|

市場調查報告書

商品編碼

2019076

關節內粘稠補充療法市場商機、成長要素、產業趨勢分析及 2026-2035 年預測。Viscosupplementation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

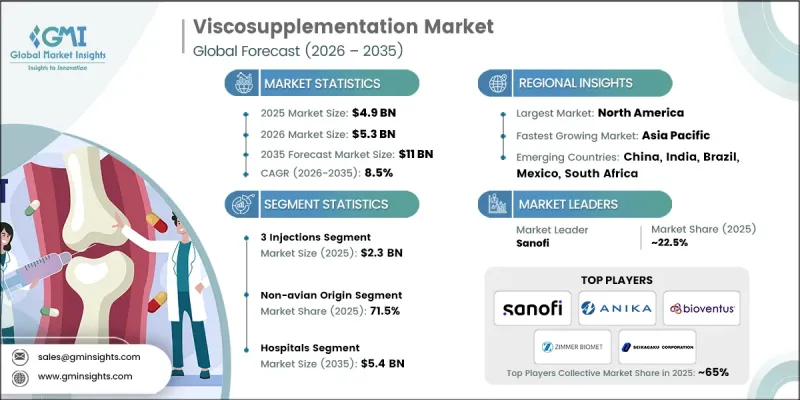

全球關節內粘稠補充療法市場預計到 2025 年將價值 49 億美元,預計到 2035 年將以 8.5% 的複合年成長率成長至 110 億美元。

關節內粘稠補充療法市場正經歷強勁成長,這主要得益於關節內注射玻尿酸療法的日益普及以及微創治療方法的興起。關節相關疾病的盛行率不斷上升,以及對有效非手術治療方法需求的日益成長,推動了這些療法的廣泛應用。透明質酸注射因其能夠改善關節功能、減輕不適並增強長期活動能力而備受關注。醫療專業人員擴大將這些療法作為保守治療策略的一部分,加速了其在全球的推廣。製劑技術的不斷進步以及人們對早期療育意識的提高,進一步促進了市場擴張。此外,醫療服務的可近性提高以及對以患者為中心的治療方案的日益重視,也促進了關節內粘稠補充療法的使用。綜合這些因素,預計該市場將在全部區域實現穩定、長期的成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 49億美元 |

| 預測金額 | 110億美元 |

| 複合年成長率 | 8.5% |

關節內粘稠補充療法是一種廣泛用於治療關節疾病的治療方法,其原理是將透明質酸注射到患處。這種治療方法有助於恢復關節潤滑、減少摩擦、緩解疼痛並改善整體活動能力。它被認為是手術介入的有效替代方案,並在整形外科和運動醫學領域中廣泛應用。隨著患者和醫療專業人員尋求在保持療效的同時縮短恢復時間和降低手術風險的解決方案,人們對微創治療方法的偏好日益成長,這持續推動著該治療方法的應用範圍不斷擴大。

預計到2035年,單劑量注射劑市場將以8.9%的複合年成長率成長,主要得益於其便捷的給藥方式和減少就診次數。患者遵守用藥的提高以及透明質酸製劑的進步(能夠以更少的劑量提供更持久的療效)也推動了該市場的成長。

預計到2025年,非禽源性產品將佔據71.5%的市場佔有率,到2035年市場規模將達到78億美元。此細分市場的成長主要得益於副作用風險較低、產品品質穩定以及患者和醫療專業人員的廣泛接受度等因素。這些優勢正推動其在各種治療領域中得到更廣泛的應用。

預計到2025年,北美關節內粘稠補充療法市場佔有率將達到42.1%,這主要得益於該地區關節疾病的高發生率和完善的醫療保健系統。該地區醫療費用支出、先進治療方法的普及以及主要市場參與企業的存在。人們對非手術治療方法的日益關注以及對微創手術需求的不斷成長,也進一步推動了該地區市場的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 老年人族群越來越容易患骨關節炎。

- 對微創治療的需求日益成長

- 運動相關傷害增加

- 產業潛在風險與挑戰

- 高昂的醫療費用

- 替代治療方法的可近性

- 市場機遇

- 開發先進的玻尿酸配方

- 擴建整形外科和運動醫學診所

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 技術趨勢(基於初步調查)

- 當前技術趨勢

- 新興技術

- 救贖方案

- 未來市場趨勢(基於初步研究)

- 管道分析

- 人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 1針

- 3針

- 5針

第6章 市場估計與預測:依產地分類,2022-2035年

- 鳥類起源

- 非鳥類起源

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 整形外科診所

- 門診手術中心(ASC)

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Anika Therapeutics

- APTISSEN

- Avanos Medical

- Biotech Healthcare

- Bioventus

- Ferring Pharmaceuticals

- Fidia Pharma

- IBSA Pharma

- Premier Surgical

- Sanofi

- Seikagaku Corporation

- Stellar Pharmaceuticals

- TRB Pharma

- Zimmer Biomet

The Global Viscosupplementation Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 11 billion by 2035.

The viscosupplementation market is experiencing strong growth, supported by the rising adoption of intra-articular hyaluronic acid therapies and a growing shift toward minimally invasive treatment approaches. The increasing prevalence of joint-related disorders and demand for effective non-surgical solutions are driving widespread acceptance of these therapies. Hyaluronic acid-based injections are gaining traction for their ability to improve joint function, reduce discomfort, and enhance mobility over a sustained period. Healthcare providers are increasingly recommending such procedures as part of conservative management strategies, which is accelerating global adoption. Continuous advancements in formulation technologies and growing awareness regarding early intervention are further strengthening market expansion. Additionally, improving healthcare access and rising focus on patient-centric treatment solutions are contributing to the increased utilization of viscosupplementation. These factors collectively position the market for steady long-term growth across developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $11 Billion |

| CAGR | 8.5% |

Viscosupplementation is widely used as a therapeutic approach for managing joint conditions through the administration of hyaluronic acid into affected areas. This treatment helps restore joint lubrication, minimize friction, relieve pain, and improve overall mobility. It is considered an effective alternative to surgical procedures and is extensively applied in orthopedic and sports medicine practices. The growing preference for less invasive treatment methods continues to support its increasing adoption, as patients and healthcare providers seek solutions that reduce recovery time and procedural risks while maintaining effectiveness.

The single injection segment is anticipated to grow at a CAGR of 8.9% through 2035, driven by its ease of administration and reduced need for multiple clinical visits. Improved patient adherence and advancements in hyaluronic acid formulations that deliver extended relief with fewer doses are contributing to the segment's growth.

The non-avian origin segment accounted for 71.5% share in 2025 and is expected to reach USD 7.8 billion by 2035. Growth in this segment is supported by factors such as lower risk of adverse reactions, consistent product quality, and broader acceptance among patients and healthcare providers. These advantages are driving increased adoption across various treatment settings.

North America Viscosupplementation Market held a share of 42.1% in 2025, supported by a high incidence of joint-related conditions and well-established healthcare systems. The region benefits from strong healthcare spending, access to advanced treatment options, and the presence of major market participants. Increasing awareness regarding non-surgical therapies and rising demand for minimally invasive procedures are further reinforcing regional growth.

Key players operating in the Global Viscosupplementation Market include Zimmer Biomet, Sanofi, Anika Therapeutics, Bioventus, Fidia Pharma, IBSA Pharma, Seikagaku Corporation, Avanos Medical, Ferring Pharmaceuticals, TRB Pharma, APTISSEN, Biotech Healthcare, Premier Surgical, and Stellar Pharmaceuticals. Companies in the Global Viscosupplementation Market are adopting a range of strategies to strengthen their competitive position and expand their global presence. Significant investments in research and development are enabling the introduction of advanced formulations with improved efficacy and longer-lasting outcomes. Market participants are focusing on expanding their product portfolios and enhancing manufacturing capabilities to meet growing demand. Strategic partnerships, collaborations, and distribution agreements are helping companies increase market penetration and geographic reach. Additionally, firms are emphasizing regulatory approvals and quality compliance to ensure product reliability. Continuous innovation, along with efforts to improve patient convenience and treatment outcomes, is supporting sustained growth and reinforcing their foothold in the global viscosupplementation industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Source of origin trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 A growing geriatric population prone to osteoarthritis

- 3.2.1.2 Rising demand for minimally invasive treatments

- 3.2.1.3 Increasing sports-related injuries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Availability of alternative treatments

- 3.2.3 Market opportunities

- 3.2.3.1 Development of advanced hyaluronic acid formulations

- 3.2.3.2 Expansion of orthopedic and sports medicine clinics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends (Driven by Primary Research)

- 3.8 Pipeline analysis

- 3.9 Impact of AI on the market

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Single injection

- 5.3 3 injections

- 5.4 5 injections

Chapter 6 Market Estimates and Forecast, By Source of Origin, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Avian origin

- 6.3 Non-avian origin

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anika Therapeutics

- 9.2 APTISSEN

- 9.3 Avanos Medical

- 9.4 Biotech Healthcare

- 9.5 Bioventus

- 9.6 Ferring Pharmaceuticals

- 9.7 Fidia Pharma

- 9.8 IBSA Pharma

- 9.9 Premier Surgical

- 9.10 Sanofi

- 9.11 Seikagaku Corporation

- 9.12 Stellar Pharmaceuticals

- 9.13 TRB Pharma

- 9.14 Zimmer Biomet

關節內粘稠補充療法市場:按產品類型、應用領域、分銷管道和最終用戶分類的全球市場預測 – 2026-2032 年

關節內粘稠補充療法市場:按產品類型、應用領域、分銷管道和最終用戶分類的全球市場預測 – 2026-2032 年 全球關節內粘稠補充療法市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球關節內粘稠補充療法市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球玻尿酸注射療法市場報告黏性補充劑注射市場按產品類型、應用部位、患者年齡層、最終用戶和分銷管道分類-2026-2032年全球預測

2026年全球玻尿酸注射療法市場報告黏性補充劑注射市場按產品類型、應用部位、患者年齡層、最終用戶和分銷管道分類-2026-2032年全球預測 關節內粘稠補充療法市場規模、佔有率和成長分析(按產品、應用、原料、最終用戶和地區分類)-2026-2033年產業預測

關節內粘稠補充療法市場規模、佔有率和成長分析(按產品、應用、原料、最終用戶和地區分類)-2026-2033年產業預測 關節內粘稠補充療法市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場預測,2025 年至 2033 年

關節內粘稠補充療法市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場預測,2025 年至 2033 年 黏液補充劑市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、最終用途、地區和競爭情況細分,2020-2030 年預測)

黏液補充劑市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、最終用途、地區和競爭情況細分,2020-2030 年預測) 2025 年至 2033 年黏彈性補充劑市場按類型、年齡層、配銷通路、應用、最終用途和地區分類

2025 年至 2033 年黏彈性補充劑市場按類型、年齡層、配銷通路、應用、最終用途和地區分類 關節內黏性補充療法市場:依劑量、關節炎類型、最終用戶和地區

關節內黏性補充療法市場:依劑量、關節炎類型、最終用戶和地區 2030 年關節內粘稠補充療法市場預測:按產品類型、來源、分銷管道、應用和地區進行全球分析

2030 年關節內粘稠補充療法市場預測:按產品類型、來源、分銷管道、應用和地區進行全球分析