|

市場調查報告書

商品編碼

2019095

CNC等電漿切割機市場機會、成長要素、產業趨勢分析及2026-2035年預測。CNC Plasma Cutting Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

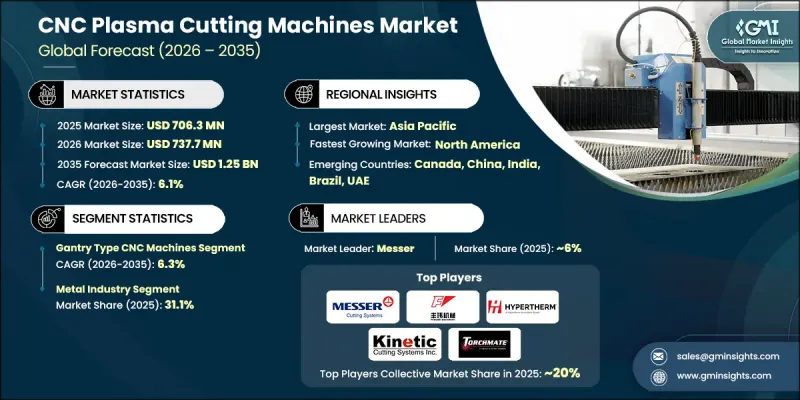

2025年全球數控等電漿切割機市值為7.063億美元,預計2035年將以6.1%的複合年成長率成長至12.5億美元。

物聯網系統、人工智慧驅動的預測性維護和智慧監控解決方案的日益普及正在改變製造環境,實現即時效能追蹤、減少人為錯誤並最佳化生產效率。汽車、航太、重工業和造船等行業對高精度、可重複且經濟高效的切割解決方案的需求日益成長。數控等離子切割系統因其速度快、運行效率高以及能夠加工中重型金屬板材而備受青睞,其性能優於機械和雷射切割方式。隨著企業尋求能夠無縫整合到智慧工廠生態系統中,即使在大批量生產中也能提供穩定品質和高產量的設備,數位化製造工作流程的轉變進一步推動了這些技術的應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 7.063億美元 |

| 預測金額 | 12.5億美元 |

| 複合年成長率 | 6.1% |

預計到2025年,龍門式數控等電漿切割機規模將達到3.889億美元,並在2026年至2035年間以6.3%的複合年成長率成長。龍門系統具有高結構剛性,能夠精確切割大型金屬板材和厚材料。其穩定性和精度使其成為需要在長距離上高速作業的重工業領域的首選。

金屬加工領域佔31.1%的市場佔有率,預計到2035年將以6.6%的複合年成長率成長。此領域涵蓋鋼鐵加工、合金加工和工業機械加工,這些領域均依賴數控等離子切割系統對鋼、鋁和銅等金屬進行精確切割。建築、汽車和造船等行業對金屬加工零件日益成長的全球需求,推動了對能夠實現大批量、高精度生產的先進等離子切割系統的需求。

美國數控等電漿切割機市場預計到2025年將達到1.29億美元,並在2026年至2035年間以6.2%的複合年成長率成長。美國在該市場的主導地位得益於其對數位化製造技術的早期應用、強大的工業基礎設施以及在汽車、航太和重工業領域的雄厚實力。美國製造商正日益將人工智慧、預測性維護和物聯網系統整合到生產過程中,從而提高數控等離子切割解決方案的效率、精度和成本效益。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 自動化和工業4.0的普及應用

- 汽車、航太和重工業領域的需求不斷成長。

- 對經濟高效的高速金屬切削的需求日益成長。

- 產業潛在風險與挑戰

- 由於替代技術的出現,競爭異常激烈。

- 高昂的資本投資成本和推廣障礙

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按模型

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依車型分類,2022-2035年

- 龍門式CNC工具工具機

- 桌上型CNC工具工具機

- 其他(多用途等)

第6章 市場估計與預測:依類型分類,2022-2035年

- 可攜式的

- 固定的

第7章 市場估計與預測:依技術分類,2022-2035年

- 傳統等離子體系統

- 高清等離子系統

第8章 市場估計與預測:依發電容量分類,2022-2035年

- 小於120安培

- 121-300安培

- 超過300安培

第9章 市場估算與預測:依自動化程度分類,2022-2035年

- 半自動

- 全自動

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 金屬加工

- 木工

- 石材加工

- 其他(玻璃加工等)

第11章 市場估計與預測:依最終用途產業分類,2022-2035年

- 車

- 金屬工業

- 製造業

- 航太/國防

- 航運/海事

- 建築和基礎設施

- 其他(能源、電力等)

第12章 市場估計與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第13章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第14章:公司簡介

- Ador Welding

- Ajan Electronics

- AKS Cutting Systems

- ALLtra

- Daihen

- Fengwei

- Hildebrand Machinery

- Hornet Cutting Systems

- Hypertherm

- Kinetic

- Koike Aronson

- Kutavar

- Messer

- Torchmate

- Zinser Cutting Systems

The Global CNC Plasma Cutting Machines Market was valued at USD 706.3 million in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 1.25 billion by 2035.

The rising adoption of IoT-enabled systems, AI-driven predictive maintenance, and smart monitoring solutions is transforming fabrication environments, allowing for real-time performance tracking, reduced human error, and optimized production efficiency. Industries such as automotive, aerospace, heavy engineering, and shipbuilding are driving demand for high-precision, repeatable, and cost-efficient cutting solutions. CNC plasma cutting systems are favored for their speed, operational efficiency, and ability to handle mid- to thick-gauge metals, outperforming mechanical and laser alternatives. The shift toward digitalized manufacturing workflows is further boosting adoption, as companies seek machines that integrate seamlessly into smart factory ecosystems, offering consistent quality and high throughput across large production volumes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $706.3 Million |

| Forecast Value | $1.25 Billion |

| CAGR | 6.1% |

The gantry-type CNC plasma machines generated USD 388.9 million in 2025 and are expected to grow at a CAGR of 6.3% from 2026 to 2035. Gantry systems provide high structural rigidity, enabling precise cutting of larger sheets and thicker materials. Their stability and enhanced accuracy make them a preferred choice for heavy fabrication industries that require high-speed operations over extended cutting spans.

The metal segment held 31.1% share and is projected to grow at a CAGR of 6.6% through 2035. This segment includes steel fabrication, alloy processing, and industrial machining sectors, which rely on CNC plasma systems for precise cutting of metals like steel, aluminum, and copper. Growing global demand for fabricated metal components across construction, automotive, and shipbuilding sectors is driving the need for advanced plasma cutting systems capable of high-volume, high-precision production.

U.S. CNC Plasma Cutting Machines Market reached USD 129 million in 2025 and is expected to grow at a CAGR of 6.2% between 2026 and 2035. The country's leadership is supported by early adoption of digital manufacturing technologies, robust industrial infrastructure, and a strong presence of automotive, aerospace, and heavy engineering sectors. U.S. manufacturers increasingly integrate AI, predictive maintenance, and IoT-enabled systems into production, enhancing the efficiency, accuracy, and cost-effectiveness of CNC plasma cutting solutions.

Key companies operating in the Global CNC Plasma Cutting Machines Market include Ador Welding, Ajan Electronics, AKS Cutting Systems, ALLtra, Daihen, Fengwei, Hildebrand Machinery, Hornet Cutting Systems, Hypertherm, Kinetic, Koike Aronson, Kutavar, Messer, Torchmate, and Zinser Cutting Systems. Companies in the Global CNC Plasma Cutting Machines Market are strengthening their positions through continuous innovation, expanding product portfolios, and investing in smart manufacturing technologies. They are focusing on integrating IoT-enabled systems, AI-based predictive maintenance, and remote monitoring solutions to enhance efficiency and minimize downtime. Strategic collaborations with industrial manufacturers enable co-development of tailored solutions for specific production requirements. Many firms are expanding their global distribution networks and localized manufacturing capabilities to reach emerging markets. Continuous R&D for high-speed, energy-efficient, and precise cutting systems ensures they meet evolving industrial demands. Additionally, companies are offering value-added services like training, technical support, and after-sales maintenance to build long-term customer relationships and reinforce market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine type

- 2.2.3 Type

- 2.2.4 Technology type

- 2.2.5 Power capacity

- 2.2.6 Automation grade

- 2.2.7 Application

- 2.2.8 End use industry

- 2.2.9 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of automation & industry 4.0

- 3.2.1.2 Increasing demand across automotive, aerospace & heavy manufacturing

- 3.2.1.3 Increasing need for cost-efficient, high-speed metal cutting

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition from alternative technologies

- 3.2.2.2 High capital costs & adoption barriers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By machine type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Gantry type CNC machines

- 5.3 Table type CNC machines

- 5.4 Others (dual purpose etc.)

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Portable

- 6.3 Fixed

Chapter 7 Market Estimates & Forecast, By Technology Type, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Conventional plasma systems

- 7.3 High-definition (HD) plasma systems

Chapter 8 Market Estimates & Forecast, By Power Capacity, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 <120 Amp

- 8.3 121-300 Amp

- 8.4 Above 300 Amp

Chapter 9 Market Estimates & Forecast, By Automation Grade, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Semi-automatic

- 9.3 Fully automatic

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Metal working

- 10.3 Wood working

- 10.4 Stone working

- 10.5 Others (glass working etc.)

Chapter 11 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 Automotive

- 11.3 Metal industry

- 11.4 Manufacturing

- 11.5 Aerospace & defense

- 11.6 Shipping and maritime

- 11.7 Construction and infrastructure

- 11.8 Others (energy & power etc.)

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 12.1 Key trends

- 12.2 Direct sales

- 12.3 Indirect sales

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.4.6 Indonesia

- 13.4.7 Malaysia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 Saudi Arabia

- 13.6.2 UAE

- 13.6.3 South Africa

Chapter 14 Company Profiles

- 14.1 Ador Welding

- 14.2 Ajan Electronics

- 14.3 AKS Cutting Systems

- 14.4 ALLtra

- 14.5 Daihen

- 14.6 Fengwei

- 14.7 Hildebrand Machinery

- 14.8 Hornet Cutting Systems

- 14.9 Hypertherm

- 14.10 Kinetic

- 14.11 Koike Aronson

- 14.12 Kutavar

- 14.13 Messer

- 14.14 Torchmate

- 14.15 Zinser Cutting Systems