|

市場調查報告書

商品編碼

2019125

攜帶式心臟超音波圖設備市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Handheld Echocardiography Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

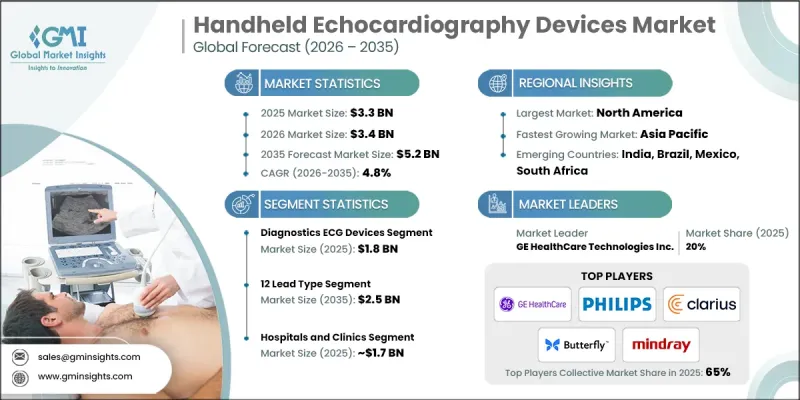

全球攜帶式心臟超音波圖市場預計到 2025 年將達到 33 億美元,預計到 2035 年將以 4.8% 的複合年成長率成長至 52 億美元。

推動這一成長的因素包括:對遠端患者監護需求的不斷成長、超音波心動圖技術的進步、心血管疾病患病率的上升、人口老齡化以及居家醫療的日益普及。攜帶式心臟超音波圖設備已成為現代醫學中不可或缺的工具,可在臨床環境中提供即時心臟影像。它們能夠實現快速篩檢、疾病早期發現、臨床分診以及在醫院、門診部、基層醫療中心、急診和醫療資源匱乏地區進行治療監測。推動這一市場發展的因素包括:影像品質的提升、設備小型化、電池續航時間的延長、無線傳輸以及人工智慧(AI)在影像分析中的應用。這些進步透過提高診斷可靠性、簡化工作流程和改善使用者體驗,促進了攜帶式超音波心動圖設備在臨床和居家照護環境中的更廣泛應用。這些設備高度便攜、輕巧且採用電池供電,使臨床醫生能夠在現場有效地對心臟的結構、功能和血流進行成像。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 33億美元 |

| 預測金額 | 52億美元 |

| 複合年成長率 | 4.8% |

預計到2025年,診斷性心電圖(ECG)設備市場規模將達到18億美元,主要得益於非侵入性、快速且易於使用的心臟影像技術。這些設備減少了對傳統推車式掃描器的依賴,並有助於加速臨床決策。諸如小型化感測器、無線連接和基於應用程式的工作流程等技術進步,提高了設備的易用性,便於整合到分散式醫療環境中,並擴大了其在床邊護理和家庭監測模式中的應用。

預計到2025年,醫院和診所領域的市場規模將達到17億美元。該領域涵蓋公立和私立醫院、心臟護理中心、門診診所和急診科,這些機構均使用攜帶式超音波心動圖進行床邊評估。這些設備使臨床醫生能夠在常規檢查、急診和後續觀察期間快速評估心臟結構和功能,而無需依賴大型固定系統。龐大的患者數量以及對快速診斷和簡化工作流程日益成長的需求,是推動該領域佔據主導地位的主要因素。

預計到2025年,北美攜帶式超音波心臟檢查市場佔有率將達到33.6%。該地區如此高的市場佔有率主要歸功於心血管疾病的高發病率以及醫院、門診和急診醫療機構對快速床邊(POC)心臟評估日益成長的需求。完善的醫療基礎設施、攜帶式成像技術的早期應用以及領先醫療設備製造商的存在,都在加速市場成長。北美的醫療生態系統支援早期診斷、及時介入以及創新型攜帶式心臟超音波圖解決方案的廣泛應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 遠端患者監護的需求日益成長

- 超音波心動圖技術的進步

- 心血管疾病發生率增加

- 人口老化和居家醫療趨勢

- 產業潛在風險與挑戰:

- 監管合規性和標準化

- 與傳統心電圖系統相比,診斷能力有其局限性

- 市場機遇

- 新興市場採用率的擴大

- 擴展即時診斷

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術進步

- 當前技術趨勢

- 新興技術(基於初步調查)

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 診斷性心電圖設備

- 靜態心電圖

- 動態心電圖

- 心電圖監測設備

- 心電圖監測

- 移動式心電遙測(MCT)

- 穿戴式心電圖設備

- 其他心電圖監測設備

第6章 市場估算與預測:依鉛類型分類,2022-2035年

- 單極型

- 3 引腳型

- 6 引腳型

- 12 鉛式

- 其他鉛類型

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院和診所

- 診斷中心

- 門診手術中心

- 居家照護設施

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- AliveCor, Inc.

- Biotronik SE & Co. KG

- Boston Scientific Corporation

- Butterfly Network

- CHISON

- Clarius

- EchoNous Inc.

- Esaote SpA

- Exo Imaging, Inc.

- Fukuda Denshi Co., Ltd.

- GE HealthCare Technologies Inc.

- Hill-Rom Holdings, Inc.

- Koninklijke Philips NV

- Medtronic plc

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

The Global Handheld Echocardiography Devices Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 5.2 billion by 2035.

The growth is driven by the rising demand for remote patient monitoring, advancements in echocardiography technology, an increasing prevalence of cardiovascular diseases, and the expanding aging population, along with growing home healthcare adoption. Handheld echocardiography devices have become essential tools in modern medicine, providing real-time cardiac imaging at the point of care. They enable rapid screening, early disease detection, clinical triage, and treatment monitoring across hospitals, outpatient clinics, primary care centers, emergency departments, and underserved areas. The market is propelled by technological innovations, including enhanced image quality, miniaturized designs, extended battery life, wireless transmission, and integration of artificial intelligence for image interpretation. These advances improve diagnostic confidence, streamline workflows, and enhance user experience, encouraging wider adoption in clinical and home care settings. Portable, lightweight, and battery-operated, these devices allow clinicians to capture cardiac structure, function, and blood flow images efficiently on-site.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 4.8% |

The diagnostics ECG devices segment accounted for USD 1.8 billion in 2025, leading the market due to its non-invasive, rapid, and accessible cardiac imaging capabilities. These devices reduce dependence on traditional cart-based scanners and speed up clinical decision-making. Technological improvements, including compact transducers, wireless connectivity, and app-based workflows, have enhanced usability and facilitated integration into decentralized healthcare settings, expanding adoption across point-of-care and home monitoring models.

The hospitals and clinics segment generated USD 1.7 billion in 2025. This segment includes public and private hospitals, cardiac care centers, outpatient clinics, and emergency departments where handheld echocardiography devices are used for bedside assessments. These devices enable clinicians to quickly evaluate cardiac structure and function during routine check-ups, emergencies, and follow-up visits without relying on large stationary systems. High patient volumes and the growing need for rapid diagnosis and workflow efficiency contribute to the dominance of this segment.

North America Handheld Echocardiography Devices Market held a 33.6% share in 2025. The region's strong market share is attributed to the high prevalence of cardiovascular diseases and the rising need for rapid, point-of-care cardiac evaluations in hospitals, outpatient clinics, and emergency care settings. A well-established healthcare infrastructure, early adoption of portable imaging technologies, and the presence of major medical device manufacturers accelerate market growth. The North American healthcare ecosystem supports early diagnosis, timely interventions, and widespread adoption of innovative handheld echocardiography solutions.

Key players operating in the Global Handheld Echocardiography Devices Market include AliveCor, Inc., Biotronik SE & Co. KG, Boston Scientific Corporation, Butterfly Network, CHISON, Clarius, EchoNous Inc., Esaote S.p.A., Exo Imaging, Inc., Fukuda Denshi Co., Ltd., GE HealthCare Technologies Inc., Hill-Rom Holdings, Inc., Koninklijke Philips N.V., Medtronic plc, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd. Companies in the Handheld Echocardiography Devices Market are adopting several strategies to strengthen their market position. They are investing in research and development to create compact, AI-integrated, and wireless-enabled devices that enhance diagnostic accuracy and ease of use. Strategic partnerships with hospitals, clinics, and telehealth providers expand product reach and ensure integration into point-of-care workflows. Firms are also entering emerging markets to tap into growing home healthcare and remote monitoring demand. Additionally, companies focus on training programs for healthcare professionals, digital marketing campaigns, and service support infrastructure to improve adoption rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Lead type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for remote patient monitoring

- 3.2.1.2 Advancements in echocardiography technology

- 3.2.1.3 Rising cardiovascular disease incidence

- 3.2.1.4 Increasing aging population and home healthcare trends

- 3.2.2 Industry Pitfalls and Challenges:

- 3.2.2.1 Regulatory compliance and standardization

- 3.2.2.2 Limited diagnostic capability compared to traditional ECG systems

- 3.2.3 Market Opportunities

- 3.2.3.1 Rising adoption in emerging markets

- 3.2.3.2 Expansion of point-of-care diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostics ECG devices

- 5.2.1 Resting ECG

- 5.2.2 Stress ECG

- 5.3 Monitoring ECG devices

- 5.3.1 Holter monitors

- 5.3.2 Mobile cardiac telemetry (MCT)

- 5.3.3 Wearable ECG devices

- 5.3.4 Other monitoring ECG devices

Chapter 6 Market Estimates and Forecast, By Lead Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Single lead type

- 6.3 3 lead type

- 6.4 6 lead type

- 6.5 12 lead type

- 6.6 Other lead types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Diagnostic centers

- 7.4 Ambulatory surgical centers

- 7.5 Home care settings

- 7.6 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AliveCor, Inc.

- 9.2 Biotronik SE & Co. KG

- 9.3 Boston Scientific Corporation

- 9.4 Butterfly Network

- 9.5 CHISON

- 9.6 Clarius

- 9.7 EchoNous Inc.

- 9.8 Esaote S.p.A.

- 9.9 Exo Imaging, Inc.

- 9.10 Fukuda Denshi Co., Ltd.

- 9.11 GE HealthCare Technologies Inc.

- 9.12 Hill-Rom Holdings, Inc.

- 9.13 Koninklijke Philips N.V.

- 9.14 Medtronic plc

- 9.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.