|

市場調查報告書

商品編碼

2019137

汽車顯示器市場機會、成長要素、產業趨勢分析及2026-2035年預測Automotive Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

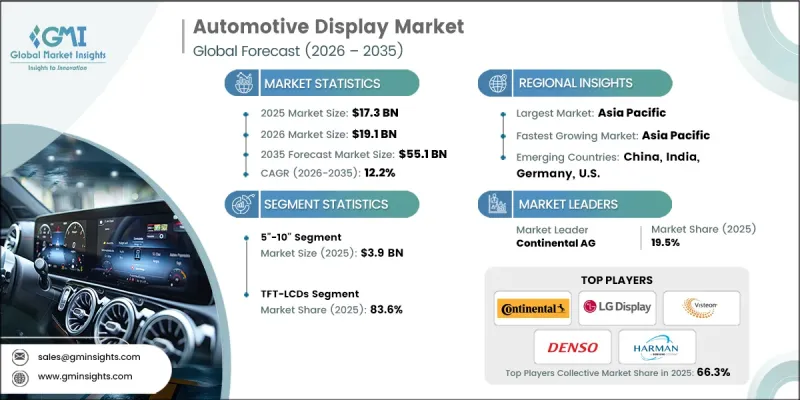

全球汽車顯示器市場預計到 2025 年將達到 173 億美元,預計到 2035 年將達到 551 億美元,年複合成長率為 12.2%。

推動這一市場發展的動力來自全數位化駕駛座的轉變,高解析度儀錶叢集和大型中控台。消費者對車輛資訊娛樂、導航和互聯功能的互動方式提出了更高的要求,促使汽車製造商在車廂內整合多個顯示器。汽車製造商正在整合人工智慧 (AI)、擴增實境(AR)抬頭顯示器和自適應介面,以個性化駕駛體驗並提升安全性。這些智慧顯示器將儀錶板從靜態面板轉變為互動式中心,提供即時導航、ADAS(高級駕駛輔助系統)分析以及基於駕駛行為的預測內容。對 OLED、QLED、曲面螢幕和超寬螢幕等高階顯示器技術的需求在豪華車和高性能車領域尤為顯著。製造商也優先考慮永續性和能源效率,推動材料和顯示面板的創新,以在提供卓越視覺性能的同時降低能耗。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 173億美元 |

| 預測金額 | 551億美元 |

| 複合年成長率 | 12.2% |

預計到2025年,5-10吋顯示器市場規模將達到39億美元。這些尺寸的顯示器在乘用車和商用車領域應用最為廣泛,在儀錶板、資訊娛樂螢幕和中控台等應用中,能夠提供卓越的可視性、功能性和整合性。此細分市場的主導地位反映了原始設備製造商(OEM)的廣泛採用,在汽車應用中實現了清晰度、易用性和成本效益之間的平衡。

預計到2035年,OLED顯示器市場將以15.1%的複合年成長率成長。這項成長主要得益於消費者對高對比、柔軟性及曲面顯示器的需求,以及高階汽車和電動車對OLED面板日益成長的採用率。技術進步使得OLED面板能夠實現節能高效且色彩鮮豔,使其成為數位駕駛座和資訊娛樂系統的理想之選,同時也支援輕量化和軟性儀錶板設計。

預計到2025年,北美汽車顯示器市佔率將達到20.9%。該地區受益於多種數位駕駛座系統、資訊娛樂解決方案以及旨在提升電動車和聯網汽車用戶體驗的先進車載儀錶叢集的日益融合。在該地區擁有強大影響力和技術專長的汽車製造商正在推動更大尺寸、更高解析度顯示器的普及。受消費者對個人化、互動式介面的日益偏好的推動,預計美國和加拿大市場將持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電動汽車產業的崛起

- 將ADAS系統整合到汽車中

- 對聯網汽車的需求日益成長

- 消費者偏好大尺寸顯示器

- 車載資訊娛樂系統需求不斷成長

- 產業潛在風險與挑戰

- 網路攻擊與資料外洩威脅

- 半導體短缺正在影響生產。

- 市場機遇

- OLED和先進顯示器的廣泛應用

- AR/VR與抬頭顯示器的整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢(基於初步調查)

- 歷史價格分析(2023-2026)

- 影響價格趨勢的因素

- 區域價格波動

- 價格預測(2027-2036)

- 定價策略(基於初步研究)

- 新經營模式

- 貿易數據分析(基於初步調查)

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- TFT-LCD

- OLED

第6章 市場估價與預測:依顯示器類型分類,2022-2035年

- 中控台顯示螢幕

- 儀表板顯示

- 數位儀表板

- 駕駛員資訊顯示

- 速率計/轉速表螢幕

- 其他

- 後座娛樂顯示器

- 抬頭顯示器(HUD)

- 其他

第7章 市場估價與預測:依螢幕大小分類,2022-2035年

- 小於5英寸

- 5英寸到10英寸

- 超過10英寸

第8章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- 多用途車輛

- 商用車輛

- 輕型商用車(LCV)

- 重型商用車(HCV)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- 主要企業

- Continental AG

- Denso Corporation

- HARMAN International

- LG DISPLAY CO., LTD.

- Mitsubishi Electric

- Panasonic Automotive Systems

- Robert Bosch GmbH

- Visteon Corporation

- 按地區分類的主要企業

- 北美洲

- ON Semiconductor(onsemi)

- Littelfuse, Inc.

- Powerex, Inc.

- 亞太地區

- Hyundai Mobis

- Nippon Seiki Co., Ltd.

- Pricol Ltd.

- YAZAKI

- SHARP

- 歐洲

- Magneti Marelli

- 北美洲

- 特殊玩家/干擾者

- Blaupunkt

- MTA SpA(Italy)

- New Vision Display(Shenzhen)Co, Ltd.

- Nuline Technologies

The Global Automotive Display Market was valued at USD 17.3 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 55.1 billion by 2035.

The market is driven by the shift toward fully digital cockpits that feature high-resolution instrument clusters and large center stacks. Consumers are increasingly seeking intuitive ways to interact with vehicles for infotainment, navigation, and connectivity, prompting OEMs to install multiple displays across vehicle interiors. Automakers are integrating artificial intelligence, augmented reality (AR) head-up displays, and adaptive interfaces to personalize the driving experience while enhancing safety. These intelligent displays provide real-time navigation, ADAS insights, and predictive content based on driver behavior, transforming dashboards from static panels into interactive hubs. Growing demand for high-end display technologies, including OLED, QLED, curved, and ultra-wide formats, is particularly strong in luxury and performance vehicles. Manufacturers are also emphasizing sustainability and energy efficiency, driving innovation in materials and display panels to reduce power consumption while delivering superior visual performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.3 Billion |

| Forecast Value | $55.1 Billion |

| CAGR | 12.2% |

The 5"-10" display segment reached USD 3.9 billion in 2025. These sizes remain the most widely deployed across passenger and commercial vehicles, offering excellent visibility, functionality, and integration in instrument clusters, infotainment screens, and center dashboards. The segment's dominance reflects widespread OEM adoption, providing a balance of clarity, usability, and cost-effectiveness for in-vehicle applications.

The OLED display segment is expected to grow at a CAGR of 15.1% through 2035. The growth is driven by the increasing incorporation of OLED panels in premium and electric vehicles, as consumers demand high-contrast, flexible, and curved displays. Technological advancements have enabled energy-efficient panels with vibrant colors, making them ideal for digital cockpits and infotainment systems, while also supporting lightweight and flexible dashboard designs.

North America Automotive Display Market accounted for 20.9% share in 2025. The region is benefiting from the integration of multiple digital cockpit systems, infotainment solutions, and advanced vehicle instrument clusters designed to enhance the user experience in electric and connected vehicles. OEMs with strong regional presence and technological expertise are driving the adoption of larger, higher-resolution displays. Increasing consumer preference for personalized, interactive interfaces is expected to sustain growth across the U.S. and Canada.

Key players in the Global Automotive Display Market include Blaupunkt, Continental AG, Denso Corporation, HARMAN International, Hyundai Mobis, LG DISPLAY CO., LTD., Magneti Marelli, Mitsubishi Electric, MTA S.p.A., New Vision Display (Shenzhen) Co., Ltd., Nippon Seiki Co., Ltd., Nuline Technologies, Panasonic Automotive Systems, Pricol Ltd., Robert Bosch GmbH, SHARP, Visteon Corporation, and YAZAKI Corporation. Companies in the automotive display market are strengthening their position through continuous innovation in display technologies, including OLED, QLED, and ultra-wide formats. They are investing in R&D to improve resolution, contrast, energy efficiency, and integration with AR and AI-enabled vehicle systems. Strategic partnerships with OEMs and technology providers allow them to embed displays into connected and electric vehicles while expanding global distribution networks. Businesses are also focusing on customization, offering flexible, modular, and adaptive display solutions tailored to regional consumer preferences. Marketing, after-sales support, and software upgrades further enhance user experience and long-term adoption, enabling these companies to maintain a competitive advantage and capture a larger market share.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Display type trends

- 2.2.3 Screen Size trends

- 2.2.4 Vehicle type trends

- 2.2.5 Technology trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 The rise of electric vehicles industry

- 3.2.1.2 Incorporation of ADAS in automotive

- 3.2.1.3 Growing demand for connected vehicles

- 3.2.1.4 Consumers preference towards larger display

- 3.2.1.5 Rising demand for in-car infotainment systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Threats of cyberattacks and data breaching

- 3.2.2.2 Semiconductor shortage affects production

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of OLED and advanced display adoption

- 3.2.3.2 Integration of AR/VR and heads-up displays

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends (Driven by Primary Research)

- 3.7.1 Historical Price Analysis (2023-2026)

- 3.7.2 Price Trend Drivers

- 3.7.3 Regional Price Variations

- 3.7.4 Price Forecast (2027-2036)

- 3.8 Pricing Strategies (Driven by Primary Research)

- 3.8.1 Emerging Business Models

- 3.9 Trade Data Analysis (Driven by Primary Research)

- 3.9.1 Import/Export Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 TFT-LCDs

- 5.3 OLEDs

Chapter 6 Market Estimates and Forecast, By Display Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Center Stack Displays

- 6.3 Instrument Cluster Displays

- 6.3.1 Digital instrument panels

- 6.3.2 Driver information displays

- 6.3.3 Speedometer/tachometer screens

- 6.3.4 Others

- 6.4 Rear-seat Entertainment Displays

- 6.5 Head-Up Displays (HUD)

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Screen Size, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Less than 5"

- 7.3 5" to 10"

- 7.4 Above 10"

Chapter 8 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Passenger Cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 Utility Vehicle

- 8.3 Commercial Vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Continental AG

- 10.1.2 Denso Corporation

- 10.1.3 HARMAN International

- 10.1.4 LG DISPLAY CO., LTD.

- 10.1.5 Mitsubishi Electric

- 10.1.6 Panasonic Automotive Systems

- 10.1.7 Robert Bosch GmbH

- 10.1.8 Visteon Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 ON Semiconductor (onsemi)

- 10.2.1.2 Littelfuse, Inc.

- 10.2.1.3 Powerex, Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Hyundai Mobis

- 10.2.2.2 Nippon Seiki Co., Ltd.

- 10.2.2.3 Pricol Ltd.

- 10.2.2.4 YAZAKI

- 10.2.2.5 SHARP

- 10.2.3 Europe

- 10.2.3.1 Magneti Marelli

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Blaupunkt

- 10.3.2 MTA S.p.A. (Italy)

- 10.3.3 New Vision Display (Shenzhen) Co, Ltd.

- 10.3.4 Nuline Technologies

中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測

中控台顯示器市場:按技術、車輛類型、顯示器尺寸、解析度、觸控技術、最終用戶和銷售管道分類——2026-2032年全球市場預測 汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道)

汽車顯示器市場預測至2034年-全球分析(按顯示器類型、顯示技術、螢幕大小、驅動系統、觸控技術、應用和地區分類)汽車顯示系統市場:2026-2032年全球市場預測(依顯示類型、顯示技術、介面技術、連接方式、解析度、車輛類型、最終用戶和銷售管道) 全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球汽車顯示系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 汽車顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)汽車顯示面板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)汽車顯示面板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 汽車顯示器、中控台和儀表板市場(2026 年)

汽車顯示器、中控台和儀表板市場(2026 年) 汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年)軟性透明顯示器市場:依技術、外形規格、應用、最終用戶和通路分類-2026-2032年全球市場預測

汽車顯示系統市場規模、佔有率、趨勢和預測:按技術、顯示尺寸、應用、車輛類型、銷售管道和地區分類(2026-2034 年)軟性透明顯示器市場:依技術、外形規格、應用、最終用戶和通路分類-2026-2032年全球市場預測 2026年全球動態著色汽車顯示器市場報告

2026年全球動態著色汽車顯示器市場報告