|

市場調查報告書

商品編碼

2019087

心絞痛治療市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Angina Pectoris Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

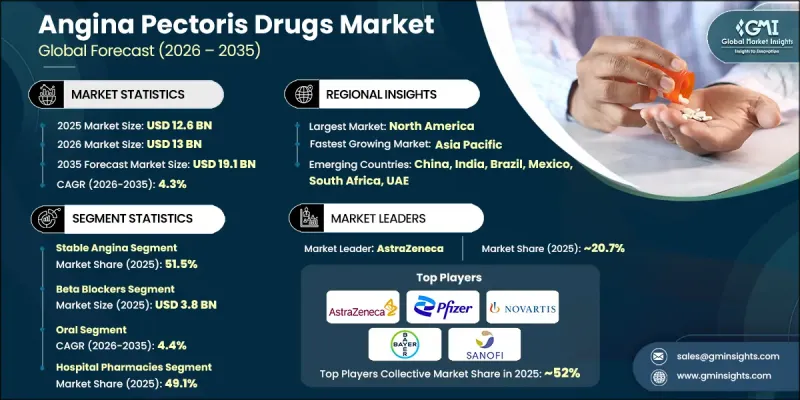

2025 年全球心絞痛治療市場規模預估為 126 億美元,預計到 2035 年將達到 191 億美元,年複合成長率為 4.3%。

心絞痛治療市場正受到生活方式相關風險因素增加的推動,例如不良飲食、缺乏運動和壓力增加。這些因素導致心血管疾病發生率上升,進而導致更多患者患有心絞痛相關疾病,增加了對有效治療方法的需求。醫療基礎設施的進步和醫療服務可近性的提高也為心絞痛治療市場提供了支持。此外,人們對心臟健康的日益重視和早期診斷的普及促進了及時治療,進一步推動了市場成長。隨著醫療體係不斷致力於慢性病管理和改善患者預後,預計心絞痛治療市場將在已開發地區和新興地區穩步擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 126億美元 |

| 預測金額 | 191億美元 |

| 複合年成長率 | 4.3% |

心絞痛治療市場涵蓋多種治療方案,旨在透過改善血流和降低心臟耗氧量來控制胸痛並改善心臟功能。治療方法包括多種藥物類別,有助於控制症狀、預防復發並降低併發症風險。學名藥的日益普及也推動了心絞痛治療市場的發展。這使得患者,尤其是在對成本敏感的地區,能夠獲得更經濟實惠的選擇,從而擴大了患者的治療範圍。同時,製劑和給藥機制的持續創新提高了治療依從性,最大限度地減少了副作用,並改善了整體治療效果,從而支持了市場的持續成長。

到2025年,穩定型心絞痛市場將佔據51.5%的市場佔有率,這反映出其在心血管疾病患者中的廣泛存在。此細分市場的成長主要得益於對有效控制症狀的長期治療方案的持續需求。心絞痛治療市場受益於成熟的治療方法,這些方法支持有效的疾病管理。此外,公眾意識的提高和診斷能力的提升也促進了檢出率的提高,進一步推動了該細分市場的成長。

預計到2025年,BETA受體阻斷劑市場規模將達38億美元,繼續在心絞痛治療市場發揮核心作用。這些藥物因其調節心臟功能和改善患者預後的能力而被廣泛應用。 BETA受體阻斷劑廣泛的臨床應用,特別是在心血管疾病的治療方面,支撐了心絞痛治療市場的發展。相關健康問題的日益普遍進一步推動了對這些治療方法的需求,並促進了該細分市場的成長。

預計到2025年,北美心絞痛治療市佔率將達到41.2%,並在2026年至2035年間以4.2%的複合年成長率成長。先進的醫療基礎設施、較高的健康意識以及患者積極接受治療是推動市場成長的主要因素。對醫療體系的持續投入和不斷進行的研究舉措也促進了市場需求的持續成長,而完善的健保報銷機制則進一步提高了病患獲得治療的機會。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 心血管疾病盛行率增加

- 藥物研發進展

- 生活方式相關風險因素增加

- 產業潛在風險與挑戰

- 藥物相關的副作用

- 微創手術的廣泛應用

- 市場機遇

- 擴大生物相似藥和學名藥。

- 新型配送系統開發進展

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

- 價格分析(基於初步調查)

- 管道分析

- 人工智慧和生成式人工智慧對市場的影響

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 穩定性心絞痛

- 不穩定型心絞痛

- 微血管性心絞痛

- Prinzmetal型心絞痛

第6章 市場估計與預測:依藥物類別分類,2022-2035年

- BETA阻斷劑

- 硝酸鹽

- 抗血小板藥物

- 鈣通道阻斷劑

- 抗凝血物

- ACE抑制劑

- 其他藥物分類

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

- 外用

第8章 市場估算與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AdvaCare Pharma

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim International

- Cadila Pharmaceuticals

- Eli Lilly and Company

- Gilead Sciences

- GlaxoSmithKline

- Merck

- Novartis

- Otsuka Pharmaceutical

- Pfizer

- Sanofi

The Global Angina Pectoris Drugs Market was valued at USD 12.6 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 19.1 billion by 2035.

The angina pectoris drugs market is driven by the increasing prevalence of lifestyle-related risk factors, including poor dietary habits, physical inactivity, and rising stress levels, which are contributing to a higher incidence of cardiovascular conditions. These factors are leading to a growing number of patients affected by conditions associated with angina, thereby increasing the demand for effective treatment options. The angina pectoris drugs market is also supported by advancements in healthcare infrastructure and improved access to medical therapies. In addition, rising awareness regarding heart health and early diagnosis is encouraging timely treatment, further strengthening market growth. As healthcare systems continue to focus on managing chronic conditions and improving patient outcomes, the angina pectoris drugs market is expected to expand steadily across both developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.6 Billion |

| Forecast Value | $19.1 Billion |

| CAGR | 4.3% |

The angina pectoris drugs market encompasses a range of therapeutic options designed to manage chest pain and improve cardiac function by enhancing blood flow or reducing the heart's oxygen demand. Treatment approaches include multiple drug categories that help control symptoms, prevent recurring episodes, and lower the risk of complications. The angina pectoris drugs market is also benefiting from the growing availability of generic medications, which have improved affordability and expanded patient access, particularly in cost-sensitive regions. At the same time, continuous innovation in drug formulations and delivery mechanisms is improving treatment adherence, minimizing side effects, and enhancing overall therapeutic outcomes, supporting ongoing market development.

The stable angina segment accounted for 51.5% share in 2025, reflecting its widespread occurrence among patients with cardiovascular conditions. This segment is driven by the consistent need for long-term management therapies that effectively control symptoms. The angina pectoris drugs market benefits from established treatment approaches that support reliable disease management. Increasing awareness and improved diagnostic capabilities are also contributing to higher detection rates, further supporting the growth of this segment.

The beta blockers segment was valued at USD 3.8 billion in 2025 and continues to play a central role in the angina pectoris drugs market. These medications are widely used due to their ability to regulate heart function and improve patient outcomes. The angina pectoris drugs market is supported by the broad clinical application of beta blockers, particularly in managing cardiovascular conditions. The rising prevalence of associated health conditions is further driving demand for these therapies, reinforcing segment growth.

North America Angina Pectoris Drugs Market accounted for 41.2% share in 2025 and is expected to grow at a CAGR of 4.2% during 2026-2035. The angina pectoris drugs market in the region is supported by advanced healthcare infrastructure, high awareness levels, and strong adoption of medical treatments. Continued investment in healthcare systems and ongoing research initiatives are contributing to sustained demand, while supportive reimbursement frameworks are further enhancing access to treatment.

Key companies operating in the Global Angina Pectoris Drugs Market include Pfizer, Novartis, AstraZeneca, Bayer, Sanofi, Merck, Eli Lilly and Company, Amgen, GlaxoSmithKline, Boehringer Ingelheim International, Gilead Sciences, Otsuka Pharmaceutical, Cadila Pharmaceuticals, and AdvaCare Pharma. Companies in the Angina Pectoris Drugs Market are focusing on strengthening their position through continuous research and development and strategic collaborations. Many players are investing in the development of advanced drug formulations to improve efficacy and patient compliance. Expansion of generic drug portfolios is helping companies reach a broader patient base and enhance affordability. Strategic partnerships and licensing agreements enable access to new markets and technologies. Companies are also increasing their presence in emerging economies to capture untapped opportunities. In addition, efforts to streamline supply chains and improve manufacturing efficiency are supporting cost optimization. Emphasis on innovation, regulatory approvals, and patient-centric solutions continues to drive competitive advantage in the angina pectoris drugs market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Advancements in drug development

- 3.2.1.3 Increasing lifestyle-related risk factors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effects associated with the drugs

- 3.2.2.2 Growing adoption of minimally invasive surgeries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of biosimilar and generic offerings

- 3.2.3.2 Rising development of novel delivery systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.6 Pipeline analysis

- 3.7 Impact of AI and generative AI on the market

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Stable angina

- 5.3 Unstable angina

- 5.4 Microvascular angina

- 5.5 Prinzmetal angina

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Beta blockers

- 6.3 Nitrates

- 6.4 Anti-platelets

- 6.5 Calcium channel blockers

- 6.6 Anticoagulants

- 6.7 ACE inhibitors

- 6.8 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Bayer

- 10.5 Boehringer Ingelheim International

- 10.6 Cadila Pharmaceuticals

- 10.7 Eli Lilly and Company

- 10.8 Gilead Sciences

- 10.9 GlaxoSmithKline

- 10.10 Merck

- 10.11 Novartis

- 10.12 Otsuka Pharmaceutical

- 10.13 Pfizer

- 10.14 Sanofi

心絞痛治療市場-2026-2032年全球市場預測

心絞痛治療市場-2026-2032年全球市場預測 血管擴張劑市場規模、佔有率和成長分析:按藥物類別、適應症、劑型、分銷管道、最終用戶和地區分類-2026-2033年產業預測

血管擴張劑市場規模、佔有率和成長分析:按藥物類別、適應症、劑型、分銷管道、最終用戶和地區分類-2026-2033年產業預測 心絞痛治療市場規模、佔有率和成長分析:按藥物類別、類型、給藥途徑、通路和地區分類-2026-2033年產業預測

心絞痛治療市場規模、佔有率和成長分析:按藥物類別、類型、給藥途徑、通路和地區分類-2026-2033年產業預測 心絞痛治療市場:依療法、藥物類別、最終使用者和地區分類

心絞痛治療市場:依療法、藥物類別、最終使用者和地區分類 2026-2034年全球康尼斯症候群市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球康尼斯症候群市場規模、佔有率、趨勢和成長分析報告 心絞痛市場規模、佔有率和成長分析:按疾病類型、藥物類別、治療方法、最終用戶、分銷管道和地區分類-2026-2033年產業預測全球心絞痛治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

心絞痛市場規模、佔有率和成長分析:按疾病類型、藥物類別、治療方法、最終用戶、分銷管道和地區分類-2026-2033年產業預測全球心絞痛治療市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 心絞痛藥物市場規模、佔有率、趨勢分析報告:按類型、藥物類別、分銷管道、地區和細分市場預測,2024-2030

心絞痛藥物市場規模、佔有率、趨勢分析報告:按類型、藥物類別、分銷管道、地區和細分市場預測,2024-2030