|

市場調查報告書

商品編碼

2019051

伴侶動物用藥品市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Companion Animal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

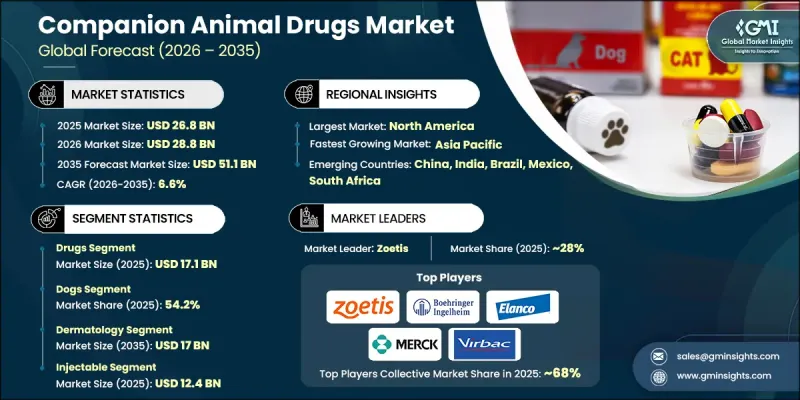

全球伴侶動物用藥品市場預計到 2025 年將達到 268 億美元,預計到 2035 年將以 6.6% 的複合年成長率成長至 511 億美元。

寵物市場擴張的促進因素包括伴侶動物數量的增加、寵物慢性病和感染疾病的日益普遍,以及飼主越來越願意投資先進的獸醫護理。寵物飼主越來越將他們心愛的動物視為家庭成員,這推動了對預防性藥物、疫苗和專業治療的需求。獸醫保健基礎設施的擴張和公眾對寵物健康意識的提高也進一步促進了市場成長。關節炎、糖尿病、心血管疾病和寄生蟲感染疾病等慢性疾病在伴侶動物中很常見,凸顯了有效藥物的必要性。隨著獸醫醫院採用創新治療方案和預防保健方法,全球對伴侶動物用藥品的需求持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 268億美元 |

| 預測金額 | 511億美元 |

| 複合年成長率 | 6.6% |

伴侶動物用藥品包括用於預防、治療或控制寵物健康狀況的藥物、疫苗和藥用飼料添加劑。這些藥物對於治療慢性疾病、感染疾病和皮膚病,以及控制動物間傳染病的傳播至關重要。

預計到2025年,醫藥產業規模將達到171億美元,這主要得益於關節炎、癌症和皮膚病等慢性疾病和感染疾病病例的不斷增加。寵物「人性化」趨勢的日益盛行,也進一步推動了對先進動物用藥品(包括抗生素、抗發炎藥和驅蟲藥)的投資,以改善動物福利。

預計到2035年,皮膚科市場規模將達到170億美元。包括過敏性皮膚炎、寄生蟲感染以及細菌或真菌性行為感染在內的皮膚疾病高發,推動了對皮膚病治療的需求。寵物容易受到環境過敏原、食物過敏和寄生蟲感染的影響,因此抗過敏藥、抗真菌藥物、抗生素和驅蟲藥是市面上必不可少的藥品類別。

預計到2025年,北美伴侶動物用藥品市佔率將達到42.9%,並在2035年之前以6.3%的複合年成長率成長。這一成長主要得益於寵物擁有率高、獸醫基礎設施完善以及寵物醫療保健方面的巨額支出。美國是該市場的主要貢獻者,這得益於寵物「人性化」的日益普及以及預防性和治療性療法的廣泛應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 伴侶動物數量不斷增加

- 動物疾病發生率上升

- 獸醫學進展

- 擴大獸醫保健基礎設施

- 產業潛在風險與挑戰

- 昂貴的動物用藥品和治療費用

- 發展中地區獲得獸醫服務的機會有限。

- 市場機遇

- 新型生技藥品和免疫療法的研發

- 獸藥電子商務的拓展

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 北美洲

- 研發管線/臨床試驗趨勢(基於初步調查)

- 價格分析(基於初步調查)

- 全國寵物數量統計(基於初步調查)

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 製藥

- 驅蟲

- 抗發炎藥

- 抗感染藥物

- 皮質類固醇

- 鎮靜劑

- 循環系統藥物

- 消化器官系統藥物

- 其他藥物

- 疫苗

- 活病毒疫苗(MLV)

- 去活化疫苗

- 重組疫苗

- 藥用飼料添加劑

- 抗生素

- 維他命

- 胺基酸

- 酵素

- 抗氧化劑

- 益生元和益生菌

- 礦物

- 其他藥用飼料添加劑

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 皮膚科

- 循環系統疾病

- 消化系統疾病

- 呼吸系統疾病

- 其他跡象

第7章 市場估計與預測:依動物類型分類,2022-2035年

- 狗

- 貓

- 馬

- 其他動物類型

第8章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

- 外用

- 其他給藥途徑

第9章 市場估價與預測:依通路分類,2022-2035年

- 獸藥

- 電子商務

- 零售藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 波蘭

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 台灣

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 海灣合作理事會國家

- 以色列

第11章:公司簡介

- Agrolabo

- Boehringer Ingelheim International

- Ceva Sante Animale

- Chanelle Pharma

- Dechra Pharmaceuticals

- Elanco Animal Health Incorporated

- Endovac Animal Health

- HIPRA

- Indian Immunologicals

- Merck

- Norbrook

- Symrise

- Vetoquinol

- Virbac

- Zoetis

The Global Companion Animal Drugs Market was valued at USD 26.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 51.1 billion by 2035.

The expansion is driven by the rising adoption of companion animals, an increasing prevalence of chronic and infectious diseases in pets, and the growing willingness of owners to invest in advanced veterinary care. Pet owners increasingly consider their animals as family members, fueling demand for preventive medications, vaccinations, and specialized treatments. The market growth is further supported by the expanding veterinary healthcare infrastructure and increased public awareness of pet health and wellness. Chronic conditions like arthritis, diabetes, cardiovascular disorders, and parasitic infections are common in companion animals, emphasizing the need for effective pharmaceuticals. As veterinary practices embrace innovative therapeutic solutions and preventive care approaches, the demand for companion animal drugs continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.8 Billion |

| Forecast Value | $51.1 Billion |

| CAGR | 6.6% |

Companion animal drugs include pharmaceuticals, vaccines, and medicated feed additives formulated to prevent, treat, or manage health conditions in pets. These drugs are essential in addressing chronic illnesses, infections, and dermatological conditions, as well as in controlling the spread of contagious diseases among animals.

In 2025, the drugs segment accounted for USD 17.1 billion, driven by increasing cases of chronic illnesses and infections such as arthritis, cancer, and skin conditions. The rising trend of pet humanization has further encouraged investment in advanced veterinary medicines, including antibiotics, anti-inflammatory agents, and parasiticides, to enhance animal well-being.

The dermatology segment is expected to reach USD 17 billion by 2035. High incidence of skin conditions, including allergic dermatitis, parasitic infestations, and bacterial or fungal infections, fuels demand for dermatological treatments. Pets are often susceptible to environmental allergens, food sensitivities, and parasites, which have made anti-allergy medications, antifungals, antibiotics, and parasiticides a vital category within the market.

North America Companion Animal Drugs Market held a 42.9% share in 2025 and is projected to grow at a CAGR of 6.3% through 2035. The regional growth is supported by high pet ownership, advanced veterinary infrastructure, and strong expenditure on pet healthcare. The U.S. contributes significantly to this market due to the rising humanization of pets and increased adoption of preventive and therapeutic treatments.

Key players in the Global Companion Animal Drugs Market include Boehringer Ingelheim International, Zoetis, Elanco Animal Health Incorporated, Vetoquinol, Ceva Sante Animale, Dechra Pharmaceuticals, HIPRA, Indian Immunologicals, Agrolabo, Chanelle Pharma, Endovac Animal Health, Merck, Symrise, Norbrook, and Virbac. Key strategies adopted by companies in the Global Companion Animal Drugs Market include investing heavily in research and development to create innovative and effective pharmaceuticals targeting specific diseases and preventive care solutions. Firms focus on expanding product portfolios across therapeutic areas such as dermatology, cardiology, and endocrinology to meet diverse pet healthcare needs. Partnerships with veterinary clinics, hospitals, and distributors help strengthen market reach and ensure the timely availability of products. Companies also emphasize regulatory compliance, quality assurance, and education programs for veterinarians to enhance adoption. Geographic expansion and targeted marketing campaigns are employed to build brand recognition and boost market share in emerging regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal type trends

- 2.2.4 Indication trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising companion animal population

- 3.2.1.2 Increasing prevalence of animal diseases

- 3.2.1.3 Advancements in veterinary pharmaceuticals

- 3.2.1.4 Expansion of veterinary healthcare infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary drugs and treatments

- 3.2.2.2 Limited access to veterinary services in developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of novel biologics and immunotherapies

- 3.2.3.2 Expansion of e-commerce veterinary pharmacies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Pipeline/clinical trial landscape (Driven by Primary Research)

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Pet population statistics, by country (Driven by Primary Research)

- 3.8 Future market trends

- 3.9 Impact of AI & generative AI on the market

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antiparasitic

- 5.2.2 Anti-inflammatory

- 5.2.3 Anti-infectives

- 5.2.4 Corticosteroids

- 5.2.5 Tranquilizers

- 5.2.6 Cardiovascular drugs

- 5.2.7 Gastrointestinal drugs

- 5.2.8 Other drugs

- 5.3 Vaccines

- 5.3.1 Modified live vaccines (MLV)

- 5.3.2 Killed inactivated vaccines

- 5.3.3 Recombinant vaccines

- 5.4 Medicated feed additives

- 5.4.1 Antibiotics

- 5.4.2 Vitamins

- 5.4.3 Amino acids

- 5.4.4 Enzymes

- 5.4.5 Antioxidants

- 5.4.6 Prebiotics and probiotics

- 5.4.7 Minerals

- 5.4.8 Other medicated feed additives

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dermatology

- 6.3 Cardiovascular diseases

- 6.4 Gastrointestinal diseases

- 6.5 Respiratory diseases

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Dogs

- 7.3 Cats

- 7.4 Horses

- 7.5 Other animal types

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Topical

- 8.5 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospital pharmacies

- 9.3 E-commerce

- 9.4 Retail pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Taiwan

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 GCC Countries

- 10.6.3 Israel

Chapter 11 Company Profiles

- 11.1 Agrolabo

- 11.2 Boehringer Ingelheim International

- 11.3 Ceva Sante Animale

- 11.4 Chanelle Pharma

- 11.5 Dechra Pharmaceuticals

- 11.6 Elanco Animal Health Incorporated

- 11.7 Endovac Animal Health

- 11.8 HIPRA

- 11.9 Indian Immunologicals

- 11.10 Merck

- 11.11 Norbrook

- 11.12 Symrise

- 11.13 Vetoquinol

- 11.14 Virbac

- 11.15 Zoetis

伴侶動物保健市場:2026-2032年全球市場預測(依動物種類、產品類型、劑型、通路和治療領域分類)

伴侶動物保健市場:2026-2032年全球市場預測(依動物種類、產品類型、劑型、通路和治療領域分類) 伴侶動物保健市場規模、佔有率和成長分析:按產品類型、動物種類、分銷管道、最終用戶和地區分類-2026-2033年產業預測

伴侶動物保健市場規模、佔有率和成長分析:按產品類型、動物種類、分銷管道、最終用戶和地區分類-2026-2033年產業預測 伴侶動物用藥品市場:依產品類型、通路和地區分類

伴侶動物用藥品市場:依產品類型、通路和地區分類 異噁唑啉類藥物市場報告:趨勢、預測及競爭分析(至2035年)

異噁唑啉類藥物市場報告:趨勢、預測及競爭分析(至2035年) 寵物保健產品市場規模、佔有率、趨勢和預測:按動物種類、產品類型、最終用戶和地區分類,2026-2034 年。

寵物保健產品市場規模、佔有率、趨勢和預測:按動物種類、產品類型、最終用戶和地區分類,2026-2034 年。 異寵及特殊寵物護理市場預測至2034年-按寵物類型、組件、應用、最終用戶和地區分類的全球分析

異寵及特殊寵物護理市場預測至2034年-按寵物類型、組件、應用、最終用戶和地區分類的全球分析 全球伴侶動物保健市場:市場規模、佔有率和趨勢分析(按動物、產品、分銷管道、最終用途和地區分類),基於細分市場的預測(2026-2033 年)

全球伴侶動物保健市場:市場規模、佔有率和趨勢分析(按動物、產品、分銷管道、最終用途和地區分類),基於細分市場的預測(2026-2033 年) 伴侶動物健康市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、解決方案、模式

伴侶動物健康市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、解決方案、模式 全球伴侶動物藥品市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球小型動物專科醫療保健市場:預測(至2034年)-依動物種類、專科醫療保健類型、服務類型、設施類型、最終使用者和地區進行分析

全球伴侶動物藥品市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球小型動物專科醫療保健市場:預測(至2034年)-依動物種類、專科醫療保健類型、服務類型、設施類型、最終使用者和地區進行分析