|

市場調查報告書

商品編碼

2019063

小型堆高機市場機會、成長要素、產業趨勢分析及2026-2035年預測Small Forklift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

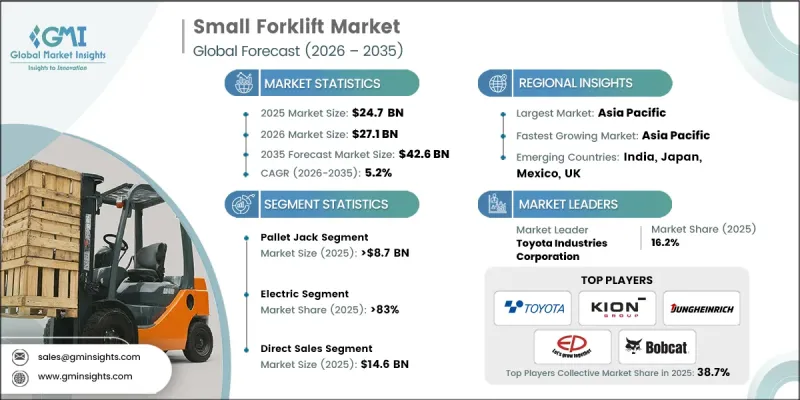

預計到 2025 年,全球小型堆高機市場價值將達到 247 億美元,並預計以 5.2% 的複合年成長率成長,到 2035 年達到 426 億美元。

受節能設備和環保營運需求不斷成長的推動,全球小型堆高機市場正在經歷轉型。企業正穩步轉向電池驅動堆高機,以減少排放氣體並改善職場環境,包括降低運作噪音。這種向電氣化的轉變正在加速傳統燃油設備的淘汰,並推動整體市場成長。同時,對緊湊型和多功能設備的需求不斷成長,也推動了物流和倉儲環境對小型堆高機的採用。電池技術和設備設計的持續創新,提高了性能並延長了運作週期。這些進步,加上有利的監管支持和永續性意識,正推動小型堆高機市場在多個工業領域持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 247億美元 |

| 預測金額 | 426億美元 |

| 複合年成長率 | 5.2% |

政策獎勵鼓勵採用先進設備,加上技術的不斷進步,進一步推動了小型堆高機市場的發展。領先的製造商正致力於提升電池性能、營運效率和以用戶為中心的設計,以滿足不斷變化的行業需求。同時,現代物流網路的擴張也推動了對緊湊高效、有助於提升營運效率的物料搬運設備的需求。這些因素,加上持續的創新和完善的法規結構,共同為市場的長期發展創造了有利條件。

預計到2025年,托盤搬運車市場規模將達到87億美元,反映出其在物料輸送作業中的廣泛應用。這些解決方案因其成本效益和人性化設計而備受青睞,有助於提高職場的生產效率。電動型號透過減輕體力消耗和實現更流暢的搬運流程,進一步提升了作業效率。托盤堆垛機高機在小型堆高機市場也佔據了相當大的佔有率,兼具靈活性和垂直搬運能力。對空間最佳化和高效物料搬運管理日益成長的需求,正在推動這些解決方案在現代化工廠中的應用。

預計到2025年,電動堆高機將佔據83%的市場佔有率,成為主要動力來源。電動堆高機日益受到青睞的原因在於其環保優勢、維修需求低以及適用於室內作業。由於運作安靜、排放氣體低、運作穩定性高,這些系統非常適合在受控環境中使用。隨著永續性成為關注的焦點,各行各業正擴大採用電動堆高機,以符合環保目標並提高整體效率。

到2025年,美國小型堆高機市場佔有率將達到83.9%。美國市場的主導地位得益於倉儲和物流基礎設施的快速擴張,以及物流和零售業需求的不斷成長。電動和先進堆高機系統的高普及率則主要歸功於永續發展舉措和自動化領域的投資。關鍵產業的持續現代化也促進了定期更新換代和持續的需求。此外,完善的分銷網路和靈活的資金籌措模式正在提升小型堆高機解決方案的可及性,從而推動了不同規模企業的廣泛應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 技術進步

- 消費者支出增加

- 可支配所得增加

- 產業潛在風險與挑戰

- 激烈的競爭與市場飽和

- 消費者偏好的變化

- 機會

- 混合協作和智慧工作空間整合快速擴展

- 拓展零售、飯店和公共空間的數位體驗基礎設施。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 組件和創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 顯示器和投影儀

- 音響設備

- 影像設備

- 控制面板和介面

- 電纜和連接基礎設施

- 軟體

- 控制和管理軟體

- 基於IP的影音平台

- 協作軟體

- 會議室預約軟體

- 遠距離診斷和監控工具

- 服務

- 諮詢和設計服務

- 安裝和設定服務

- 培訓和支援服務

- 託管服務和維護

- 系統升級和遷移服務

第6章 市場估算與預測:依解類型分類,2022-2035年

- 整合通訊與協作 (UC)

- 整合統一通訊平台

- 獨立協作工具

- 視訊會議解決方案

- 基於房間的系統

- 個人視訊會議終端

- 混合會議解決方案

- 數位電子看板

- 室內數位電子看板

- 戶外數位電子看板

- 互動數位電子看板

- 示範系統

- 基於預測的系統

- 基於顯示器的系統

- 無線演示解決方案

- 控制和自動化系統

- 集中控制平台

- 觸控面板介面

- 房間自動化解決方案

- 通報系統和緊急聯繫

- 校園範圍通知系統

- 建築緊急警報系統

- 綜合危機管理平台

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 公司

- 教育

- 政府/國防

- 衛生保健

- 零售和酒店

- 體育娛樂

- 運輸

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 大公司

- 中小企業

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Barco

- Biamp Systems

- Cisco Systems

- Crestron Electronics

- Extron Electronics

- Logitech

- Microsoft

- Panasonic

- Poly

- QSC Audio Products

- Samsung

- Shure Incorporated

- Sony Professional Solutions

- Zoom Video Communications

The Global Small Forklift Market was valued at USD 24.7 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 42.6 billion by 2035.

The global small forklift market is evolving in response to increasing demand for energy-efficient equipment and environmentally responsible operations. Organizations are steadily transitioning toward battery-powered forklifts to reduce emissions and improve workplace conditions, including minimizing operational noise. This shift toward electrification is accelerating the replacement of conventional fuel-based equipment, strengthening overall market growth. At the same time, rising demand for compact and versatile equipment is supporting adoption across logistics and warehousing environments. Continuous innovation in battery technologies and equipment design is enabling improved performance and longer operational cycles. These advancements, combined with favorable regulatory support and the growing emphasis on sustainability, are positioning the small forklift market for sustained growth across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.7 Billion |

| Forecast Value | $42.6 Billion |

| CAGR | 5.2% |

The small forklift market is further supported by policy incentives and ongoing technological improvements that encourage the adoption of advanced equipment. Leading manufacturers are focusing on enhancing battery performance, operational efficiency, and user-centric designs to meet evolving industry requirements. In parallel, the expansion of modern distribution networks is increasing the need for compact and highly efficient lifting equipment that can support streamlined operations. These factors, along with continuous innovation and supportive regulatory frameworks, are creating a favorable environment for long-term market development.

In 2025, the pallet jack segment reached USD 8.7 billion, reflecting its strong adoption across material handling operations. These solutions are widely preferred due to their cost efficiency and user-friendly design, which supports improved workplace productivity. Electric variants further enhance operational efficiency by reducing physical strain and enabling smoother handling processes. The pallet stacker segment also represents a significant portion of the small forklift market, offering a balance between mobility and vertical lifting capability. Increasing demand for space optimization and efficient load management is driving the adoption of these solutions across modern facilities.

The electric segment accounted for 83% share in 2025, establishing itself as the dominant power type. The growing preference for electric forklifts is driven by their environmental advantages, reduced maintenance requirements, and suitability for indoor operations. These systems offer quieter performance, lower emissions, and improved operational stability, making them highly suitable for controlled environments. As sustainability becomes a key focus area, industries are increasingly integrating electric forklifts into their operations to align with environmental goals and improve overall efficiency.

United States Small Forklift Market held an 83.9% share in 2025. The country's dominance is supported by rapid expansion in warehousing and distribution infrastructure, along with increasing demand from logistics and retail sectors. High adoption of electric and advanced forklift systems is being driven by sustainability initiatives and investments in automation. Ongoing modernization across key industries is also contributing to consistent replacement cycles and sustained demand. Additionally, strong distribution networks and flexible financing models are improving accessibility, enabling wider adoption of small forklift solutions across businesses of varying sizes.

Key companies operating in the Global Small Forklift Market include Anhui Heli Co., Ltd., BYD Forklift, Crown Equipment Corporation, Doosan Bobcat, EP Equipment, Godrej & Boyce, Hangcha Group Co., Ltd., Hyster-Yale, Inc., Hyundai Material Handling, Jungheinrich AG, KION Group AG, Komatsu, Lonking Machinery, Mitsubishi Logisnext Co., Ltd., and Toyota Industries Corporation. Companies in the Global Small Forklift Market are strengthening their competitive position through innovation, electrification, and strategic expansion initiatives. They are investing in advanced battery technologies, including lithium-ion systems, to improve energy efficiency and extend operating cycles. Product development efforts are focused on enhancing ergonomics, safety features, and automation capabilities to meet evolving user expectations. Strategic partnerships and distribution network expansion are helping companies increase market reach and improve customer access. Additionally, manufacturers are offering flexible financing and leasing options to attract a broader customer base. Integration of smart technologies such as telematics and predictive maintenance solutions is further enabling companies to deliver value-added services, improve operational efficiency, and strengthen long-term customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Solution Type

- 2.2.4 Application

- 2.2.5 End User

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Increasing consumer spending

- 3.2.1.3 Rising disposable income

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition and market saturation

- 3.2.2.2 Changing consumer preferences

- 3.2.3 Opportunities

- 3.2.3.1 Rapid growth of hybrid collaboration & smart workspace integrations

- 3.2.3.2 Expansion of digital experience infrastructure across retail, hospitality & public spaces

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Component and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 Gen AI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Component, 2022-2035 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Displays & projectors

- 5.2.2 Audio equipment

- 5.2.3 Video equipment

- 5.2.4 Control panels & interfaces

- 5.2.5 Cabling & connectivity infrastructure

- 5.3 Software

- 5.3.1 Control & management software

- 5.3.2 AV-over-IP platforms

- 5.3.3 Collaboration software

- 5.3.4 Room scheduling & booking software

- 5.3.5 Remote diagnostics & monitoring tools

- 5.4 Services

- 5.4.1 Consulting & design services

- 5.4.2 Installation & deployment services

- 5.4.3 Training & support services

- 5.4.4 Managed services & maintenance

- 5.4.5 System upgrade & migration services

Chapter 6 Market Estimates & Forecast, By Solution Type, 2022-2035 (USD Billion)

- 6.1 Key trends

- 6.2 Unified communications & collaboration (uc)

- 6.2.1 Integrated uc platforms

- 6.2.2 Standalone collaboration tools

- 6.3 Video conferencing solutions

- 6.3.1 Room-based systems

- 6.3.2 Personal video conferencing devices

- 6.3.3 Hybrid meeting solutions

- 6.4 Digital signage

- 6.4.1 Indoor digital signage

- 6.4.2 Outdoor digital signage

- 6.4.3 Interactive digital signage

- 6.5 Presentation systems

- 6.5.1 Projection-based systems

- 6.5.2 Display-based systems

- 6.5.3 Wireless presentation solutions

- 6.6 Control & automation systems

- 6.6.1 Centralized control platforms

- 6.6.2 Touch panel interfaces

- 6.6.3 Room automation solutions

- 6.7 Mass notification & emergency communication

- 6.7.1 Campus-wide notification systems

- 6.7.2 Building emergency alert systems

- 6.7.3 Integrated crisis management platforms

- 6.8 Other

Chapter 7 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion)

- 7.1 Key trends

- 7.2 Corporate

- 7.3 Education

- 7.4 Government & Defense

- 7.5 Healthcare

- 7.6 Retail & Hospitality

- 7.7 Sports & Entertainment

- 7.8 Transportation

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion)

- 8.1 Key trends

- 8.2 Large Enterprises

- 8.3 Small & Medium Businesses (SMBs)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Barco

- 10.2 Biamp Systems

- 10.3 Cisco Systems

- 10.4 Crestron Electronics

- 10.5 Extron Electronics

- 10.6 Google

- 10.7 Logitech

- 10.8 Microsoft

- 10.9 Panasonic

- 10.10 Poly

- 10.11 QSC Audio Products

- 10.12 Samsung

- 10.13 Shure Incorporated

- 10.14 Sony Professional Solutions

- 10.15 Zoom Video Communications

堆高機市場:全球市場預測,2026-2032年堆高機市場:2026-2032年全球市場預測(依產品類型、驅動系統、輪胎類型、操作方式、負載能力、提升高度、應用及最終用戶產業分類)

堆高機市場:全球市場預測,2026-2032年堆高機市場:2026-2032年全球市場預測(依產品類型、驅動系統、輪胎類型、操作方式、負載能力、提升高度、應用及最終用戶產業分類) 堆高機市場:依產品類型、等級、燃料類型、引擎類型、載重能力、最終用途產業和地區分類

堆高機市場:依產品類型、等級、燃料類型、引擎類型、載重能力、最終用途產業和地區分類 堆高機市場:市場規模、佔有率和趨勢分析(按等級、動力來源、負載容量、電池類型、應用和地區分類),細分市場預測(2026-2033 年)堆高機變速箱市場:依負載能力、動力來源及終端用戶產業分類-2026-2032年全球市場預測

堆高機市場:市場規模、佔有率和趨勢分析(按等級、動力來源、負載容量、電池類型、應用和地區分類),細分市場預測(2026-2033 年)堆高機變速箱市場:依負載能力、動力來源及終端用戶產業分類-2026-2032年全球市場預測 堆高機市場規模、佔有率、趨勢和預測:按產品類型、技術、等級、應用和地區分類,2026-2034年超窄巷道堆高機市場:依產品類型、負載能力、作業範圍類型、應用、最終用戶產業、通路分類,全球預測(2026-2032年)

堆高機市場規模、佔有率、趨勢和預測:按產品類型、技術、等級、應用和地區分類,2026-2034年超窄巷道堆高機市場:依產品類型、負載能力、作業範圍類型、應用、最終用戶產業、通路分類,全球預測(2026-2032年) 港口堆高機市場規模、佔有率和成長分析:按產品類型、載重能力、應用、最終用戶產業、分銷管道、地區和產業預測分類,2026-2033年

港口堆高機市場規模、佔有率和成長分析:按產品類型、載重能力、應用、最終用戶產業、分銷管道、地區和產業預測分類,2026-2033年 倉庫堆高機市場規模、佔有率和成長分析:按堆高機類型、載重能力、終端用戶產業、動力來源和地區分類-2026-2033年產業預測

倉庫堆高機市場規模、佔有率和成長分析:按堆高機類型、載重能力、終端用戶產業、動力來源和地區分類-2026-2033年產業預測 多向堆高機市場規模、佔有率和成長分析:按堆高機類型、燃料類型、載重能力、應用、終端用戶產業、地區和產業預測分類,2026-2033年

多向堆高機市場規模、佔有率和成長分析:按堆高機類型、燃料類型、載重能力、應用、終端用戶產業、地區和產業預測分類,2026-2033年