|

市場調查報告書

商品編碼

2019106

賽車自行車市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Racing Bike Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

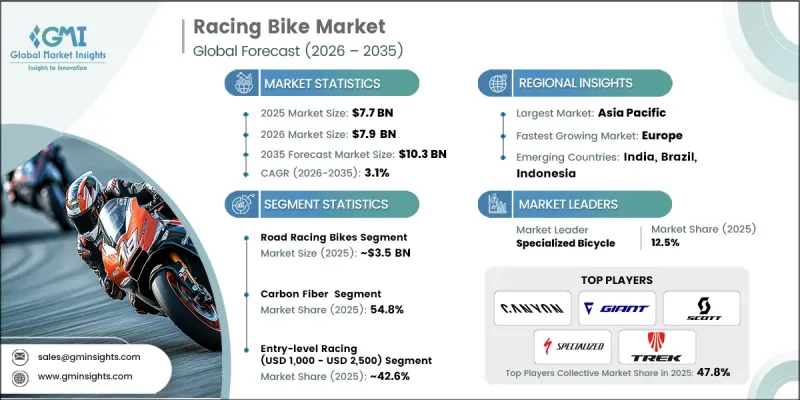

全球賽車自行車市場預計到 2025 年將價值 77 億美元,預計到 2035 年將以 3.1% 的複合年成長率成長至 103 億美元。

市場擴張的驅動力在於競技自行車賽事和各類比賽的日益普及,促使業餘和專業自行車手紛紛投資高性能自行車。輕量化車架、空氣動力學設計和尖端裝備的進步,提升了消費者對競賽自行車的興趣。自行車管理機構制定的技術規範標準,例如重量限制和幾何形狀,正在塑造產品開發的方向,並確保自行車在性能和安全性方面都達到最佳狀態。國內外自行車比賽參與度的提高,以及政府對自行車作為永續交通途徑的支持,進一步加速了市場需求。人們對健康、健身和競技運動日益成長的興趣,也推動了全球各地市場的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 77億美元 |

| 預測金額 | 103億美元 |

| 複合年成長率 | 3.1% |

公路賽車目前佔據45.4%的市場佔有率,預計到2025年市場規模將達35億美元。其受歡迎程度源自於其專為高速鋪路騎行而最佳化的設計,深受休閒騎乘者和競技騎乘者的青睞。技術創新、輕量化材料以及空氣動力學部件的進步進一步推動了公路賽車的普及,使其成為追求極致效率和速度的騎行愛好者的理想之選。

預計到2025年,碳纖維自行車市佔率將達到54.8%,市場規模將達42億美元。碳纖維之所以備受青睞,是因為它擁有卓越的強度重量比,這對於提升競技性能至關重要。製造商在設計碳纖維車架時,力求確保其具有優異的剛性和空氣動力學性能,從而最大限度地提高騎士與路面之間的動力傳輸效率。因此,在那些對速度、靈活性和耐力要求極高的賽事中,碳纖維公路車的需求量極大。

2025年美國公路車市場規模預計為12億美元,預計在2026年至2035年間以2.3%的複合年成長率成長。美國擁有成熟的自行車文化和高性能自行車市場。國內的自行車賽事和完善的自行車訓練體係正在推動消費者對高性能自行車和公路自行車的興趣。公路自行車運動、健身活動和休閒騎行的普及也促進了對技術先進、輕便耐用的公路自行車的需求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人們越來越關注健康和健身

- 參加競技自行車賽事人數增加

- 受職業賽車運動的影響和敬仰而購買。

- 基礎建設(興建專用自行車道和自行車賽車場)

- 產業潛在風險與挑戰

- 供應鏈中斷和零件短缺

- 與電動自行車和其他健身活動的競爭

- 市場機遇

- 新興市場的騎乘文化正在擴展

- 女子賽車運動的擴張

- 活動導向的租賃和共享自行車服務

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國 - 消費品安全委員會 (CPSC)

- 美國 - ASTM國際

- 加拿大 - 加拿大運輸部

- 歐洲

- 德國萊茵TÜV

- 法國 - AFNOR

- 亞太地區

- 中國國家品質監督檢驗檢疫總局

- 印度 - 標準局 (BIS)

- 拉丁美洲

- 巴西 - INMETRO

- 墨西哥 - 經濟部

- 中東和非洲

- UAE-ESMA

- 沙烏地阿拉伯 - 沙烏地阿拉伯標準、計量和品質組織 (SASO)

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 碳纖維車架

- 電子換檔(Di2/eTap)

- 液壓碟式煞車

- 空氣動力學車架設計

- 新興技術

- 智慧互聯自行車

- 先進複合材料

- 自適應動態

- 目前技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 專利趨勢(基於初步調查)

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊和關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 設備運轉率和擴建計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、局限性和監管考量

- 成本細分分析

- 消費者人口統計和心理特徵評估

- 年齡和性別分佈

- 收入和消費模式

- 以生活方式和健身為導向

- 地理因素與都市化因素

- 案例研究

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:自行車類型,2022-2035年

- 公路賽車

- 場地自行車/自行車館自行車

- 越野公路自行車

- 山地賽車自行車

- 計時賽/鐵人三項自行車

- 礫石公路賽車

第6章 市場估算與預測:依框架材質分類,2022-2035年

- 碳纖維

- 鋁合金

- 鈦

- 鋼

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 入門級賽馬(1000 美元 - 2500 美元)

- 中階性能(2500美元至5000美元)

- 高階發燒友(5000美元及以上)

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 專業賽車隊

- 業餘競技自行車手

- 性能愛好者

第9章 市場估價與預測:依銷售管道分類,2022-2035年

- 線上

- 消費者電子商務

- 品牌官方網站

- 離線

- 品牌旗艦店

- 自行車專賣店

- 獨立自行車零售店

- 品牌授權零售商

- 運動用品零售商

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 波蘭

- 荷蘭

- 挪威

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Specialized Bicycle

- Trek Bicycle

- Giant Manufacturing

- Canyon Bicycles

- Scott Sports

- Cannondale Bicycle

- Merida Industry

- Cervelo Cycles

- Pinarello

- BMC Switzerland

- 本地製造商

- Wilier Triestina

- Look Cycle

- Eddy Merckx Cycles

- De Rosa

- Fuji Bikes

- Felt Bicycles

- 新興製造商

- Factor Bikes

- 3T Cycling

- Allied Cycle Works

- Ribble Cycles

The Global Racing Bike Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 3.1% to reach USD 10.3 billion by 2035.

The market expansion is influenced by the growing popularity of competitive cycling events and organized races, which motivate both amateur and professional cyclists to invest in high-performance bikes. Advancements in lightweight frames, aerodynamic designs, and cutting-edge equipment are driving consumer interest in racing bicycles. Regulatory standards set by cycling authorities for technical specifications, such as weight limits and geometry, are shaping product development and ensuring that bikes are optimized for performance and safety. Rising participation in domestic and international cycling competitions, coupled with supportive initiatives from government bodies promoting cycling as a sustainable mode of transport, is further accelerating demand. The increasing interest in health, fitness, and performance-oriented sports is also contributing to sustained growth across various markets globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $10.3 Billion |

| CAGR | 3.1% |

The road racing bikes segment held a 45.4% share, generating USD 3.5 billion in 2025. Their popularity stems from optimized designs for high-speed performance on paved roads, appealing to both recreational and competitive cyclists. Innovations in technology, lightweight materials, and aerodynamic components have reinforced the widespread adoption of road racing bikes, making them the preferred choice for enthusiasts seeking maximum efficiency and speed.

The carbon fiber segment held 54.8% share in 2025, valued at USD 4.2 billion. Carbon fiber is preferred due to its exceptional strength-to-weight ratio, which is crucial for competitive performance. Manufacturers design carbon fiber frames to ensure superior rigidity and aerodynamics, maximizing power transfer between rider and road. This has made carbon fiber racing bikes highly desirable for events where speed, agility, and endurance are critical.

U.S. Racing Bike Market was valued at USD 1.2 billion in 2025 and is expected to grow at a CAGR of 2.3% from 2026 to 2035. The United States has a well-established cycling culture and a mature market for performance-oriented bicycles. Domestic competitive events and structured cycling programs drive consumer interest in high-performance and racing bikes. The popularity of road cycling, fitness initiatives, and recreational biking also supports demand for technologically advanced, lightweight, and durable racing bicycles.

Key players operating in the Global Racing Bike Market include BMC, Cannondale, Canyon, Cervelo, Giant, Merida, Pinarello, Scott, Specialized, and Trek. Companies in the Global Racing Bike Market are leveraging technological innovation, lightweight materials, and aerodynamic designs to strengthen their market presence. They invest in R&D to develop carbon fiber frames, advanced drivetrains, and high-performance components that cater to both professional and amateur cyclists. Strategic partnerships with competitive cycling events, sponsorships, and collaborations with professional riders help brands build credibility and visibility. Expanding online and retail distribution networks allows companies to reach global markets efficiently. Additionally, firms are focusing on customization options, limited-edition models, and integrated digital performance tracking to differentiate products, enhance user experience, and capture a loyal customer base while maintaining premium positioning in the competitive racing bike segment.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Bike

- 2.2.3 Frame Material

- 2.2.4 Price Range

- 2.2.5 End-Use

- 2.2.6 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing health & fitness consciousness

- 3.2.1.2 Rising participation in competitive cycling events

- 3.2.1.3 Professional racing influence & aspirational purchases

- 3.2.1.4 Infrastructure development (bike lanes, velodrome construction)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions & component shortages

- 3.2.2.2 Competition from e-bikes & alternative fitness activities

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets with growing cycling culture

- 3.2.3.2 Women's racing segment expansion

- 3.2.3.3 Rental & bike-sharing for events

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Consumer Product Safety Commission (CPSC)

- 3.4.1.2 U.S. - ASTM International

- 3.4.1.3 Canada - Transport Canada

- 3.4.2 Europe

- 3.4.2.1 Germany - TUV Rheinland

- 3.4.2.2 France - AFNOR

- 3.4.3 Asia Pacific

- 3.4.3.1 China - AQSIQ

- 3.4.3.2 India - Bureau of Indian Standards (BIS)

- 3.4.4 Latin America

- 3.4.4.1 Brazil - INMETRO

- 3.4.4.2 Mexico - Secretaria de Economia

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - ESMA

- 3.4.5.2 Saudi Arabia - Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Carbon Fiber Frames

- 3.8.1.2 Electronic Shifting (Di2 / eTap)

- 3.8.1.3 Hydraulic Disc Brakes

- 3.8.1.4 Aerodynamic Frame Design

- 3.8.2 Emerging technologies

- 3.8.2.1 Smart Connected Bikes

- 3.8.2.2 Advanced Composite Materials

- 3.8.2.3 Adaptive Aerodynamics

- 3.8.1 Current technologies

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Capacity & Production Landscape (Driven by Primary Research)

- 3.12.1 Installed Capacity by Region & Key Producer

- 3.12.2 Capacity Utilization Rates & Expansion Pipelines

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Cost breakdown analysis

- 3.15 Consumer demographics & psychographics assessment

- 3.15.1 Age and gender distribution

- 3.15.2 Income and spending patterns

- 3.15.3 Lifestyle and fitness orientation

- 3.15.4 Geographic and urbanization factors

- 3.16 Case studies

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Bike, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Road racing bikes

- 5.3 Track/Velodrome bikes

- 5.4 Cyclocross bikes

- 5.5 Mountain racing bikes

- 5.6 Time Trial/Triathlon bikes

- 5.7 Gravel racing bikes

Chapter 6 Market Estimates & Forecast, By Frame Material, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Carbon fiber

- 6.3 Aluminum alloy

- 6.4 Titanium

- 6.5 Steel

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Entry-level racing (USD 1,000 - USD 2,500)

- 7.3 Mid-range performance (USD 2,500 - USD 5,000)

- 7.4 High-end enthusiast (Above USD 5,000)

Chapter 8 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Professional racing teams

- 8.3 Amateur competitive cyclists

- 8.4 Performance enthusiasts

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 Direct-to-consumer e-commerce

- 9.2.2 Brand website

- 9.3 Offline

- 9.3.1 Brand flagship stores

- 9.3.2 Specialty bike shops

- 9.3.2.1 Independent bike retailers

- 9.3.2.2 Authorized brand dealers

- 9.3.3 Sporting goods retailers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.3.8 Norway

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Specialized Bicycle

- 11.1.2 Trek Bicycle

- 11.1.3 Giant Manufacturing

- 11.1.4 Canyon Bicycles

- 11.1.5 Scott Sports

- 11.1.6 Cannondale Bicycle

- 11.1.7 Merida Industry

- 11.1.8 Cervelo Cycles

- 11.1.9 Pinarello

- 11.1.10 BMC Switzerland

- 11.2 Regional players

- 11.2.1 Wilier Triestina

- 11.2.2 Look Cycle

- 11.2.3 Eddy Merckx Cycles

- 11.2.4 De Rosa

- 11.2.5 Fuji Bikes

- 11.2.6 Felt Bicycles

- 11.3 Emerging players

- 11.3.1 Factor Bikes

- 11.3.2 3T Cycling

- 11.3.3 Allied Cycle Works

- 11.3.4 Ribble Cycles

2026-2030年全球登山車市場

2026-2030年全球登山車市場 2026年全球山地自行車市場報告2026年全球山地電動自行車市場報告

2026年全球山地自行車市場報告2026年全球山地電動自行車市場報告 電動山地自行車市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

電動山地自行車市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 山地自行車懸吊市場按產品類型、應用和地區分類

山地自行車懸吊市場按產品類型、應用和地區分類 賽車摩托車座椅市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、座椅高度、銷售通路、地區和競爭格局分類,2020-2030 年預測山地車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、類型、應用、地區和競爭格局分類,2020-2030 年預測

賽車摩托車座椅市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、座椅高度、銷售通路、地區和競爭格局分類,2020-2030 年預測山地車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、類型、應用、地區和競爭格局分類,2020-2030 年預測 全球電動越野自行車市場山地電動自行車市場-全球產業規模、佔有率、趨勢、機會和預測,按電池、類型、應用、地區和競爭細分,2020-2030 年

全球電動越野自行車市場山地電動自行車市場-全球產業規模、佔有率、趨勢、機會和預測,按電池、類型、應用、地區和競爭細分,2020-2030 年 山地電動自行車市場規模、佔有率、趨勢分析報告:按驅動系統、電池、推進器、地區、細分市場預測,2025-2030 年

山地電動自行車市場規模、佔有率、趨勢分析報告:按驅動系統、電池、推進器、地區、細分市場預測,2025-2030 年