|

市場調查報告書

商品編碼

2019091

單元貨載設備市場機會、成長要素、產業趨勢分析及2026-2035年預測Unit Load Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

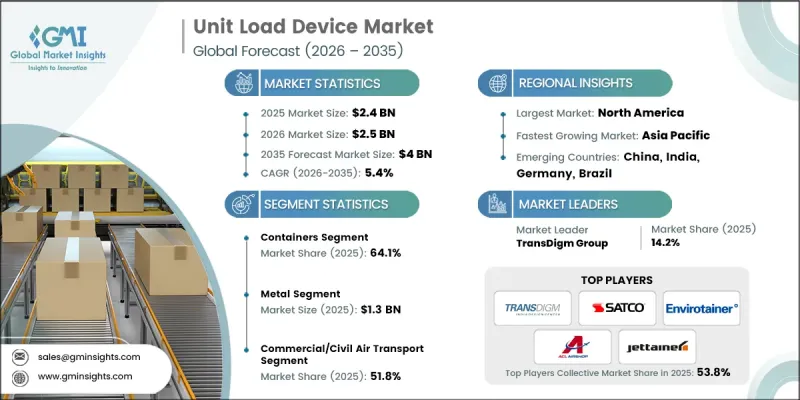

全球單元貨載設備市場預計到 2025 年將達到 24 億美元,預計到 2035 年將達到 40 億美元,年複合成長率為 5.4%。

市場擴張主要受航空貨運的快速成長和電子商務物流的持續發展所驅動,這兩者都需要更快、更有效率的貨物處理系統。寬體飛機和專用貨機的交付增加進一步刺激了市場需求,因為每種飛機都需要與之相符的貨物處理解決方案。此外,該行業也在向先進材料轉型,輕質複合材料和混合型貨櫃(ULD)因其在營運和燃油單元貨載方面的優勢而日益普及。航空公司也在加速向外包和服務共用轉型,以提高營運效率並降低成本。溫控物流的整合和貨物保護系統的改進也在塑造市場需求趨勢,而數位追蹤技術則持續提升全球航空物流網路的效率、可視性和資產利用率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 24億美元 |

| 預測金額 | 40億美元 |

| 複合年成長率 | 5.4% |

航空貨運業務的擴張和跨境電子商務的活性化持續顯著影響著單元貨載(ULD)的需求。這是因為貨運量的增加需要更有效率的貨物裝卸和更短的飛機週轉時間。對專用貨機和客機貨運能力的日益依賴推動了對標準化貨櫃和托盤的需求。同時,全球飛機機隊的不斷成長也持續創造對工廠安裝和替換型貨櫃解決方案的需求,從而支撐著航空公司和貨運公司市場的長期成長。

隨著航空公司將減輕重量和提高燃油效率作為首要任務,複合材料和混合材料的出現正在改變競爭格局。與傳統的鋁結構相比,複合材料設計具有更高的耐久性、更低的維護需求以及對溫控貨物運輸的更強適應性。這些創新在處理易碎和高價值貨物方面尤其重要,促使其在全球航空流動系統中得到越來越廣泛的應用。

貨櫃憑藉其柔軟性、耐用性和與多種機型的兼容性,預計到2025年將佔據64.1%的市場佔有率。這些貨櫃能夠實現高效率的裝卸作業,同時增強貨物保護並滿足溫控貨物等特殊運輸需求。其標準化的規格有助於提高營運效率和機隊的有效利用,使其成為客運和貨運的首選。

受航空航太業對輕量化和節能解決方案需求不斷成長的推動,複合材料市場預計將在2026年至2035年間以7.2%的複合年成長率成長。這些材料有助於減輕飛機重量、提高負載容量並增強設計柔軟性,從而實現模組化和溫控配置。隨著航空公司和物流營運商追求成本效益和永續性,基於複合材料的航空集裝器(ULD)正成為現代貨運營運中不可或缺的一部分。

預計到2025年,北美單元貨載(ULD)市佔率將達到36.9%,這得益於全部區域強大的航空貨運基礎設施和龐大的客運量。機隊規模的持續擴張和電子商務貨運量的成長正在推動對標準化貨運解決方案的需求。先進的物流系統和基礎設施正在提高ULD的處理效率,而數位追蹤和物聯網系統的加大投入則增強了營運視覺性和資產管理能力。該地區輕量化ULD解決方案的採用率也在不斷提高,旨在降低營運成本並提高燃油效率。此外,對ULD池管理和維護外包服務的需求不斷成長,使航空公司能夠最佳化資源配置,專注於核心業務。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 航空貨運和電子商務業務的擴張

- 寬體飛機和貨機的交付。

- 輕質複合材料和溫控超輕量貨櫃的廣泛應用

- 數位化與物聯網賦能的智慧ULD

- 航空公司外包和共享服務增加

- 產業潛在風險與挑戰

- 先進複合材料和智慧ULD的初始成本較高

- 監管和認證合規要求

- 市場機遇

- 延長超大容量設備 (ULD)維修和更換週期

- 新興市場航空貨運的擴張

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 容器

- LD容器

- 主甲板貨櫃

- 調色盤

- 其他

第6章 市場估計與預測:依材料分類,2022-2035年

- 金屬

- 複合材料

- 其他

第7章 市場估價與預測:依貨櫃類型分類,2022-2035年

- 標準容器

- 溫控容器

- 其他

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 民用航空運輸

- 貨物空運

- 軍用/特種任務飛機

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- TransDigm Group

- Safran Group

- Unilode Aviation Solutions

- Envirotainer AB

- CSafe Global

- Jettainer GmbH

- ACL Airshop

- 本地球員

- Satco, Inc.

- Brambles Limited(CHEP Aerospace Solutions)

- DoKaSch GmbH

- Nordisk Aviation Products AS

- PalNet GmbH

- 小眾玩家

- Cargo Composites

- VRR Aviation

- Taiwan Fylin Industrial Co., Ltd.

- Wuxi Aviation Products Co., Ltd.

- Shanghai Avifit Co., Ltd.

- AAR Corp

The Global Unit Load Device Market was estimated at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 4 billion by 2035.

Market expansion is fueled by the rapid acceleration of air freight activity and the continuous rise in e-commerce logistics, both of which demand faster and more efficient cargo movement systems. Increasing deliveries of wide-body aircraft and dedicated freighters are further strengthening demand, as each aircraft requires compatible cargo handling solutions. The industry is also experiencing a shift toward advanced materials, with lightweight composite and hybrid ULDs gaining traction due to their operational and fuel-saving benefits. Additionally, airlines are increasingly turning toward outsourcing and pooling services to streamline operations and reduce costs. The integration of temperature-sensitive logistics and improved cargo protection systems is also shaping demand patterns, while digital tracking technologies continue to enhance efficiency, visibility, and asset utilization across global aviation logistics networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4 Billion |

| CAGR | 5.4% |

The expansion of air cargo operations and cross-border e-commerce activity continues to significantly influence demand for unit load devices, as growing shipment volumes require streamlined cargo handling and quicker aircraft turnaround times. Increasing reliance on both dedicated cargo aircraft and passenger aircraft belly capacity is driving the need for standardized containers and pallets. At the same time, the rise in global aircraft fleet size is creating sustained demand for both factory-installed and replacement ULD solutions, supporting long-term market growth across airline and cargo operator segments.

The transition toward composite and hybrid ULD materials is transforming the competitive landscape, as airlines prioritize weight reduction and fuel efficiency. Compared to traditional aluminum structures, composite designs offer improved durability, reduced maintenance requirements, and better adaptability for temperature-controlled cargo transport. These innovations are particularly valuable for handling sensitive and high-value goods, contributing to their growing adoption across global aviation logistics systems.

The containers segment accounted for 64.1% share in 2025, supported by its flexibility, durability, and compatibility across various aircraft types. These containers facilitate efficient loading and unloading processes while offering enhanced cargo protection and supporting specialized transport needs such as temperature-sensitive shipments. Their standardized formats contribute to improved operational efficiency and better utilization of airline fleets, making them a preferred choice for both passenger and cargo operations.

The composite materials segment is anticipated to grow at a CAGR of 7.2% during 2026-2035, driven by the aviation sector's increasing focus on lightweight and fuel-efficient solutions. These materials contribute to reduced aircraft weight, higher payload capacity, and improved design flexibility, enabling modular and temperature-controlled configurations. As airlines and logistics providers seek cost efficiency and sustainability, composite ULDs are becoming an essential component of modern cargo operations.

North America Unit Load Device Market accounted for 36.9% share in 2025, supported by strong air cargo infrastructure and high passenger traffic across the region. Continued fleet expansion and increasing shipment volumes from e-commerce are driving demand for standardized cargo solutions. Advanced logistics systems and infrastructure enhance ULD handling efficiency, while growing investments in digital tracking and IoT-enabled systems improve operational visibility and asset management. The region is also witnessing increased adoption of lightweight ULD solutions to reduce operational costs and improve fuel efficiency. Additionally, the rising preference for outsourced ULD pooling and maintenance services is enabling airlines to focus on core operations while ensuring optimized resource utilization.

Key players operating in the Global Unit Load Device Market include TransDigm Group, Safran Group, Unilode Aviation Solutions, Envirotainer AB, CSafe Global, Jettainer GmbH, ACL Airshop, Satco, Inc., Brambles Limited (CHEP Aerospace Solutions), DoKaSch GmbH, Nordisk Aviation Products AS, PalNet GmbH, Cargo Composites, VRR Aviation, Taiwan Fylin Industrial Co., Ltd., Wuxi Aviation Products Co., Ltd., Shanghai Avifit Co., Ltd., and AAR Corp. Companies in the Unit Load Device Market are focusing on strategic initiatives to strengthen their competitive position and expand global reach. They are investing in advanced materials such as composites to improve product performance and reduce lifecycle costs. Partnerships and long-term contracts with airlines and logistics providers are being prioritized to secure recurring revenue streams. Firms are also expanding ULD pooling and leasing services to enhance customer flexibility and operational efficiency. Digital transformation, including IoT-based tracking and fleet management systems, is becoming a key focus area to improve asset visibility and utilization.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product Type trends

- 2.2.2 Material trends

- 2.2.3 Container Type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of air cargo and e-commerce operations

- 3.2.1.2 Growth in wide-body and freighter aircraft deliveries

- 3.2.1.3 Rising adoption of lightweight composite and temperature-controlled ULDs

- 3.2.1.4 Digitalization and IoT-enabled smart ULDs

- 3.2.1.5 Increasing airline outsourcing and pooling services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced composite and smart ULDs

- 3.2.2.2 Regulatory and certification compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growing ULD retrofit and replacement cycle

- 3.2.3.2 Expansion of air cargo in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Containers

- 5.2.1 LD containers

- 5.2.2 Main deck containers

- 5.3 Pallets

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Composite

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Container Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Standard container

- 7.3 Temperature-controlled container

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Commercial/civil air transport

- 8.3 Cargo/freight air transport

- 8.4 Military & special mission aircraft

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 TransDigm Group

- 10.1.2 Safran Group

- 10.1.3 Unilode Aviation Solutions

- 10.1.4 Envirotainer AB

- 10.1.5 CSafe Global

- 10.1.6 Jettainer GmbH

- 10.1.7 ACL Airshop

- 10.2 Regional Players

- 10.2.1 Satco, Inc.

- 10.2.2 Brambles Limited (CHEP Aerospace Solutions)

- 10.2.3 DoKaSch GmbH

- 10.2.4 Nordisk Aviation Products AS

- 10.2.5 PalNet GmbH

- 10.3 Niche Players

- 10.3.1 Cargo Composites

- 10.3.2 VRR Aviation

- 10.3.3 Taiwan Fylin Industrial Co., Ltd.

- 10.3.4 Wuxi Aviation Products Co., Ltd.

- 10.3.5 Shanghai Avifit Co., Ltd.

- 10.3.6 AAR Corp

單元貨載設備市場:按類型、材料、貨櫃、飛機類型、所有權和最終用戶分類-2026-2032年全球市場預測

單元貨載設備市場:按類型、材料、貨櫃、飛機類型、所有權和最終用戶分類-2026-2032年全球市場預測 2026年全球單元貨載設備市場報告

2026年全球單元貨載設備市場報告 航空貨物單元貨載設備市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用類型、甲板類型、地區和競爭對手分類,2021-2031年

航空貨物單元貨載設備市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用類型、甲板類型、地區和競爭對手分類,2021-2031年 2032 年航空貨運單元貨載設備市場預測:按類型、材料、甲板類型、飛機類型、負載容量、應用和地區進行的全球分析

2032 年航空貨運單元貨載設備市場預測:按類型、材料、甲板類型、飛機類型、負載容量、應用和地區進行的全球分析 航空貨物單元貨載設備(ULD)的全球市場規模:各類型,各材料,各用途,各地區,範圍及預測到 2030 年單元貨載設備市場預測:按產品類型、材料類型、應用和地區進行的全球分析

航空貨物單元貨載設備(ULD)的全球市場規模:各類型,各材料,各用途,各地區,範圍及預測到 2030 年單元貨載設備市場預測:按產品類型、材料類型、應用和地區進行的全球分析