|

市場調查報告書

商品編碼

2019131

船用引擎市場機會、成長要素、產業趨勢分析及2026-2035年預測Marine Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

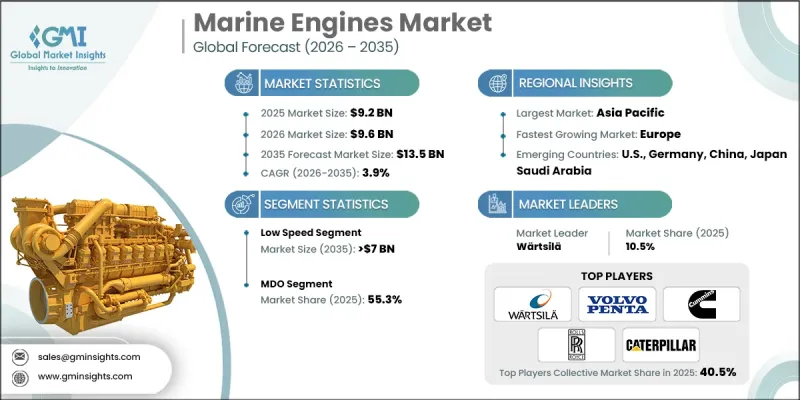

預計到 2025 年,全球船用引擎市場價值將達到 92 億美元,並預計以 3.9% 的複合年成長率成長,到 2035 年達到 135 億美元。

國際航運貿易格局的變化影響著船舶產業的格局,包括物流結構、定價策略和供應鏈調整等,這些因素都會影響各國的競爭力。全球大宗商品貿易的擴張和經濟成長預計將進一步提升對船舶推進系統的需求。船舶引擎是船舶性能的核心,為從小型船舶到大型貨船等各種類型的船舶提供必要的動力和效率。其設計必須確保能夠經得起惡劣海洋環境的考驗,包括海水、振動和極端天氣條件。市場趨勢強調燃油效率、引擎現代化和環境永續解決方案。此外,商業、國防和休閒領域海事活動的擴張正在推動對高性能、高可靠性引擎的需求,而船隊現代化和貿易量的成長則提升了整體市場潛力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 92億美元 |

| 預測金額 | 135億美元 |

| 複合年成長率 | 3.9% |

受港口開發、拖船和小船舶需求成長的推動,預計到2035年,低速船用引擎市場規模將達到70億美元。這些引擎通常是小缸四衝程引擎,因其結構緊湊、性能卓越而備受青睞。其小巧的尺寸使其易於安裝,同時保持了良好的運作效率,因此非常適合渡輪、遊艇和漁船使用。緊湊性和可靠性的結合,使其在各種船舶應用領域中廣泛應用。

預計到2025年,船用柴油(MDO)引擎市佔率將達到55.3%,其高速性能、低噪音水平以及適用於大規模生產等優勢使其發展勢頭強勁。這些引擎由於活動部件少、燃油效率高、排放氣體低,且無需額外潤滑,因此具有成本效益,成為商用和工業船舶的理想選擇。

預計到2025年,美國船用引擎市場規模將達到8.901億美元,主要促進因素包括船舶運行可靠性需求的不斷成長、柴油引擎性能要求的提高以及航運業的擴張。此外,經濟的穩定、對引擎效率日益成長的需求以及對舒適性和高性能船舶解決方案的關注,也進一步加速了該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 價格趨勢分析(單位:美元)

- 按地區

- 依輸出類型

- 波特五力分析

- PESTEL 分析

- 船用引擎成本結構分析

- 新機會和趨勢

- 數位化和物聯網整合

- 未開發市場和應用領域的成長

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依產品分類,2022-2035年

- MDO

- MGO

- LNG

- 混合

- 其他

第6章 市場規模及預測:依產量分類,2022-2035年

- 不足1000馬力

- 1000至5000馬力

- 5,001~10,000 HP

- 10,001 至 20,000 馬力

- 超過20000馬力

第7章 市場規模及預測:依技術分類,2022-2035年

- 慢速

- 中速

- 高速

第8章 市場規模及預測:依促進因素分類,2022-2035年

- 二行程

- 四衝程

第9章 市場規模及預測:依應用領域分類,2022-2035年

- 商船

- 貨櫃船

- 油船

- 散貨船

- 氣體裝運船隻

- RO-RO

- 其他

- 離岸

- 鑽井鑽機和船舶

- 錨作作業船

- 海上支援船

- 浮體式生產設備

- 平台供應船

- 遊輪渡輪

- 郵輪

- 客運渡輪

- 客船和貨船

- 其他

- 海軍

- 其他

第10章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 義大利

- 挪威

- 法國

- 俄羅斯

- 丹麥

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 越南

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 安哥拉

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

第11章:公司簡介

- AB Volvo Penta

- Anglo Belgian Corporation

- Caterpillar

- Cummins

- DAIHATSU INFINEARTH MFG. CO., LTD.

- DEUTZ

- Deere & Company

- Everllence

- Hyundai Heavy Industries

- IHI Corporation

- Mercury Marine

- Mitsubishi Heavy Industries

- Rolls-Royce

- Societe Internationale des Moteurs Baudouin

- Scania

- Shanghai Diesel Engine

- STX Engines

- Wartsila

- Weichai Holding Group Co., Ltd.

- Yamaha Motor Co., Ltd.

- YANMAR HOLDINGS CO., LTD.

- Yuchai International

The Global Marine Engines Market was valued at USD 9.2 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 13.5 billion by 2035.

The industry is being shaped by evolving factors in international maritime trade, including logistics structures, pricing strategies, and supply chain adjustments, which influence the competitiveness of countries. Expanding global merchandise trade and economic growth are expected to further energize demand for marine propulsion systems. Marine engines are central to vessel performance, providing the necessary power and efficiency for various types of boats, from small crafts to large cargo carriers. Their design must ensure durability against harsh marine environments, including saltwater, vibrations, and extreme weather. Market trends emphasize fuel efficiency, engine modernization, and environmentally sustainable solutions. Additionally, the growth of commercial, defense, and leisure maritime activities drives the need for high-performance, reliable engines, while fleet modernization and increasing trade volumes enhance overall market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.2 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 3.9% |

The low-speed marine engines segment is expected to reach USD 7 billion by 2035, driven by seaport development and growing demand for tugboats and smaller vessels. These engines, often four-stroke with fewer cylinders, are valued for their compact design and high performance. Their smaller size allows easier installation while maintaining operational efficiency, making them ideal for ferries, yachts, and fishing boats. The combination of compactness and reliability continues to boost adoption across multiple marine applications.

The MDO (marine diesel oil) engine segment accounted for a 55.3% share in 2025 and is gaining momentum due to its high-speed capabilities, low noise levels, and suitability for large-scale production. These engines are cost-efficient with fewer moving parts, improved fuel efficiency, reduced emissions, and no need for additional lubricants, which makes them an attractive choice for commercial and industrial vessels.

U.S. Marine Engines Market was valued at USD 890.1 million in 2025, driven by the rising demand for operational reliability in vessels, increased diesel engine performance requirements, and the expansion of the maritime transportation industry. Additionally, economic stability, rising demand for engine efficiency, and a focus on comfort and high-performance marine solutions are further accelerating market growth in the region.

Key players in the Global Marine Engines Market include Wartsila, Rolls-Royce, Cummins, Hyundai Heavy Industries, Mitsubishi Heavy Industries, AB Volvo Penta, Caterpillar, Scania, YANMAR HOLDINGS, Mercury Marine, IHI Corporation, Societe Internationale des Moteurs Baudouin, Weichai Holding Group, DAIHATSU INFINEARTH, STX Engines, Deere & Company, Shanghai Diesel Engine, JCW Acoustic Flooring, Anglo Belgian Corporation, Everllence, and Yamaha Motor. Companies in the Marine Engines Market are leveraging several strategies to strengthen their market foothold. These include continuous investment in research and development to enhance fuel efficiency, durability, and environmental compliance of engines. Strategic partnerships with shipbuilders, maritime service providers, and global distributors help expand market reach. Companies are also focusing on product innovation, introducing hybrid and low-emission engines to meet regulatory requirements and attract environmentally conscious buyers. Marketing efforts emphasize reliability, performance, and lifecycle cost efficiency. Geographic expansion into emerging markets, coupled with after-sales services, maintenance programs, and customer training initiatives, further strengthens brand loyalty and market positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Power trends

- 2.1.4 Technology trends

- 2.1.5 Propulsion trends

- 2.1.6 Application trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By power

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of marine engines

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 LNG

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Size and Forecast, By Power, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 < 1,000 HP

- 6.3 1,000 - 5,000 HP

- 6.4 5,001 - 10,000 HP

- 6.5 10,001 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 2 Stroke

- 8.3 4 Stroke

Chapter 9 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 Gas carriers

- 9.2.5 RO-RO

- 9.2.6 Others

- 9.3 Offshore

- 9.3.1 Drilling rigs & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger ferries

- 9.4.3 Passenger/cargo vessels

- 9.4.4 Others

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 Anglo Belgian Corporation

- 11.3 Caterpillar

- 11.4 Cummins

- 11.5 DAIHATSU INFINEARTH MFG. CO., LTD.

- 11.6 DEUTZ

- 11.7 Deere & Company

- 11.8 Everllence

- 11.9 Hyundai Heavy Industries

- 11.10 IHI Corporation

- 11.11 Mercury Marine

- 11.12 Mitsubishi Heavy Industries

- 11.13 Rolls-Royce

- 11.14 Societe Internationale des Moteurs Baudouin

- 11.15 Scania

- 11.16 Shanghai Diesel Engine

- 11.17 STX Engines

- 11.18 Wartsila

- 11.19 Weichai Holding Group Co., Ltd.

- 11.20 Yamaha Motor Co., Ltd.

- 11.21 YANMAR HOLDINGS CO., LTD.

- 11.22 Yuchai International

船用輔助引擎市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料、功率、應用、地區和競爭格局分類,2021-2031年

船用輔助引擎市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料、功率、應用、地區和競爭格局分類,2021-2031年 船用引擎市場:全球市場按產品類型、燃料類型、應用和銷售管道分類的預測——2026-2032年小型船用引擎市場:2026-2032年全球市場預測(按引擎類型、功率範圍、燃料類型、冷卻系統、應用、分銷管道和銷售管道)

船用引擎市場:全球市場按產品類型、燃料類型、應用和銷售管道分類的預測——2026-2032年小型船用引擎市場:2026-2032年全球市場預測(按引擎類型、功率範圍、燃料類型、冷卻系統、應用、分銷管道和銷售管道) 2026年全球小型船舶引擎市場報告2026年全球船用引擎市場報告船用內燃機市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、燃料類型、應用、地區和競爭格局分類,2021-2031年船用引擎市場-全球產業規模、佔有率、趨勢、機會和預測:按衝程、排氣量、燃料類型、船舶類型、地區和競爭格局分類,2021-2031年全球船用氨燃料引擎市場(按引擎類型、功率、推進系統、船舶類型和配銷通路分類)預測(2026-2032年)全球船用雙燃料氨引擎市場(按船舶類型、引擎功率等級、安裝類型、引擎配置、應用和最終用途分類)預測(2026-2032年)

2026年全球小型船舶引擎市場報告2026年全球船用引擎市場報告船用內燃機市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、燃料類型、應用、地區和競爭格局分類,2021-2031年船用引擎市場-全球產業規模、佔有率、趨勢、機會和預測:按衝程、排氣量、燃料類型、船舶類型、地區和競爭格局分類,2021-2031年全球船用氨燃料引擎市場(按引擎類型、功率、推進系統、船舶類型和配銷通路分類)預測(2026-2032年)全球船用雙燃料氨引擎市場(按船舶類型、引擎功率等級、安裝類型、引擎配置、應用和最終用途分類)預測(2026-2032年) 小型船用引擎市場規模、佔有率和成長分析(按引擎類型、安裝位置、排氣量、應用和地區分類)-2026-2033年產業預測

小型船用引擎市場規模、佔有率和成長分析(按引擎類型、安裝位置、排氣量、應用和地區分類)-2026-2033年產業預測