|

市場調查報告書

商品編碼

2019059

靜脈輸液市場商機、成長要素、產業趨勢分析及2026-2035年預測。Intravenous Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

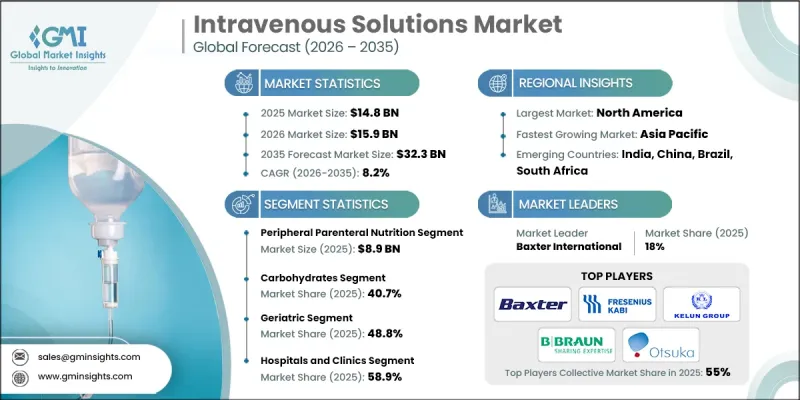

預計到 2025 年,全球靜脈輸液市場價值將達到 148 億美元,並有望以 8.2% 的複合年成長率成長,到 2035 年達到 323 億美元。

新興國家和已開發國家營養不良盛行率的上升以及對專業營養支持需求的增加,推動了該市場的成長。靜脈輸液,包括腸外營養(PN),在直接向血液中輸送必需營養素、體液和電解質方面發揮著至關重要的作用,尤其適用於無法口服或吸收營養的患者。醫護人員也更傾向於使用預混即用型靜脈輸液,這類輸液能夠提高病患安全性和操作效率,同時最大限度地降低污染和配製錯誤的風險,從而進一步刺激了市場需求。此外,製劑技術的進步以及人們對及時營養干預重要性的認知不斷提高,也促使醫院和診所在新生兒護理、重症監護、腫瘤科和慢性病管理等領域更多地採用靜脈輸液。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 148億美元 |

| 預測金額 | 323億美元 |

| 複合年成長率 | 8.2% |

預計到2025年,周邊靜脈營養(PPN)市場規模將達89億美元。 PPN廣泛用於需要短期營養支持的患者,透過周邊靜脈輸注胺基酸、葡萄糖和脂質等必需巨量營養素。這種療法有助於恢復營養平衡,防止營養素進一步流失,並改善口服或腸內攝取受限患者的營養缺乏。臨床研究表明,及時給予PPN可改善患者的預後和滿意度。 PPN的精確配方可確保患者以正確的比例獲得必需的微量營養素和宏量營養素,從而降低併發症風險,並在康復期間維持代謝穩定。醫院越來越依賴PPN製劑,將其作為一種安全有效的營養支持方式,用於重症監護和外科手術環境。

預計到2025年,碳水化合物類產品將佔據40.7%的市場佔有率,成為重要的市場貢獻因素。葡萄糖類靜脈輸液為無法透過口服或經腸營養獲得足夠熱量的患者提供必需的能量。這些輸液能夠滿足細胞能量需求,防止瘦體重流失,並維持重症患者和營養不良患者的代謝平衡。富含碳水化合物的靜脈輸液在加護病房、外科病房和新生兒護理中尤其重要,因為這些科室能量需求高,及時的營養支持至關重要。醫護人員更傾向於使用含葡萄糖的輸液,因為可以根據每位患者的個別需求進行精準輸注,這已成為現代腸外營養治療中不可或缺的一部分。

預計到2025年,北美靜脈輸液市場將佔據最大的市場佔有率。這主要得益於先進的醫療基礎設施、大量的手術以及在各種醫療機構中廣泛應用腸外營養和靜脈輸液療法。美國和加拿大的醫院、診所、門診中心以及不斷擴展的家庭醫療保健服務,都在持續推動靜脈輸液的需求。該地區受益於由美國FDA和加拿大衛生署主導的健全法規結構,該框架對無菌、標籤、品管和GMP(良好生產規範)合規性實施嚴格的標準。這些法規確保了病患安全、產品品質穩定以及可靠的供應鏈。此外,醫院採用先進技術、完善的臨床方案以及即用型預混合料靜脈輸液,正在提高營運效率,最大限度地減少臨床錯誤,並進一步鞏固北美在靜脈輸液市場的主導地位。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查過程和可靠性評分

- 調查過程的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 營養不良病例增加

- 早產發生率高

- 胃腸道疾病、神經系統疾病和癌症等疾病的發生率增加。

- 手術數量增加

- 產業潛在風險與挑戰

- 嚴格的規章制度和品質要求

- 市場機遇

- 居家和門診靜脈輸液護理正成為日益成長的趨勢。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 技術趨勢(基於初步調查)

- 目前技術

- 即用型 (RTU)預混合料溶液

- 個人化靜脈營養配方

- 新興技術

- 過渡到口服補液療法

- 多腔袋和自複合袋

- 目前技術

- 未來市場趨勢(基於初步研究)

- 專利分析(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響(基於初步研究)

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 全靜脈營養

- 周邊靜脈營養

第6章 市場估計與預測:依組成分類,2022-2035年

- 碳水化合物

- 維生素和礦物質

- 單劑量胺基酸

- 腸外脂肪乳劑

- 其他作品

第7章 市場估計與預測:依年齡層別分類,2022-2035年

- 兒童

- 成人

- 老年人

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 營養支持

- 輸血

- 體液和電解質平衡

- 其他用途

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院和診所

- 門診手術中心

- 居家照護設施

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Aculife Healthcare

- AdvaCare Pharma

- Albert David

- Amanta Healthcare

- Axa Parenterals

- B. Braun Melsungen

- Baxter International

- CSL

- Fresenius Kabi

- Grifols

- Haisco Pharmaceutical Group

- ICU Medical

- JW Life Science

- Kelun Industry Group

- Otsuka Pharmaceutical

The Global Intravenous Solutions Market was valued at USD 14.8 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 32.3 billion by 2035.

The market growth is fueled by the rising prevalence of malnutrition and an increasing need for specialized nutrition support across both emerging and developed regions. Intravenous solutions, including parenteral nutrition (PN), play a critical role in delivering essential nutrients, hydration, and electrolytes directly into the bloodstream, particularly for patients who cannot ingest or absorb nutrients orally. The demand is also driven by healthcare providers' preference for pre-mixed, ready-to-use IV solutions, which minimize the risks of contamination and preparation errors while enhancing patient safety and operational efficiency. In addition, advancements in formulation technology and increasing awareness of the importance of timely nutritional intervention have encouraged hospitals and clinics to adopt IV solutions for neonatal, critical care, oncology, and chronic disease management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.8 Billion |

| Forecast Value | $32.3 Billion |

| CAGR | 8.2% |

The peripheral parenteral nutrition (PPN) segment generated USD 8.9 billion in 2025. PPN is widely used for patients requiring short-term nutritional support, delivering vital macronutrients like amino acids, dextrose, and lipids through peripheral veins. The solution helps restore nutrient balance, prevent further nutritional depletion, and correct deficiencies in patients with limited oral or enteral intake. Clinical studies indicate that the timely administration of PPN improves patient outcomes and satisfaction. The precise formulation of PPN ensures that patients receive the necessary micromolecules and macromolecules in the right proportion, reducing the risk of complications and supporting metabolic stability during recovery periods. Hospitals increasingly rely on PPN solutions as a safe, efficient method to maintain nutritional support in critical care and surgical settings.

The carbohydrates segment accounted for 40.7% share in 2025, establishing the segment as a key contributor. Dextrose-based IV solutions provide essential energy for patients who cannot obtain adequate calories orally or through enteral feeding. These solutions support cellular energy requirements, prevent the breakdown of lean body mass, and maintain metabolic balance in critically ill and malnourished patients. The use of carbohydrate-enriched IV fluids is particularly critical in intensive care units, surgical wards, and neonatal care, where energy demands are high and timely nutrient delivery is essential. Clinicians favor dextrose-containing solutions because they can be accurately dosed to meet individual patient needs, making them indispensable in modern parenteral nutrition therapy.

North America Intravenous Solutions Market held the largest market share in 2025, driven by advanced healthcare infrastructure, high surgical procedure volumes, and widespread use of parenteral nutrition and IV fluid therapy across multiple care settings. Hospitals, clinics, ambulatory centers, and expanding home healthcare services in the U.S. and Canada have created sustained demand for intravenous solutions. The region benefits from a strong regulatory framework, led by the U.S. FDA and Health Canada, which enforces rigorous standards for sterility, labeling, quality control, and GMP compliance. These regulations ensure patient safety, consistent product quality, and reliable supply chains. Additionally, technological adoption in hospitals, advanced clinical protocols, and integration of ready-to-use pre-mixed IV solutions enhance operational efficiency and minimize clinical errors, further consolidating North America's dominance in the intravenous solutions market.

Key players operating in the Global Intravenous Solutions Market include Baxter International, B. Braun Melsungen, Fresenius Kabi, Grifols, ICU Medical, AdvaCare Pharma, JW Life Science, Otsuka Pharmaceutical, Aculife Healthcare, Amanta Healthcare, Albert David, Axa Parenterals, and Haisco Pharmaceutical Group. Companies in the Intravenous Solutions Market strengthen their presence by focusing on developing pre-mixed, ready-to-use formulations that reduce contamination risk and enhance operational efficiency. They invest in advanced manufacturing technologies to improve sterility, stability, and shelf life. Strategic collaborations with hospitals, clinics, and home healthcare providers help expand distribution networks and increase product adoption. Market leaders also prioritize regulatory compliance, leveraging certifications from U.S. FDA, Health Canada, and other authorities to build trust and maintain quality standards. Additionally, companies emphasize product innovation, offering customized nutrient compositions tailored for neonatal, critical care, and oncology patients.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.3 Type trends

- 2.4 Compositions trends

- 2.5 Age group trends

- 2.6 Application trends

- 2.7 End use trends

- 2.8 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing cases of malnutrition

- 3.2.1.2 High prevalence of pre-term births

- 3.2.1.3 Increasing prevalence of diseases, such as gastrointestinal disorder, neurological diseases, and cancer

- 3.2.1.4 Increasing number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory and quality requirements

- 3.2.3 Market opportunity

- 3.2.3.1 Rising shift toward home-based and outpatient infusion care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Ready-to-use (RTU) premixed solutions

- 3.5.1.2 Personalized IV nutrition formulations

- 3.5.2 Emerging technologies

- 3.5.2.1 Shift toward oral rehydration therapy

- 3.5.2.2 Multi-chamber and self-compounding bags

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Total parenteral nutrition

- 5.3 Peripheral parenteral nutrition

Chapter 6 Market Estimates and Forecast, By Composition, 2022 - 2035 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Carbohydrates

- 6.3 Vitamins and minerals

- 6.4 Single-dose amino acids

- 6.5 Parenteral lipid emulsion

- 6.6 Other compositions

Chapter 7 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

- 7.4 Geriatric

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Nutritional support

- 8.3 Blood transfusion

- 8.4 Fluid and electrolyte balance

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgery centers

- 9.4 Home care settings

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aculife Healthcare

- 11.2 AdvaCare Pharma

- 11.3 Albert David

- 11.4 Amanta Healthcare

- 11.5 Axa Parenterals

- 11.6 B. Braun Melsungen

- 11.7 Baxter International

- 11.8 CSL

- 11.9 Fresenius Kabi

- 11.10 Grifols

- 11.11 Haisco Pharmaceutical Group

- 11.12 ICU Medical

- 11.13 JW Life Science

- 11.14 Kelun Industry Group

- 11.15 Otsuka Pharmaceutical

北美靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分和細分市場預測(2026-2033 年)

北美靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分和細分市場預測(2026-2033 年) 靜脈注射市場:按產品類型、包裝類型、分銷管道、應用和最終用戶分類的全球市場預測 – 2026-2032 年

靜脈注射市場:按產品類型、包裝類型、分銷管道、應用和最終用戶分類的全球市場預測 – 2026-2032 年 靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年

靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年 全球靜脈輸液市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年

全球靜脈輸液市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年 靜脈輸液市場規模、佔有率和成長分析(按產品、營養成分和地區分類)—產業預測(2026-2033 年)靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分、最終用途、地區和細分市場預測(2026-2033 年)

靜脈輸液市場規模、佔有率和成長分析(按產品、營養成分和地區分類)—產業預測(2026-2033 年)靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分、最終用途、地區和細分市場預測(2026-2033 年) 林格氏液:2025-2031年全球市佔率與排名、總收入與需求預測

林格氏液:2025-2031年全球市佔率與排名、總收入與需求預測 全球藥用級氯化鉀市場:依通路、應用和地區(~2035年)美國靜脈注射注射液市場規模、佔有率、趨勢分析報告:按產品、營養、最終用途、細分市場預測,2025-2030 年

全球藥用級氯化鉀市場:依通路、應用和地區(~2035年)美國靜脈注射注射液市場規模、佔有率、趨勢分析報告:按產品、營養、最終用途、細分市場預測,2025-2030 年