|

市場調查報告書

商品編碼

2019073

抗病毒藥物市場機會、成長要素、產業趨勢分析及2026-2035年預測。Antiviral Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

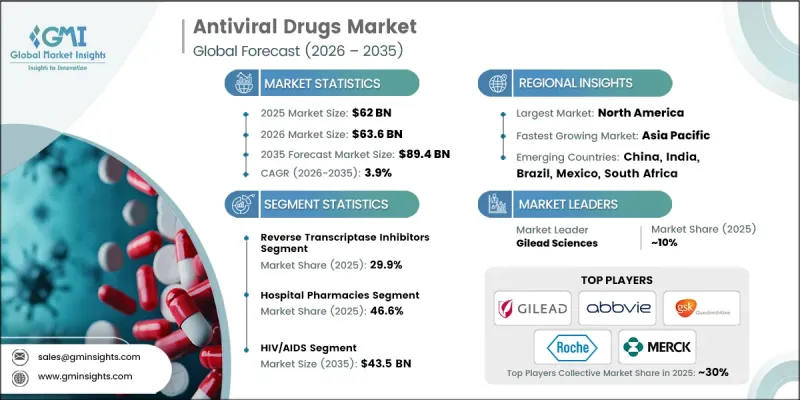

2025 年全球抗病毒藥物市場規模預計為 620 億美元,預計到 2035 年將達到 894 億美元,年複合成長率為 3.9%。

隨著對有效治療方法病毒感染疾病的需求持續成長,抗病毒藥物市場正穩步發展。抗病毒藥物旨在抑制病毒複製和增殖,在減輕疾病嚴重程度和縮短病程方面發揮至關重要的作用,並在某些情況下可用於預防。公眾意識的提高,以及政府為加速藥物核准、資助臨床研究和促進公共衛生教育所採取的利多舉措,都推動了市場擴張。全球病毒感染疾病負擔的加重和藥物研發的持續進步進一步增強了市場成長前景。藥物研發技術的進步和對創新治療方法投入的增加,正在改善治療效果和提高藥物可及性。此外,公營和私營機構所進行的宣傳活動也在促進先進治療方法的應用。製藥公司積極參與新型抗病毒治療方法的研發,也有助於擴大市場需求並提升長期市場潛力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 620億美元 |

| 預測金額 | 894億美元 |

| 複合年成長率 | 3.9% |

預計到2025年,逆轉錄酶抑制劑市佔率將達到29.9%,市場規模將達到186億美元。該細分市場的成長主要得益於對需要長期治療的病毒感染疾病有效療法的需求不斷成長。這些藥物在治療方法中發揮著至關重要的作用,透過提高生物利用度和療效,從而改善治療效果。政府加強支持力度和宣傳活動,進一步促進了這些藥物的應用,推動了該細分市場的持續成長。

品牌藥品市場在研發和臨床開發方面的強勁投入支撐下,預計到2025年將佔71.8%的市場佔有率。品牌抗病毒藥物因其在長期治療中展現的安全性、有效性和可靠性而廣受青睞。製藥公司將繼續致力於擴大這些治療方法的可及性,這將推動其廣泛應用並促進該細分市場的成長。

預計到2025年,北美抗病毒藥物市佔率將達到40.1%。這得歸功於先進的醫療基礎設施和對研發的大量投入。該地區之所以能夠保持主導地位,是因為其能夠及早採用創新療法,並且擁有大型製藥企業。治療方法的不斷進步以及對有效抗病毒療法日益成長的需求,正進一步推動該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 病毒感染疾病上升

- 愛滋病治療藥物上市數量增加。

- 對研發活動進行了大量投資,並且有在研發線產品。

- 老年人口增加

- 產業潛在風險與挑戰

- 新型抗菌素抗藥性

- 高昂的開發成本

- 市場機遇

- 擴大個人化抗病毒治療

- 擴大聯合治療和頻譜抗病毒療法的應用。

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 價格分析(基於初步調查)

- 管道分析

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依藥物類別分類,2022-2035年

- 逆轉錄酶抑制劑

- DNA聚合酵素抑制劑

- 蛋白酶抑制劑

- 神經氨酸酶抑制劑

- 其他藥物分類

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 愛滋病毒/愛滋病

- 肝炎

- 冠狀病毒感染疾病

- 單純皰疹病毒(HSV)

- 流感

- 其他跡象

第7章 市場估計與預測:依類型分類,2022-2035年

- 品牌商品

- 非專利的

第8章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 腸外

- 外用

- 其他給藥途徑

第9章 市場估計與預測:依年齡層別分類,2022-2035年

- 老年人

- 成人版

- 兒童

第10章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- AbbVie

- AstraZeneca

- Aurobindo Pharma

- Bristol-Myers Squibb

- Cipla

- Dr. Reddy's Laboratories

- F. Hoffmann-La Roche

- Gilead Sciences

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Sun Pharmaceutical

- Takeda Pharmaceutical

- Viatris

The Global Antiviral Drugs Market was valued at USD 62 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 89.4 billion by 2035.

The antiviral drugs market is gaining steady traction as the demand for effective therapies to manage viral infections continues to rise. Antiviral medications are designed to inhibit the growth and replication of viruses, playing a vital role in reducing disease severity and duration while also supporting preventive care in certain cases. Increasing awareness, along with favorable government initiatives aimed at accelerating drug approvals, funding clinical research, and promoting public health education, is supporting market expansion. The rising global burden of viral infections and continuous advancements in pharmaceutical research are further strengthening growth prospects. Technological progress in drug development and increasing investments in innovative therapies are enhancing treatment outcomes and accessibility. In addition, expanding awareness programs by public and private organizations are encouraging the adoption of advanced therapeutic options. The active involvement of pharmaceutical companies in developing new antiviral treatments is also contributing to the growing demand and long-term market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $62 Billion |

| Forecast Value | $89.4 Billion |

| CAGR | 3.9% |

The reverse transcriptase inhibitors segment accounted for 29.9% share and was valued at USD 18.6 billion in 2025. Growth in this segment is primarily driven by the increasing need for effective treatment solutions targeting viral infections that require long-term therapy. These drugs play a critical role in therapeutic regimens, offering improved treatment outcomes through enhanced bioavailability and effectiveness. Supportive government initiatives and increasing awareness programs are further boosting their adoption, contributing to sustained segment growth.

The branded segment held a share of 71.8% in 2025, supported by strong investments in research and clinical development. Branded antiviral drugs are widely preferred due to their proven safety, efficacy, and reliability in long-term treatment applications. Pharmaceutical companies continue to focus on expanding access to these therapies, which is driving their widespread adoption and reinforcing segment growth.

North America Antiviral Drugs Market accounted for 40.1% share in 2025, supported by advanced healthcare infrastructure and significant investment in research and development activities. The region continues to lead due to early adoption of innovative treatment solutions and the strong presence of major pharmaceutical companies. Continuous advancements in therapeutic development and increasing demand for effective antiviral treatments are further supporting regional growth.

Key players operating in the Global Antiviral Drugs Market include Pfizer, Merck, AbbVie, AstraZeneca, GlaxoSmithKline, Johnson & Johnson, Novartis, Gilead Sciences, Bristol-Myers Squibb, Takeda Pharmaceutical, Cipla, Dr. Reddy's Laboratories, Sun Pharmaceutical, Aurobindo Pharma, F. Hoffmann-La Roche, and Viatris. Companies in the Global Antiviral Drugs Market are focusing on strategic initiatives to strengthen their market position and expand their global footprint. Investments in research and development are enabling the introduction of advanced antiviral therapies with improved efficacy and safety profiles. Firms are actively pursuing partnerships, collaborations, and licensing agreements to accelerate drug development and commercialization. Expansion into emerging markets and strengthening distribution networks are also key priorities to enhance accessibility. Additionally, companies are focusing on regulatory approvals and innovation in drug formulations to remain competitive. Continuous efforts toward product differentiation and technological advancement are supporting long-term growth and reinforcing their presence across the global antiviral drugs industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Indication trends

- 2.2.4 Type trends

- 2.2.5 Route of administration trends

- 2.2.6 Age group trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of viral infections

- 3.2.1.2 Increasing number of product launches for HIV treatment

- 3.2.1.3 High investment in R&D activities and presence of pipeline products

- 3.2.1.4 Increasing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Emerging drug resistance

- 3.2.2.2 High development cost

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized antiviral therapies

- 3.2.3.2 Growing adoption of combination and broad spectrum antiviral regimens

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.6 Pipeline analysis

- 3.7 Future market trends (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plan

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Reverse transcriptase inhibitors

- 5.3 DNA polymerase inhibitors

- 5.4 Protease inhibitors

- 5.5 Neuraminidase inhibitors

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 HIV/AIDS

- 6.3 Hepatitis

- 6.4 Coronavirus infection

- 6.5 Herpes simplex virus (HSV)

- 6.6 Influenza

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generic

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Parenteral

- 8.4 Topical

- 8.5 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Geriatric

- 9.3 Adult

- 9.4 Pediatric

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacies

- 10.3 Retail pharmacies

- 10.4 Online pharmacies

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 AstraZeneca

- 12.3 Aurobindo Pharma

- 12.4 Bristol-Myers Squibb

- 12.5 Cipla

- 12.6 Dr. Reddy's Laboratories

- 12.7 F. Hoffmann-La Roche

- 12.8 Gilead Sciences

- 12.9 GlaxoSmithKline

- 12.10 Johnson & Johnson

- 12.11 Merck

- 12.12 Novartis

- 12.13 Pfizer

- 12.14 Sun Pharmaceutical

- 12.15 Takeda Pharmaceutical

- 12.16 Viatris

全球瑞德西韋市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球瑞德西韋市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 直接抗病毒藥物市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、適應症、給藥途徑、分銷管道、地區和競爭格局分類,2021-2031年瑞德西韋市場-全球產業規模、佔有率、趨勢、機會與預測:按劑型、給藥途徑、病患年齡、應用、分銷管道、地區和競爭格局分類,2021-2031年

直接抗病毒藥物市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、適應症、給藥途徑、分銷管道、地區和競爭格局分類,2021-2031年瑞德西韋市場-全球產業規模、佔有率、趨勢、機會與預測:按劑型、給藥途徑、病患年齡、應用、分銷管道、地區和競爭格局分類,2021-2031年 抗病毒療法市場:2026-2032年全球市場預測(依疾病、藥物分類、給藥途徑、治療方法及分銷管道分類)直接作用抗病毒藥物市場:依產品類型、治療領域、通路和最終用戶分類-2026-2032年全球市場預測抗病毒藥物市場:2026-2032年全球市場預測(依適應症、藥物類別、給藥途徑、最終用戶和分銷管道分類)

抗病毒療法市場:2026-2032年全球市場預測(依疾病、藥物分類、給藥途徑、治療方法及分銷管道分類)直接作用抗病毒藥物市場:依產品類型、治療領域、通路和最終用戶分類-2026-2032年全球市場預測抗病毒藥物市場:2026-2032年全球市場預測(依適應症、藥物類別、給藥途徑、最終用戶和分銷管道分類) 纈更昔洛韋市場規模、佔有率和成長分析:按產品類型、適應症、應用、患者類型、最終用戶、分銷管道和地區分類-2026-2033年產業預測

纈更昔洛韋市場規模、佔有率和成長分析:按產品類型、適應症、應用、患者類型、最終用戶、分銷管道和地區分類-2026-2033年產業預測 抗病毒藥物市場:依藥物類別、類型、應用、分銷管道和地區分類。

抗病毒藥物市場:依藥物類別、類型、應用、分銷管道和地區分類。 抗病毒藥物市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、劑型、成分、製程、功能及上市類型分類全球抗病毒藥物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

抗病毒藥物市場分析及預測(至2035年):依類型、產品類型、技術、應用、最終用戶、劑型、成分、製程、功能及上市類型分類全球抗病毒藥物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)