|

市場調查報告書

商品編碼

2019122

行動配件市場機會、成長要素、產業趨勢分析及2026-2035年預測Mobile Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

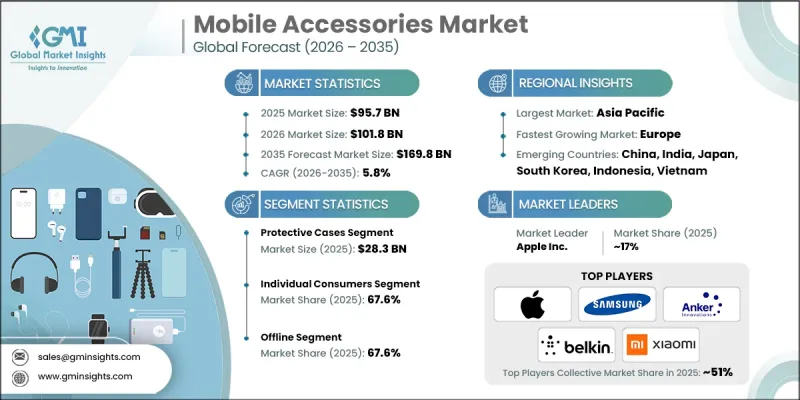

預計到 2025 年,全球行動配件市場規模將達到 957 億美元,並以 5.8% 的複合年成長率成長,到 2035 年將達到 1,698 億美元。

智慧型手機在全球範圍內的快速普及推動了市場成長,越來越多的消費者需要配件來增強和保護他們的設備。智慧型手機價格的上漲和頻繁的型號更新換代帶動了對保護殼、螢幕保護貼和充電器的需求。智慧型手機媒體消費的持續成長也顯著促進了耳機和耳塞等無線音訊設備的需求。此外,多功能高階智慧型手機的普及也推動了對高效能行動電池的需求。行動遊戲和串流媒體的興起進一步刺激了對專用配件的需求。新興市場智慧型手機滲透率的不斷提高支撐了對配件的持續需求,零售商也不斷拓展其產品線,涵蓋各種品牌和規格。穩定的智慧型手機銷售週期確保了相關行動配件的穩定需求,從而推動了市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 957億美元 |

| 預測金額 | 1698億美元 |

| 複合年成長率 | 5.8% |

預計到2025年,保護殼市場規模將達到283億美元,並在2026年至2035年間以6.5%的複合年成長率成長。這些保護殼之所以必不可少,是因為它們能夠保護設備免受意外損壞、磨損和日常使用造成的損害。隨著智慧型手機價格的上漲,消費者積極投資於耐用且抗衝擊的材質,以降低維修和更換成本。廣泛的兼容性,涵蓋多種設備品牌和型號,確保了穩定的銷售;而注重設計的保護殼則吸引了追求獨特風格的時尚消費者。頻繁的設備更換在短期內推動了重複購買。強大的零售和電商分銷網路使這些產品廣泛普及,從而保持了主導地位。

預計到2025年,個人消費者市場將佔據67.6%的市場佔有率,並在2026年至2035年間以5.3%的複合年成長率成長。該細分市場受益於智慧型手機的高普及率和消費者對設備的高度日常依賴,這推動了對保護性和性能增強型配件的需求。消費者偏好對手機殼、充電器、螢幕保護貼和音訊設備的購買有顯著影響。頻繁更換智慧型手機導致各類配件的重複購買。可支配收入的增加使得消費者能夠購買高級產品品牌產品,而電子商務平台則提供了便利的購買管道和價格比較功能。社群媒體和網路趨勢進一步加速了消費者主導的需求,並促進了全球行動配件的普及和使用。

中國行動配件市場預計到2025年將達到101億美元,並在2026年至2035年間以6%的複合年成長率成長。市場成長主要得益於智慧型手機的大規模生產和國內消費的強勁勢頭。本土品牌在無線音訊、快速充電和多功能設備等領域引領創新。數位技術和電子商務的日益普及推動了產品的快速分銷和全國範圍的覆蓋。都市區消費者對支持新興技術的先進、功能豐富的配件表現出濃厚的興趣。 5G網路的部署持續促進了高效能行動配件的普及。具有競爭力的價格和持續的產品創新維持了穩健的更換週期,並在一二線城市保持了持續的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 全球智慧型手機普及率的快速成長

- 行動裝置資訊科技創新

- 消費者對個人化的偏好日益成長

- 陷阱與挑戰

- 激烈的競爭和對價格的敏感性

- 產品快速過時

- 機會

- 高階和奢侈品配件領域的成長

- 智慧和人工智慧功能的整合

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 耳塞/頭戴式耳機

- 充電器和數據線

- 行動電池

- 保護殼

- 其他

第6章 市場估算與預測:依相容性分類,2022-2035年

- 通用/多平台相容配件

- 僅限 iOS 的配件

- 僅限安卓系統的配件

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 低價位(50美元以下)

- 中價位(50-100美元)

- 高級版(超過 100 美元)

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 個人消費者(B2C)

- 企業對企業 (B2B)

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 品牌官方網站

- 離線

- 品牌自營店

- 量販店

- 大賣場和超級市場

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Anker Innovations

- Apple Inc.

- Belkin

- Bose Corporation

- Huawei

- Incipio Group

- Mophie

- Panasonic

- Plantronics

- Samsung

- Skullcandy, Inc.

- Sony Corporation

- Spigen Inc.

- UGREEN Group Limited

- Xiaomi

The Global Mobile Accessories Market was valued at USD 95.7 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 169.8 billion by 2035.

Market growth is driven by the rapid increase in global smartphone adoption, as more consumers seek accessories that enhance device functionality and protection. Rising smartphone prices and frequent device upgrades are prompting higher demand for protective cases, screen guards, and chargers. Wireless audio devices, such as headphones and earbuds, are seeing strong adoption as media consumption on smartphones continues to rise. High-performance power banks are also increasingly in demand due to the prevalence of feature-rich, high-end smartphones. Mobile gaming and streaming trends are further boosting the need for specialized accessories. Growing smartphone penetration in emerging markets supports sustained accessory demand, while retailers continue to expand product offerings across brands and specifications. The steady sales cycles of smartphones ensure stable demand for complementary mobile accessories, reinforcing long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $95.7 Billion |

| Forecast Value | $169.8 Billion |

| CAGR | 5.8% |

The protective cases segment generated USD 28.3 billion in 2025 and is expected to grow at a CAGR of 6.5% from 2026 to 2035. These cases remain essential due to their ability to protect devices against accidental damage, wear, and daily use. Rising smartphone costs encourage consumers to invest in durable, impact-resistant materials, which reduce repair and replacement expenses. Wide compatibility across multiple device brands and models ensures consistent sales, while design-focused cases attract style-conscious buyers seeking personalized options. Frequent device upgrades drive repeat purchases within short timeframes. Strong retail and e-commerce distribution networks make these products widely accessible, maintaining their market leadership globally.

The individual consumers segment held 67.6% share in 2025 and is expected to grow at a CAGR of 5.3% from 2026 to 2035. This segment benefits from widespread smartphone ownership and daily device reliance, which fuels demand for protective and performance-enhancing accessories. Consumer preferences strongly influence purchases of cases, chargers, screen protectors, and audio devices. Frequent smartphone replacements generate repeat accessory purchases across categories. Rising disposable incomes enable spending on premium and branded products, while e-commerce platforms provide convenient access and price comparisons. Social media and online trends further accelerate consumer-driven demand, promoting higher engagement and adoption of mobile accessories worldwide.

China Mobile Accessories Market captured USD 10.1 billion in 2025 and is projected to grow at a CAGR of 6% from 2026 to 2035. Market growth is supported by large-scale smartphone production and high domestic consumption. Local brands drive innovation in wireless audio, fast charging, and multifunctional devices. Strong digital adoption and e-commerce penetration allow rapid product distribution and nationwide availability. Urban consumers show strong interest in advanced, feature-rich accessories compatible with emerging technologies. The rollout of 5G networks continues to stimulate the adoption of high-performance mobile accessories. Competitive pricing and continuous product innovation maintain strong replacement cycles and sustained demand across both tier-1 and tier-2 cities.

Key players operating in the Global Mobile Accessories Market include Anker Innovations, Apple Inc., Belkin, Bose Corporation, Huawei, Incipio Group, Mophie, Panasonic, Plantronics, Samsung, Skullcandy, Inc., Sony Corporation, Spigen Inc., UGREEN Group Limited, and Xiaomi. Companies in the Mobile Accessories Market strengthen their position by focusing on product innovation, offering high-performance, durable, and stylish accessories that cater to consumer preferences. They invest in R&D to introduce next-generation wireless audio, fast-charging devices, and gaming-specific accessories. Expanding e-commerce and retail distribution channels ensures widespread product availability and quick adoption. Strategic partnerships with smartphone manufacturers and tech brands enhance visibility and market penetration. Competitive pricing strategies, combined with promotional campaigns and influencer marketing, help capture attention in crowded markets. Companies also emphasize brand differentiation through design, technology integration, and compatibility with multiple devices, while maintaining rigorous quality control and certification standards. These approaches enable firms to sustain market share, encourage repeat purchases, and build long-term customer loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Compatibility

- 2.2.3 Price Range

- 2.2.4 End-User

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging global smartphone penetration

- 3.2.1.2 Rapid technological innovation in mobile devices

- 3.2.1.3 Growing consumer preference for personalization

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Intense competition and price sensitivity

- 3.2.2.2 Rapid product obsolescence

- 3.2.3 Opportunities

- 3.2.3.1 Growth in premium and luxury accessory segments

- 3.2.3.2 Integration of smart features and AI capabilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Earphones & headphones

- 5.3 Chargers & cables

- 5.4 Power bank

- 5.5 Protective cases

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Compatibility, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Universal/Multi-Platform Accessories

- 6.3 iOS-Specific Accessories

- 6.4 Android-Specific Accessories

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (Less than $50)

- 7.3 Mid Range ($50 to $100)

- 7.4 Premium (More than $100)

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Individual Consumers (B2C)

- 8.3 Commercial (B2B)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Brand Websites

- 9.3 Offline

- 9.3.1 Brand-owned Stores

- 9.3.2 Electronics Retailers

- 9.3.3 Hypermarkets & Supermarkets

- 9.3.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Anker Innovations

- 11.2 Apple Inc.

- 11.3 Belkin

- 11.4 Bose Corporation

- 11.5 Huawei

- 11.6 Incipio Group

- 11.7 Mophie

- 11.8 Panasonic

- 11.9 Plantronics

- 11.10 Samsung

- 11.11 Skullcandy, Inc.

- 11.12 Sony Corporation

- 11.13 Spigen Inc.

- 11.14 UGREEN Group Limited

- 11.15 Xiaomi

行動電話配件市場:2026-2032年全球市場預測(按產品類型、連接方式、相容性、製造商類型和分銷管道分類)

行動電話配件市場:2026-2032年全球市場預測(按產品類型、連接方式、相容性、製造商類型和分銷管道分類) 穿戴式裝置及行動配件市場佔有率及預測:市場概覽(2026年第一季)

穿戴式裝置及行動配件市場佔有率及預測:市場概覽(2026年第一季) 全球相機背帶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)穿戴式裝置和行動配件的市場佔有率和預測

全球相機背帶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)穿戴式裝置和行動配件的市場佔有率和預測 行動配件市場規模、佔有率和趨勢分析報告:按產品、銷售管道、地區和細分市場預測(2026-2033 年)

行動配件市場規模、佔有率和趨勢分析報告:按產品、銷售管道、地區和細分市場預測(2026-2033 年) 行動電話配件市場規模、佔有率、趨勢和預測:按產品類型、價格範圍、銷售管道和地區分類,2026-2034年實驗室千斤頂市場:依產品類型、負載能力、材料、操作模式、最終用途產業和通路分類,全球預測,2026-2032年智慧型手機長焦距鏡頭市場:按鏡頭卡口類型、焦距類型、通路、最終用戶類型和應用案例分類-全球預測,2026-2032年行動電話磁性濾鏡夾市場:依產品類型、材質、價格範圍、銷售管道、應用程式和最終用戶分類,全球預測(2026-2032年)

行動電話配件市場規模、佔有率、趨勢和預測:按產品類型、價格範圍、銷售管道和地區分類,2026-2034年實驗室千斤頂市場:依產品類型、負載能力、材料、操作模式、最終用途產業和通路分類,全球預測,2026-2032年智慧型手機長焦距鏡頭市場:按鏡頭卡口類型、焦距類型、通路、最終用戶類型和應用案例分類-全球預測,2026-2032年行動電話磁性濾鏡夾市場:依產品類型、材質、價格範圍、銷售管道、應用程式和最終用戶分類,全球預測(2026-2032年) 行動電話配件市場分析及預測(至2035年):依類型、產品、技術、材質、設備、應用、最終用戶、功能、安裝方式及解決方案分類

行動電話配件市場分析及預測(至2035年):依類型、產品、技術、材質、設備、應用、最終用戶、功能、安裝方式及解決方案分類