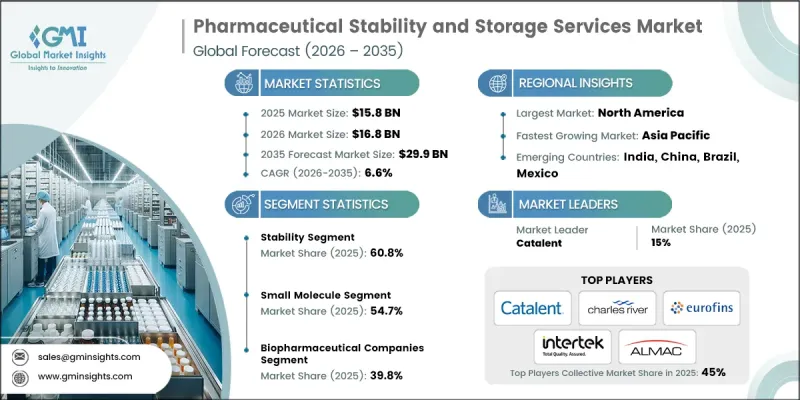

2025 年全球藥品穩定性和儲存服務市場價值為 158 億美元,預計到 2035 年將以 6.6% 的複合年成長率成長至 299 億美元。

受監管合規性日益重視、醫藥研發投入不斷增加以及全球醫藥供應鏈擴張的推動,醫藥穩定性及儲存服務業正經歷穩定成長。嚴格的監管要求促使企業實施先進的穩定性測試和受控儲存方案,以確保產品在整個生命週期內的安全性、品質和有效性。監管機構對穩定性數據和儲存條件製定了嚴格的指導方針,從而推動了整個醫藥行業對專業服務的需求。同時,現代藥物製劑日益複雜以及醫藥分銷網路的全球化進一步增強了對先進儲存基礎設施和測試能力的依賴。這些服務在受控環境條件(包括溫度、濕度和光照)下維持產品完整性方面發揮著至關重要的作用,同時也有助於符合國際品質標準。隨著醫藥創新加速發展,全球市場對可靠的穩定性及儲存解決方案的需求持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 158億美元 |

| 預測金額 | 299億美元 |

| 複合年成長率 | 6.6% |

藥品穩定性和儲存服務涉及一系列專門的流程,旨在維持藥品、生物製藥和醫療產品在其整個保存期限內的品質、安全性和有效性。這些服務包括受控的儲存環境和系統化的測試程序,以評估產品隨時間推移對環境條件的反應,從而確保產品性能穩定並符合法規要求。

到2025年,穩定性測試領域將佔據60.8%的市場。穩定性測試在檢驗藥品在其整個生命週期內的安全性和有效性方面發揮著至關重要的作用。原料藥和成品的監管要求日益嚴格,推動了對這類服務的需求。測試程序會評估溫度、濕度和光照等環境因素的影響,以確保符合既定的品質標準。隨著藥品的複雜性不斷增加,對先進測試技術的需求也日益成長,以確定合適的保存期限和儲存條件。

預計到2025年,生物製藥公司將佔據39.8%的市場。這些公司處於藥物研發、生產和商業化流程的核心,需要進行廣泛的穩定性測試和受控儲存,以滿足監管要求。複雜治療方法的不斷發展推動了對精準客製化儲存解決方案的需求成長。生物製藥公司管理著多元化的產品系列,這些產品需要進行廣泛的穩定性測試和特殊的儲存條件,這進一步促進了該領域的成長。

預計到2025年,北美藥品穩定性和儲存服務市場規模將達到60億美元,2035年將達到108億美元。這一成長得益於其強大的製藥生產生態系統、成熟的外包模式以及對經過驗證的檢驗和儲存服務的高度依賴。持續的藥物研發活動和嚴格的監管要求正在推動對先進穩定性解決方案的需求。成熟的醫療保健基礎設施和完善的監管體系進一步鞏固了該地區在全球市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 人們越來越關注監管合規性

- 加大對藥品研發的投入。

- 用於提高藥品穩定性和儲存性能的技術創新

- 全球供應鏈的擴張

- 產業潛在風險與挑戰

- 專業儲存解決方案高成本

- 對運輸和物流的擔憂

- 市場機遇

- 對端到端穩定性測試和儲存生態系統外包的需求日益成長。

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 技術格局

- 目前技術

- 符合ICH標準的穩定性測試實驗室

- 溫控儲藏室

- 新興技術

- 物聯網賦能的穩定性測試實驗室

- 先進的低溫和液態氮(LN2) 儲存解決方案

- 目前技術

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依服務類型分類,2022-2035年

- 穩定

- 原料藥

- 穩定性指數方法的驗證

- 加速穩定性測試

- 光照穩定性測試

- 其他穩定性測試方法

- 貯存

- 寒冷的

- 冰凍

- 冷藏

- 管理

- 極低溫度

- 無需冷藏

第6章 市場估計與預測:依分子類型分類,2022-2035年

- 低分子

- 市售產品

- 研究產品

- 聚合物

- 市售產品

- 研究產品

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 生物製藥公司

- 契約製造組織

- 受託研究機構

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Alcami Corporation

- Almac Group

- Auriga Research

- Catalent

- Charles River Laboratories

- Element Materials Technology

- Eurofins Scientific

- Intertek Group

- Lucideon

- PD Partners

- Precision Stability Storage

- Q Laboratories

- Q1 Scientific

- Reading Scientific Services

- Roylance Stability Storage

The Global Pharmaceutical Stability and Storage Services Market was valued at USD 15.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 29.9 billion by 2035.

The pharmaceutical stability and storage services industry is experiencing steady growth, supported by increasing emphasis on regulatory compliance, rising investments in drug research and development, and the expansion of global pharmaceutical supply chains. Stringent regulatory requirements are compelling companies to adopt advanced stability testing and controlled storage solutions to ensure product safety, quality, and efficacy throughout the product lifecycle. Regulatory authorities enforce strict guidelines for stability data and storage conditions, which is driving the need for specialized services across the pharmaceutical sector. At the same time, the growing complexity of modern drug formulations and the globalization of drug distribution networks are further increasing reliance on advanced storage infrastructure and testing capabilities. These services play a critical role in maintaining product integrity under controlled environmental conditions, including temperature, humidity, and light exposure, while also supporting compliance with international quality standards. As pharmaceutical innovation accelerates, the demand for reliable stability and storage solutions continues to strengthen across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.8 Billion |

| Forecast Value | $29.9 Billion |

| CAGR | 6.6% |

Pharmaceutical stability and storage services involve specialized processes designed to maintain the quality, safety, and effectiveness of drugs, biologics, and medical products throughout their shelf life. These services include controlled storage environments and systematic testing procedures to evaluate how products respond to environmental conditions over time, ensuring consistent performance and regulatory compliance.

The stability segment held a 60.8% share in 2025. Stability testing plays a critical role in validating the safety and performance of pharmaceutical products across their lifecycle. Increasing regulatory requirements for both drug substances and finished formulations are driving demand for these services. Testing procedures evaluate the impact of environmental factors such as temperature, humidity, and light, ensuring adherence to established quality standards. The growing complexity of pharmaceutical products is also increasing the need for advanced testing approaches that determine appropriate shelf life and storage parameters.

The biopharmaceutical companies segment held a 39.8% share in 2025. These organizations are central to drug development, manufacturing, and commercialization processes, requiring extensive stability testing and controlled storage to meet regulatory expectations. As the development of complex therapies continues to expand, demand for precise and customized storage solutions is increasing. Biopharmaceutical companies manage diverse product portfolios, which require a wide range of stability studies and specialized storage conditions, further supporting segment growth.

North America Pharmaceutical Stability and Storage Services Market garnered USD 6 billion in 2025 and is projected to reach USD 10.8 billion by 2035. Growth in the region is supported by a strong pharmaceutical manufacturing ecosystem, a well-established outsourcing framework, and high reliance on validated testing and storage services. Continuous drug development activity and strict regulatory requirements are reinforcing the demand for advanced stability solutions. A mature healthcare infrastructure and comprehensive regulatory systems further strengthen the region's leadership position in the global market.

Key companies operating in the Global Pharmaceutical Stability and Storage Services Market include Eurofins Scientific, Catalent, Charles River Laboratories, Almac Group, Intertek Group, Alcami Corporation, Q1 Scientific, Precision Stability Storage, Q Laboratories, Auriga Research, Element Materials Technology, Reading Scientific Services, Roylance Stability Storage, PD Partners, and Lucideon. Companies in the Pharmaceutical Stability and Storage Services Market are enhancing their competitive position through continuous investment in advanced infrastructure and technology. They are focusing on expanding temperature-controlled storage capabilities and improving testing accuracy to meet evolving regulatory standards. Strategic partnerships with pharmaceutical and biotechnology firms are helping companies secure long-term contracts and broaden service offerings. Firms are also adopting digital monitoring systems and data analytics to improve efficiency and compliance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.2.1 Service type trends

- 2.2.2 Molecule type trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing focus on regulatory compliance

- 3.2.1.2 Increasing investments in drug development and research

- 3.2.1.3 Technological innovations enhancing pharmaceutical stability and storage

- 3.2.1.4 Expansion in global supply chains

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with specialized storage solutions

- 3.2.2.2 Concerns related to transportation and logistics

- 3.2.3 Market opportunity

- 3.2.3.1 Rising demand for end-to-end outsourced stability and storage ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological landscape

- 3.5.1 Current technology

- 3.5.1.1 ICH-compliant stability chambers

- 3.5.1.2 Temperature-controlled storage chambers

- 3.5.2 Emerging technology

- 3.5.2.1 IoT-enabled stability chamber

- 3.5.2.2 Advanced cryogenic and liquid nitrogen (LN2) storage solutions

- 3.5.1 Current technology

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Stability

- 5.2.1 Drug substance

- 5.2.2 Stability indicating method validation

- 5.2.3 Accelerated stability testing

- 5.2.4 Photostability testing

- 5.2.5 Other stability testing methods

- 5.3 Storage

- 5.3.1 Cold

- 5.3.2 Frozen

- 5.3.3 Refrigerated

- 5.3.4 Controlled

- 5.3.5 Cryogenic

- 5.4 Non-cold

Chapter 6 Market Estimates and Forecast, By Molecule Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Small molecule

- 6.2.1 Commercial products

- 6.2.2 Research products

- 6.3 Large molecule

- 6.3.1 Commercial products

- 6.3.2 Research products

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Biopharmaceutical companies

- 7.3 Contract manufacturing organization

- 7.4 Contract research organization

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alcami Corporation

- 9.2 Almac Group

- 9.3 Auriga Research

- 9.4 Catalent

- 9.5 Charles River Laboratories

- 9.6 Element Materials Technology

- 9.7 Eurofins Scientific

- 9.8 Intertek Group

- 9.9 Lucideon

- 9.10 PD Partners

- 9.11 Precision Stability Storage

- 9.12 Q Laboratories

- 9.13 Q1 Scientific

- 9.14 Reading Scientific Services

- 9.15 Roylance Stability Storage

媒體與娛樂儲存市場報告:按儲存解決方案、部署類型、錄製媒體、最終用戶和地區分類(2026-2034 年)

媒體與娛樂儲存市場報告:按儲存解決方案、部署類型、錄製媒體、最終用戶和地區分類(2026-2034 年) 2026年全球儲存服務市場報告

2026年全球儲存服務市場報告 區塊儲存市場:2026 年至 2032 年全球市場預測,按組件、部署模式、儲存媒體、通訊協定、組織規模、應用和產業分類。2026年全球外部儲存設備市場報告2026年全球藥品穩定性和儲存服務市場報告GMP倉儲服務市場按倉儲溫度、產品類型、服務地點、最終用戶和應用進行分類-全球預測(2026-2032年)脂肪幹細胞儲存服務市場:按服務類型、儲存期限、交付方式、定價模式、應用和最終用戶分類的全球預測(2026-2032年)

區塊儲存市場:2026 年至 2032 年全球市場預測,按組件、部署模式、儲存媒體、通訊協定、組織規模、應用和產業分類。2026年全球外部儲存設備市場報告2026年全球藥品穩定性和儲存服務市場報告GMP倉儲服務市場按倉儲溫度、產品類型、服務地點、最終用戶和應用進行分類-全球預測(2026-2032年)脂肪幹細胞儲存服務市場:按服務類型、儲存期限、交付方式、定價模式、應用和最終用戶分類的全球預測(2026-2032年) 全球媒體與娛樂儲存市場全球藥品穩定性與儲存服務市場

全球媒體與娛樂儲存市場全球藥品穩定性與儲存服務市場 北美和歐洲藥物穩定性服務市場規模、佔有率和趨勢分析報告:按服務、分子、國家和細分市場預測,2025 年至 2030 年

北美和歐洲藥物穩定性服務市場規模、佔有率和趨勢分析報告:按服務、分子、國家和細分市場預測,2025 年至 2030 年