|

市場調查報告書

商品編碼

2019141

乳製品包裝器材市場機會、成長要素、產業趨勢分析及2026-2035年預測。Dairy Packaging Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

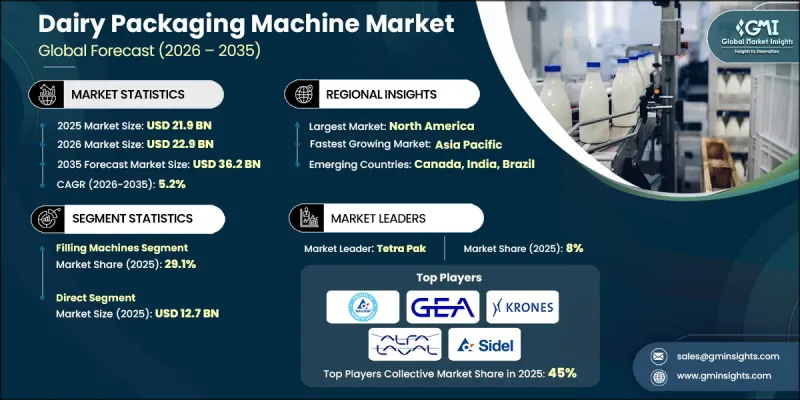

預計到 2025 年,全球乳製品包裝器材市場價值將達到 219 億美元,並預計以 5.2% 的複合年成長率成長,到 2035 年達到 362 億美元。

乳製品包裝器材的快速普及得益於自動化、智慧製造系統和食品安全技術的持續創新。製造商正加速從人工流程向全自動和數位整合的包裝解決方案轉型,這體現了業界對效率、精度和可追溯性的重視。硬體和軟體供應商之間的整合進一步推動了整合加工、品質檢測和生產監控的承包解決方案的普及。現代乳製品包裝器材設計柔軟性,可實現無縫規格切換、多產品處理並減少停機時間。人工智慧驅動的品管、預測性維護、機器視覺系統和物聯網驅動的資產管理等最尖端科技,在確保符合嚴格的安全和衛生標準的同時,提升了營運績效。數位雙胞胎技術的引入實現了即時監控、運行模擬和流程最佳化,進一步推動了市場的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 219億美元 |

| 預測金額 | 362億美元 |

| 複合年成長率 | 5.2% |

到2025年,灌裝機市佔率將達到29.1%,市場規模達64億美元。灌裝機憑藉其高速性能、體積和重量精度以及與多種乳製品(包括牛奶、優格和奶油)的兼容性,在初級包裝中發揮著至關重要的作用。灌裝和封口流程的自動化實現了集中式品管,操作人員可以透過數位化控制面板即時監控多條生產線並進行調整。這減少了產品浪費,縮短了換線時間,並確保了產品品質的穩定性,而這正是推動市場成長的主要動力。人工智慧和視覺系統的整合提高了精度,能夠檢測缺陷並確保符合監管標準,從而提高營運效率並最大限度地減少生產損失。

預計到2035年,直銷業務將以5.3%的複合年成長率成長。該業務板塊仍然是大規模工業加工企業和跨國乳製品公司的最佳選擇。這一成長主要得益於市場對綜合承包解決方案、與原始設備製造商 (OEM) 直接技術諮詢、專屬售後服務以及操作人員培訓計劃的需求不斷成長。製造商的直接參與使其能夠提供客製化的安裝服務、長期維護合約和持續的系統升級,從而確保運作可靠性並減少停機時間。提供現場支援和客製化技術解決方案的公司持續贏得追求最高效率和系統柔軟性的工業和商業乳製品製造商的信賴。

到2025年,美國乳製品包裝器材市佔率將達到75.3%。這一市場主導地位得益於大規模乳製品合作社的集中化、嚴格的食品安全和衛生法規,以及對長保存期限包裝解決方案日益成長的需求。在該地區,用於牛奶、起司、優格和其他乳製品的自動化、可追溯生產線和先進包裝系統的應用正在加速。對永續性和減少廢棄物的日益關注,以及對智慧製造技術的投資,進一步推動了市場成長。無菌填充系統、多規格生產線柔軟性和人工智慧監控等先進包裝解決方案正被擴大採用,以滿足消費者對新鮮度、品質和安全日益成長的期望。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 無菌包裝及長期儲存

- 人手不足和回流

- 智慧包裝與物聯網的融合

- 產業潛在風險與挑戰

- 高額初始資本支出(CAPEX)

- 加強永續性合規性

- 機會

- 模組化「微型日間」單元的成長

- 智慧型「自清潔」系統的發展

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易走廊及關稅影響(基於初步調查)

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的列印管理和預測性維護

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 基礎設施和實施情況(基於初步調查)

- 按地區和購買者群體分類的採用率和滲透率(基於初步調查)

- 基礎設施投資的可擴展性限制和趨勢(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 灌裝機

- 成型填色封口 (FFS) 機

- 碼高機

- 包裝機

- 裝盒機

- 貼標機

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 靈活的

- 難的

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 自動的

- 半自動

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 牛奶

- 生乳製品

- 奶油和酪乳

- 奶粉

- 其他

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Barry-Wehmiller

- Carpigiani Group

- Elopak

- GEA Group

- Greatview Aseptic Packaging

- IMA Group

- Krones AG

- Scherjon Dairy Equipment

- Scholle IPN(SIG)

- Sidel

- SIG Combibloc

- SPX Flow(ITT)

- Syntegon

- Technogel SpA

- Tetra Pak

The Global Dairy Packaging Machine Market was valued at USD 21.9 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 36.2 billion by 2035.

The rapid adoption of dairy packaging machines is being driven by ongoing innovations in automation, smart manufacturing systems, and food safety technologies. Manufacturers are increasingly shifting from manual to fully automated and digitally integrated packaging solutions, reflecting the industry's focus on efficiency, precision, and traceability. Consolidation between hardware and software providers has further reinforced the adoption of turnkey solutions that integrate processing, quality inspection, and production monitoring. Modern dairy packaging machines are designed for high flexibility, allowing seamless format changes, multi-product handling, and reduced downtime. Cutting-edge technologies, including AI-enabled quality control, predictive maintenance, machine vision systems, and IoT-driven asset management, are enhancing operational performance while ensuring compliance with stringent safety and hygiene standards. The adoption of digital twin technologies is enabling real-time monitoring, operational simulation, and process optimization, further supporting sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.9 Billion |

| Forecast Value | $36.2 Billion |

| CAGR | 5.2% |

In 2025, the filling machines segment held 29.1% share, valued at USD 6.4 billion. Filling machines are critical in primary packaging due to their high-speed performance, volumetric and gravimetric accuracy, and compatibility with a variety of dairy products, including milk, yogurt, and cream. Automation of filling and sealing operations allows for centralized quality oversight, enabling operators to monitor multiple production lines through digital dashboards and make real-time adjustments. This reduces product waste, shortens changeover times, and ensures consistent output quality, which is a key driver of growth. The integration of AI and vision systems enhances precision, enabling defect detection and adherence to regulatory standards, which strengthens operational efficiency and minimizes production losses.

The direct sales segment is projected to grow at a CAGR of 5.3% through 2035. This segment remains the preferred choice for large-scale industrial processors and multinational dairy corporations. Growth is supported by the rising demand for comprehensive turnkey solutions, direct technical consultations with OEMs, dedicated after-sales support, and operator training programs. Direct engagement allows manufacturers to offer tailored installation services, long-term maintenance agreements, and ongoing system upgrades, which ensure operational reliability and reduce downtime. Companies providing on-site support and customized technical solutions continue to gain the trust of industrial and commercial dairy producers seeking maximum efficiency and system flexibility.

United States Dairy Packaging Machine Market held a 75.3% share in 2025. Market dominance is fueled by a high concentration of large dairy cooperatives, stringent food safety and hygiene regulations, and increasing demand for extended shelf-life packaging solutions. The region is witnessing accelerated adoption of automated, traceability-enabled production lines and advanced packaging systems for milk, cheese, yogurt, and other dairy products. Growing emphasis on sustainability and waste reduction, combined with investments in smart manufacturing technologies, further drives market growth. Advanced packaging solutions, including aseptic filling systems, multi-format line flexibility, and AI-driven monitoring, are increasingly deployed to meet evolving consumer expectations for freshness, quality, and safety.

Major companies operating in the Global Dairy Packaging Machine Market include Alfa Laval AB, Barry-Wehmiller, Carpigiani Group, Elopak, GEA Group, Greatview Aseptic Packaging, IMA Group, Krones AG, Scherjon Dairy Equipment, Scholle IPN (SIG), Sidel, SIG Combibloc, SPX Flow (ITT), Syntegon, Technogel S.p.A., and Tetra Pak. These players are driving innovation, expanding their product portfolios, and enhancing global reach to cater to increasing demand for automated, flexible, and smart dairy packaging solutions. Key strategies adopted by companies in the Dairy Packaging Machine Market include continuous investment in research and development to improve automation, digitalization, and AI-driven inspection technologies. Firms are forming strategic alliances with software and IoT providers to deliver integrated turnkey solutions and smart factory capabilities. Expanding after-sales service networks, including on-site maintenance, operator training, and predictive support, strengthens customer trust and operational reliability. Companies are also focusing on multi-format packaging capabilities, energy-efficient designs, and sustainable material usage to appeal to environmentally conscious dairy producers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Packaging Type

- 2.2.4 Operation

- 2.2.5 Application

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aseptic & extended shelf life

- 3.2.1.2 Labor shortages & reshoring

- 3.2.1.3 Smart Packaging & Iot Integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial capex

- 3.2.2.2 Increasing sustainability compliance

- 3.2.3 Opportunities

- 3.2.3.1 Increasing growth of modular "micro-dairy" units

- 3.2.3.2 Growth in smart "self-cleaning" systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Print Management & Predictive Maintenance

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.12.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.12.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Filling Machines

- 5.3 Form-Fill-Seal (FFS) Machines

- 5.4 Palletizing Machines

- 5.5 Wrapping Machines

- 5.6 Cartoning Machines

- 5.7 Labeling Machines

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Flexible

- 6.3 Rigid

Chapter 7 Market Estimates & Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Milk

- 8.3 Fresh Dairy Products

- 8.4 Butter & Buttermilk

- 8.5 Milk Powder

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Barry-Wehmiller

- 11.2 Carpigiani Group

- 11.3 Elopak

- 11.4 GEA Group

- 11.5 Greatview Aseptic Packaging

- 11.6 IMA Group

- 11.7 Krones AG

- 11.8 Scherjon Dairy Equipment

- 11.9 Scholle IPN (SIG)

- 11.10 Sidel

- 11.11 SIG Combibloc

- 11.12 SPX Flow (ITT)

- 11.13 Syntegon

- 11.14 Technogel S.p.A.

- 11.15 Tetra Pak

乳製品包裝市場預測至2034年-按包裝類型、材料、產品類型、包裝形式、封裝方式、最終用戶和地區分類的全球分析

乳製品包裝市場預測至2034年-按包裝類型、材料、產品類型、包裝形式、封裝方式、最終用戶和地區分類的全球分析 乳製品包裝市場規模、佔有率、趨勢和預測:按包裝材料、包裝形式、產品類型、應用和地區分類,2026-2034年

乳製品包裝市場規模、佔有率、趨勢和預測:按包裝材料、包裝形式、產品類型、應用和地區分類,2026-2034年 乳製品包裝市場:2026-2032年全球市場預測(依包裝類型、材料、技術、封裝方法及應用分類)

乳製品包裝市場:2026-2032年全球市場預測(依包裝類型、材料、技術、封裝方法及應用分類) 全球乳製品包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球乳製品包裝市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

全球乳製品包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球乳製品包裝市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034) 乳製品包裝市場規模、佔有率及成長分析(依材料、包裝類型、產品類型及地區)-2025-2032 年產業預測

乳製品包裝市場規模、佔有率及成長分析(依材料、包裝類型、產品類型及地區)-2025-2032 年產業預測 乳製品包裝市場機會、成長動力、產業趨勢分析與預測 2025-2034

乳製品包裝市場機會、成長動力、產業趨勢分析與預測 2025-2034 乳製品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)拉丁美洲乳製品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)美國乳製品包裝:市場佔有率分析、產業趨勢、產業趨勢、成長預測(2025-2030)

乳製品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)拉丁美洲乳製品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)美國乳製品包裝:市場佔有率分析、產業趨勢、產業趨勢、成長預測(2025-2030)