|

市場調查報告書

商品編碼

2019067

2026 年至 2035 年神經痛治療的市場機會、成長要素、產業趨勢與預測。Neuralgia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

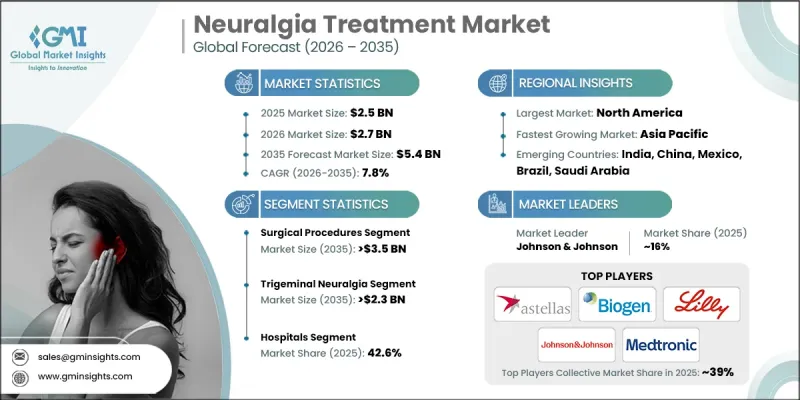

全球神經痛治療市場預計到 2025 年將價值 25 億美元,預計到 2035 年將以 7.8% 的複合年成長率成長至 54 億美元。

市場成長的促進因素包括神經系統疾病盛行率的上升、人們對神經病變疼痛的認知不斷提高以及診斷率的改善。神經痛的治療重點在於透過藥物、微創手術和生活方式調整來緩解神經相關疼痛。隨著世界人口老化,老年人更容易患上神經病變疼痛及其併發症,因此市場需求進一步成長。疼痛管理技術的進步,例如脊髓刺激設備和周邊神經刺激設備等神經調節設備,正在改變治療方案。射頻和脈衝串刺激技術在增強鎮痛效果的同時,最大限度地減少了副作用,而人工智慧驅動的程式設計則實現了個人化治療。微創手術的日益普及提高了患者的依從性和滿意度,從而推動了全球市場的強勁成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預測金額 | 54億美元 |

| 複合年成長率 | 7.8% |

神經痛的治療方法包括手術和非手術療法,旨在解決慢性神經痛問題。微創手術、先進的藥物療法和神經調節裝置能夠精準緩解疼痛並降低併發症風險。整合高解析度影像和神經傳導檢查等先進的診斷工具,可以製定個人化的治療方案,從而改善治療效果並提高整體治療效率。

預計到2035年,外科手術介入領域將以7.6%的複合年成長率成長,達到35億美元。微血管減壓手術和神經移植等先進手術針對潛在的神經壓迫或損傷,從而實現長期疼痛緩解。微創手術技術的應用將進一步推動該領域的成長,為患者提供有效的治療效果和更短的康復時間。

三叉神經痛市場預計將以8%的複合年成長率成長,到2035年市場規模將達到23億美元。作為最常見的神經痛類型之一,三叉神經痛嚴重影響患者的生活品質。雖然提高公眾意識的宣傳活動和早期診斷工作正在提高患者對治療的接受度,但先進的影像技術和個人化治療方案正在改善治療效果,並減少治療方法選擇中的試驗。

美國神經痛治療市場預計到2025年將達到11億美元,並在2035年之前以7.3%的複合年成長率成長。市場成長的促進因素包括:先進的醫療基礎設施、神經調控技術的廣泛應用、微創手術的普及、老齡化社會中神經病變疾病的高發生率以及有利的醫保報銷政策。大型製藥公司和醫療設備製造商的大量研發投入進一步鞏固了美國在該領域的主導地位。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 神經系統疾病盛行率增加

- 疼痛管理技術的進展

- 提高認知度和診斷率

- 產業潛在風險與挑戰

- 先進治療方法的高成本

- 市場機遇

- 生物技術進展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 客戶洞察(基於初步研究)

- 波特五力分析

- PESTEL 分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係與合作

- 引入新的治療方法

- 業務拓展計劃

第5章 市場估計與預測:依治療方法,2022-2035年

- 手術治療

- 射頻熱凝療法

- 立體定位放射放射線手術

- 顯微血管減壓手術

- 其他外科手術

- 藥物

- 抗驚厥藥物

- 抗憂鬱症

- 其他藥物

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 三叉神經痛

- 帶狀皰疹後遺症神經痛

- 枕神經痛

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 診所

- 門診手術中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- AA pharma

- astellas

- Biogen

- Eli Lilly

- Johnson & Johnson

- Medtronic

- NOVARTIS

- PACIRA

- Pfizer

- Siemens Healthineers

The Global Neuralgia Treatment Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 5.4 billion by 2035.

Market growth is driven by the rising incidence of neurological disorders, improved awareness of neuropathic conditions, and increasing diagnosis rates. Neuralgia treatments focus on alleviating nerve-related pain through medications, minimally invasive surgical procedures, and lifestyle modifications. The aging global population further fuels demand, as older adults are more susceptible to neuropathic pain and its complications. Technological advancements in pain management, such as neuromodulation devices including spinal cord and peripheral nerve stimulators, are transforming treatment options. High-frequency and burst stimulation technologies improve pain relief while minimizing side effects, and AI-driven programming allows for personalized therapy. The rise of minimally invasive interventions increases patient compliance and satisfaction, supporting robust market expansion worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.8% |

Neuralgia treatments encompass both surgical and non-surgical approaches aimed at addressing chronic nerve pain. Minimally invasive procedures, advanced pharmacological interventions, and neuromodulation devices provide targeted relief and reduce the risk of complications. The integration of precise diagnostic tools, such as high-resolution imaging and nerve conduction studies, enables tailored treatment plans, enhancing patient outcomes and improving overall therapeutic efficiency.

The surgical procedures segment is projected to grow at a CAGR of 7.6%, reaching USD 3.5 billion by 2035. Advanced interventions, including microvascular decompression and nerve grafting, target underlying nerve compression or damage, providing long-term pain relief. The adoption of minimally invasive surgical techniques further strengthens this segment, offering patients effective outcomes with reduced recovery times.

The trigeminal neuralgia segment is expected to grow at a CAGR of 8%, achieving a market value of USD 2.3 billion by 2035. As one of the most prevalent forms of neuralgia, it significantly impacts a patient's quality of life. Awareness campaigns and early diagnosis initiatives are enhancing treatment uptake, while personalized approaches guided by advanced imaging and diagnostics improve therapeutic results and reduce trial-and-error in care selection.

U.S. Neuralgia Treatment Market reached USD 1.1 billion in 2025 and is anticipated to grow at a CAGR of 7.3% through 2035. Market growth is supported by advanced medical infrastructure, widespread adoption of neuromodulation technologies, minimally invasive procedures, a high prevalence of neuropathic conditions among aging populations, and favorable reimbursement policies. Substantial R&D investments by major pharmaceutical and medical device companies further reinforce U.S. leadership in this sector.

Key players in the Global Neuralgia Treatment Market include Biogen, Eli Lilly, Johnson & Johnson, Novartis, Medtronic, Pfizer, PACIRA, Siemens Healthineers, AA Pharma, and Astellas. Companies in the Neuralgia Treatment Market are strengthening their presence by focusing on innovation and R&D to develop next-generation neuromodulation devices and surgical solutions. They are expanding partnerships with hospitals, research institutes, and clinics to enhance distribution and clinical adoption. Personalized treatment solutions, including AI-driven therapy programming, improve patient outcomes and satisfaction, differentiating companies in competitive markets. Firms also invest in educational initiatives for healthcare professionals, launch awareness campaigns to boost early diagnosis, and secure regulatory approvals to facilitate global market expansion. Strategic mergers, acquisitions, and collaborations further solidify their foothold while increasing geographic reach and product portfolio diversity.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Application

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neurological disorders

- 3.2.1.2 Advancements in pain management technologies

- 3.2.1.3 Increase in awareness and diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in biotechnology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.8 Customer insights (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New treatment type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical procedures

- 5.2.1 Radiofrequency thermal lesioning

- 5.2.2 Stereotactic radiosurgery

- 5.2.3 Microvascular decompression

- 5.2.4 Other surgical procedures

- 5.3 Medications

- 5.3.1 Anticonvulsants

- 5.3.2 Antidepressants

- 5.3.3 Other medications

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trigeminal neuralgia

- 6.3 Postherpetic neuralgia

- 6.4 Occipital neuralgia

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AA pharma

- 9.2 astellas

- 9.3 Biogen

- 9.4 Eli Lilly

- 9.5 Johnson & Johnson

- 9.6 Medtronic

- 9.7 NOVARTIS

- 9.8 PACIRA

- 9.9 Pfizer

- 9.10 Siemens Healthineers