|

市場調查報告書

商品編碼

2019060

異丁酸市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Isobutyric Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

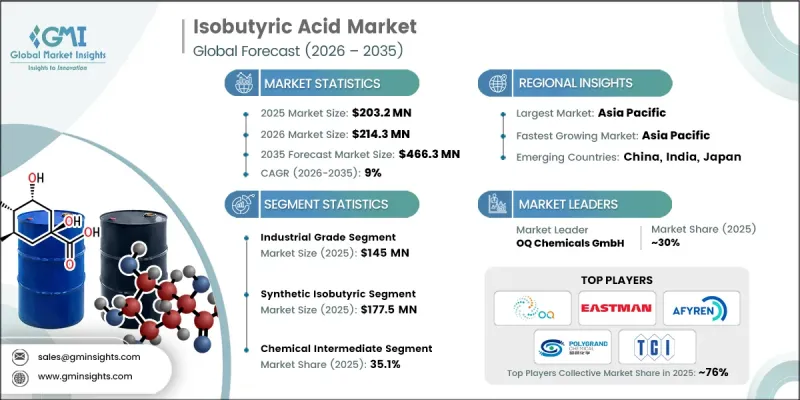

預計到 2025 年,全球異丁酸酯市場價值將達到 2.032 億美元,並預計以 9% 的複合年成長率成長,到 2035 年達到 4.663 億美元。

由於高純度異丁酸 (ISOB) 在各種工業製程中性能穩定,且與多種材料相容,因此其市場正在不斷擴大,成為尋求可靠化學解決方案的製造商的理想選擇。工業規模的生產和標準級產品的供應促進了其在化學、香料和橡膠添加劑行業的廣泛應用。同時,永續和生物基化學品生產的趨勢正在改變市場動態,推動可再生原料和更環保的生產方法的創新。監管壓力和消費者對環保解決方案的偏好也進一步推動了市場成長。此外,飼料產業在 ISOB 的應用方面發揮著至關重要的作用,它能夠改善牲畜的腸道環境和營養吸收,從而提高飼料轉換率。這進一步促進了人們對動物健康和生產力的日益關注,從而推動了市場需求的成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2.032億美元 |

| 預測金額 | 4.663億美元 |

| 複合年成長率 | 9% |

預計到2025年,工業級異丁酸市場規模將達到1.45億美元,並在2035年之前以9.5%的複合年成長率成長。工業級異丁酸是化學中間體、橡膠添加劑、香料和動物飼料等應用領域的重要原料。製造商重視該細分市場的成本效益、穩定的供應和一致的質量,使其適用於對純度要求不高的大批量工業應用。該細分市場受益於其與酯類生產的關聯性,並隨著特種化學品應用範圍的擴大和生物基生產方法的日益普及而持續成長。

預計到2025年,合成異丁酸(ISI)市場規模將達到1.775億美元,並在2026年至2035年間以9.2%的複合年成長率成長。合成生產主要採用石油化學方法,憑藉大規模的供給能力、成本效益和可靠的性能,仍然是商業供應的主要驅動力。眾多產業依賴該領域生產化學中間體、橡膠添加劑和香精酯。生產流程的持續最佳化提高了產量、營運效率和產品整體均勻性,從而鞏固了該領域在市場中的重要地位。

預計到2025年,北美異丁酸市場規模將達到4,620萬美元,並在整個預測期內保持強勁成長。該地區擁有完善的化學品生產基礎設施,推動了工業、香料和製藥領域對異丁酸的強勁需求。美國憑藉其特用化學品、食品香料和藥品的生產,佔據了大部分銷售額。穩定的產品品質、合規的監管以及高效率的供應鏈系統維持了市場的穩定。工業買家對生物基化學品和永續發展措施的日益重視,正在影響其籌資策略,並為環保異丁酸解決方案創造了機會。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依等級分類,2022-2035年

- 工業級

- 標準工業級

- 高純度工業級

- 試劑級

- 分析純試劑(AR等級)

- 實驗室試劑級

第6章 市場估計與預測:依類型分類,2022-2035年

- 合成異丁酸

- 以丙烯為原料的合成(Oxo基法)

- 異丁醛的氧化

- 其他合成路線

- 可再生異丁酸

- 生物基(發酵)

- 生質能衍生

第7章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 批發商和公司

- 線上/電子商務平台

第8章 市場估算與預測:最終用途,2022-2035年

- 化學中間體

- 酯類製造

- 塑化劑中間體

- 農藥中間體

- 聚合物添加劑

- 食品/調味料

- 增味劑

- 食品防腐劑

- 香料成分

- 飼料

- 飼料酸味劑

- 飼料防腐劑

- 生長促效劑

- 製藥

- 活性藥物成分(API)的中間體

- 添加劑和塗料

- 藥物輸送系統

- 其他

- 化妝品和個人護理

- 用於實驗和研究

- 工業用清潔劑

- 紡織加工

- 新興應用

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- AFYREN

- Eastman Chemical Company

- OQ Chemicals GmbH

- Central Drug House

- Tokyo Chemical Industry(TCI)

- Nanjing Chemical Material Corp

- Weifang Qiyi Chemical Co., Ltd.

- Shandong Luoheng Chemical Products Co., Ltd.

- Haihang Industry(GetChem Co., Ltd.)

The Global Isobutyric Acid Market was valued at USD 203.2 million in 2025 and is estimated to grow at a CAGR of 9% to reach USD 466.3 million by 2035.

The market is expanding as high-purity isobutyric acid ensures consistent performance across diverse industrial processes, while its compatibility with a wide range of materials makes it an attractive choice for manufacturers seeking reliable chemical solutions. Industrial-scale production and the availability of standard-grade products support broad adoption across chemical, flavor, and rubber additive sectors. Simultaneously, the trend toward sustainable and bio-based chemical production is reshaping market dynamics, encouraging innovations in renewable feedstocks and greener manufacturing methods. Regulatory pressures and consumer preference for environmentally responsible solutions further drive growth. The animal feed industry also plays a critical role, as isobutyric acid enhances gut health and nutrient absorption in livestock, boosting feed efficiency and contributing to the expanding demand from the growing focus on animal health and productivity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $203.2 Million |

| Forecast Value | $466.3 Million |

| CAGR | 9% |

The industrial grade segment reached USD 145 million in 2025 and is expected to grow at a CAGR of 9.5% through 2035. Industrial-grade isobutyric acid is essential for chemical intermediates, rubber additives, flavors, and animal nutrition applications. Manufacturers favor this segment for its cost-effectiveness, consistent supply, and stable quality, making it suitable for large-volume industrial use without the need for ultra-high purity. The segment benefits from its linkage to ester production and continues to gain traction as specialty chemical applications expand, and bio-based production methods are increasingly adopted.

The synthetic isobutyric acid segment was valued at USD 177.5 million in 2025 and is anticipated to grow at a CAGR of 9.2% from 2026 to 2035. Synthetic production, derived primarily from petrochemical methods, remains the mainstay for commercial supply due to its large-scale availability, cost-efficiency, and reliable performance. Industries depend on this segment to produce chemical intermediates, rubber additives, and flavor esters. Continued optimization of manufacturing processes enhances yields, operational efficiency, and overall product consistency, supporting the segment's sustained market relevance.

North America Isobutyric Acid Market accounted for USD 46.2 million in 2025 and is expected to witness robust growth over the forecast period. The region has a well-established chemical production infrastructure, fostering strong demand for isobutyric acid in industrial, flavoring, and pharmaceutical applications. The United States contributes a major share of revenue through specialized chemical, food flavoring, and pharmaceutical production. Market stability is maintained by consistent product quality, regulatory compliance, and efficient supply chain systems. Increasing adoption of bio-based chemicals and sustainability initiatives among industrial buyers is influencing procurement strategies, creating opportunities for eco-friendly isobutyric acid solutions.

Key players operating in the Global Isobutyric Acid Market include AFYREN, Eastman Chemical Company, OQ Chemicals GmbH, Central Drug House, Tokyo Chemical Industry (TCI), Nanjing Chemical Material Corp, Weifang Qiyi Chemical Co., Ltd., Shandong Luoheng Chemical Products Co., Ltd., Haihang Industry (GetChem Co., Ltd.), and others. Companies in the Global Isobutyric Acid Market strengthen their market position through a combination of innovation, sustainable product development, and strategic partnerships. Firms invest in R&D to improve production efficiency, purity, and yield, while also exploring bio-based feedstocks to meet environmental regulations and customer demand for sustainable chemicals. Partnerships with industrial end users ensure reliable supply chains and large-volume contracts. Companies expand geographic reach through mergers, acquisitions, and regional production facilities. Focusing on cost optimization, operational excellence, and eco-friendly production methods enhances competitiveness. Offering tailored solutions for animal feed, chemical intermediates, and flavor applications allows firms to capture diverse market segments and reinforce long-term presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Type

- 2.2.4 Distribution Channel

- 2.2.5 End-Use Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022- 2035 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Industrial Grade

- 5.2.1 Standard Industrial Grade

- 5.2.2 High-Purity Industrial Grade

- 5.3 Reagent Grade

- 5.3.1 Analytical Reagent (AR) Grade

- 5.3.2 Laboratory Reagent (LR) Grade

Chapter 6 Market Estimates and Forecast, By Type, 2022- 2035 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Synthetic Isobutyric Acid

- 6.2.1 Propylene-based Synthesis (Oxo Process)

- 6.2.2 Isobutyraldehyde Oxidation

- 6.2.3 Other Synthetic Routes

- 6.3 Renewable Isobutyric Acid

- 6.3.1 Bio-based (Fermentation)

- 6.3.2 Biomass-derived

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Direct Sales

- 7.3 Distributors & Traders

- 7.4 Online/E-commerce Platforms

Chapter 8 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical Intermediate

- 8.2.1 Ester Production

- 8.2.2 Plasticizer Intermediates

- 8.2.3 Agrochemical Intermediates

- 8.2.4 Polymer Additives

- 8.3 Food & Flavor

- 8.3.1 Flavor Enhancers

- 8.3.2 Food Preservatives

- 8.3.3 Fragrance Components

- 8.4 Animal Feed

- 8.4.1 Feed Acidifiers

- 8.4.2 Feed Preservatives

- 8.4.3 Growth Promoters

- 8.5 Pharmaceutical

- 8.5.1 Active Pharmaceutical Ingredient (API) Intermediates

- 8.5.2 Excipients & Coatings

- 8.5.3 Drug Delivery Systems

- 8.6 Others

- 8.6.1 Cosmetics & Personal Care

- 8.6.2 Laboratory & Research Use

- 8.6.3 Industrial Cleaning Agents

- 8.6.4 Textile Processing

- 8.6.5 Emerging Applications

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 AFYREN

- 10.2 Eastman Chemical Company

- 10.3 OQ Chemicals GmbH

- 10.4 Central Drug House

- 10.5 Tokyo Chemical Industry (TCI)

- 10.6 Nanjing Chemical Material Corp

- 10.7 Weifang Qiyi Chemical Co., Ltd.

- 10.8 Shandong Luoheng Chemical Products Co., Ltd.

- 10.9 Haihang Industry (GetChem Co., Ltd.)

異丁酸市場:2026-2032年全球市場預測(依原料、等級、形態、應用及通路分類)

異丁酸市場:2026-2032年全球市場預測(依原料、等級、形態、應用及通路分類) 異丁酸市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區分類的洞察,未來預測(2026-2034年)

異丁酸市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區分類的洞察,未來預測(2026-2034年) 異丁酸市場規模、佔有率和成長分析(按等級、類型、純度、最終用途和地區分類)-2026-2033年產業預測

異丁酸市場規模、佔有率和成長分析(按等級、類型、純度、最終用途和地區分類)-2026-2033年產業預測 全球異丁酸市場

全球異丁酸市場 2030 年異丁酸市場預測:按類型、等級、純度、最終用戶和地區進行的全球分析

2030 年異丁酸市場預測:按類型、等級、純度、最終用戶和地區進行的全球分析 異丁酸的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

異丁酸的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 異丁酸市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區、細分市場預測,2024-2030 年

異丁酸市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區、細分市場預測,2024-2030 年