|

市場調查報告書

商品編碼

2019036

工業光電系統市場機會、成長要素、產業趨勢分析及2026-2035年預測Industrial Solar Power System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

預計到 2025 年,全球工業光伏系統市場規模將達到 3,684 億美元,並預計以 4.1% 的複合年成長率成長,到 2035 年達到 5,414 億美元。

企業正逐步重新思考其能源採購方式,日益重視太陽能解決方案,將其納入長期產業計畫,而非僅將其視為臨時性的永續發展措施。這種觀點轉變源於能源價格上漲、監管機構和企業為實現可再生能源目標而施加的日益成長的壓力,以及對穩定可靠的電力基礎設施不斷成長的需求。業內人士逐漸體認到,太陽能是一項策略性投資,既能提升財務效率,又能兼顧環境責任。因此,各行各業都在加速採用太陽能,以減少對傳統能源來源的依賴,同時確保可預測且經濟高效的發電。隨著企業將永續發展目標與營運效率相結合,並將太陽能定位為面向未來的產業生態系統的核心組成部分,市場正在持續擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 3684億美元 |

| 預測金額 | 5414億美元 |

| 複合年成長率 | 4.1% |

現代工業太陽能發電系統旨在與現有基礎設施無縫整合,並透過併網和混合配置提供柔軟性。這些高度適應性的系統可部署於各種工業環境。此外,儲能和先進能源管理解決方案的整合確保了穩定的電力供應。持續的技術進步,例如更高的面板效率和更強大的智慧監控能力,提高了系統可靠性,並最大限度地減少了因組件故障導致的運行停機時間。

預計到2025年,晶體矽光電技術市場規模將達3,026億美元。該領域憑藉其技術成熟度、成本效益和卓越的性能指標,持續引領市場。單晶矽和多晶矽組件均受惠於數十年的發展、大規模生產和完善的全球供應鏈網路。這些優勢體現在其可靠的性能和較長的使用壽命上,使其非常適用於對可靠性和投資回報率要求極高的工業應用。

到2025年,專用太陽能發電系統將佔54.1%的市場。其主導地位得益於其設計簡單、初始投資低以及久經考驗的高效性能。由於這些系統無需額外組件即可將陽光直接轉換為電能,因此安裝和維護成本可以保持在較低水平。強大的全球組件和逆變器供應鏈進一步保障了產品的供應和價格競爭力。除了能夠在用電高峰期帶來高收益外,其易於擴充性和與現有基礎設施的兼容性也推動了其廣泛應用。

北美工業太陽能發電系統市場佔80%的市場佔有率,預計2025年將達到1,217億美元。有利的政策框架、財政獎勵以及企業永續發展措施正在推動該地區的成長。工業領域正擴大採用太陽能解決方案來最佳化營運成本並減少排放。太陽能發電與儲能結合的系統也不斷普及,實現更有效率的能源管理和更高的電網穩定性。加拿大清潔能源政策及其對可再生能源發展的承諾,對加拿大該市場的發展產生了深遠的影響。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 人們對永續性和減碳的興趣日益濃厚

- 能源成本上漲及成本最佳化需求

- 太陽光電技術的進步與整合

- 產業潛在風險與挑戰

- 高昂的初始投資和資金籌措障礙

- 空間和基礎設施限制

- 機會

- 儲能及其與智慧電網的整合

- 政府獎勵和政策支持

- 促進因素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險及風險緩解分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依技術類型

- 監理情勢

- 標準和合規要求

- 認證標準

- 消費者購買行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依技術分類,2022-2035年

- 晶體矽太陽能電池

- 薄膜太陽能電池

- 船舶用太陽能熱能

- 其他

第6章 市場估計與預測:依系統配置分類,2022-2035年

- 太陽能發電系統

- 一種結合太陽能發電和儲能的混合系統。

第7章 市場估計與預測:依併網狀況分類,2022-2035年

- 併網連接

- 離網(獨立式)

第8章 市場估算與預測:依系統規模分類,2022-2035年

- 小規模工業用途

- 中型工業用途

- 大型工業/電力公司規模

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 重工業

- 流程工業

- 採礦和金屬

- 食品/飲料

- 紡織服裝

- 資料中心和IT

- 建材

- 紙漿和造紙

- 其他

第10章 市場估價與預測:依最終用途產業分類,2022-2035年

- 直銷

- 間接銷售

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 馬來西亞

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Longi Green Energy Technology Co., Ltd.

- Jinko Solar Holding Co., Ltd.

- JA Solar Technology Co., Ltd.

- Trina Solar Co., Ltd.

- Tongwei Solar Co., Ltd.

- Canadian Solar Inc.

- Aiko Solar

- First Solar, Inc.

- Huawei Technologies Co., Ltd.(Digital Power Business)

- Sungrow Power Supply Co., Ltd.

- SMA Solar Technology AG

- Fronius International GmbH

- GoodWe Technologies Co., Ltd.

- Nextracker Inc.

- Array Technologies, Inc.

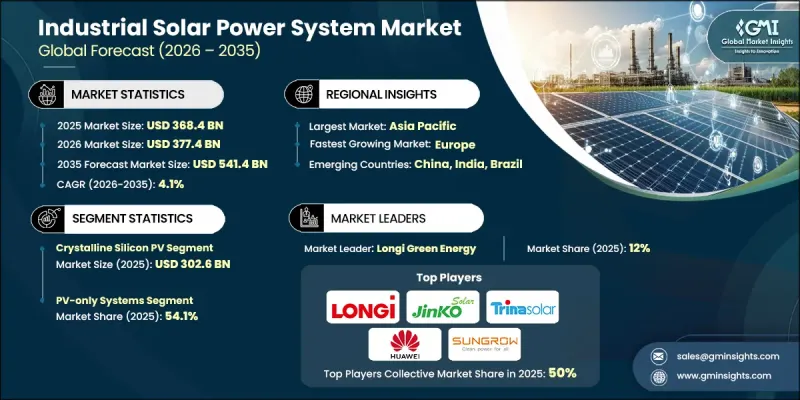

The Global Industrial Solar Power System Market was valued at USD 368.4 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 541.4 billion by 2035.

Companies are steadily redefining their approach to energy sourcing, increasingly prioritizing solar solutions as part of long-term operational planning rather than treating them as temporary sustainability measures. This evolving perspective is being shaped by escalating energy prices, mounting regulatory and corporate pressure to meet renewable energy targets, and the growing need for stable and resilient power infrastructure. Industrial players are recognizing solar energy as a strategic investment that supports both financial efficiency and environmental responsibility. As a result, adoption is accelerating across industries seeking to reduce dependence on conventional energy sources while ensuring predictable and cost-effective power generation. The market continues to expand as organizations align sustainability goals with operational efficiency, positioning solar energy as a central component of future-ready industrial ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $368.4 Billion |

| Forecast Value | $541.4 Billion |

| CAGR | 4.1% |

Modern industrial solar power systems are designed to integrate seamlessly with existing infrastructure, offering flexibility through grid-connected and hybrid configurations. These adaptable systems can be deployed across a wide range of industrial environments. In addition, the integration of energy storage and advanced energy management solutions ensures consistent power availability. Ongoing technological progress, including improvements in panel efficiency and intelligent monitoring capabilities, enhances system reliability and minimizes operational disruptions caused by component failures.

The crystalline silicon photovoltaic technology segment generated USD 302.6 billion in 2025. This segment continues to lead due to its technological maturity, cost efficiency, and strong performance metrics. Both monocrystalline and polycrystalline modules benefit from decades of development, large-scale manufacturing, and well-established global supply networks. These advantages translate into dependable performance and extended operational life, making them highly suitable for industrial applications where reliability and return on investment are critical considerations.

The PV-only systems segment accounted for 54.1% share in 2025. Its leadership is driven by its straightforward design, lower upfront investment, and proven efficiency. By directly converting sunlight into electricity without requiring additional components, these systems maintain reduced installation and maintenance costs. A robust global supply chain for modules and inverters further supports accessibility and competitive pricing. Their ability to deliver strong returns during peak energy demand periods, along with easy scalability and compatibility with existing infrastructure, reinforces their widespread adoption.

North America Industrial Solar Power System Market held an 80% share, generating USD 121.7 billion in 2025. Favorable policy frameworks, financial incentives, and corporate sustainability initiatives support growth in this region. Industrial sectors are increasingly deploying solar solutions to optimize operational costs and lower emissions. The adoption of combined solar and storage systems is also expanding, enabling efficient energy management and improved grid stability. Canada's progress in this market is largely influenced by its clean energy policies and commitment to renewable energy development.

Key participants in the Global Industrial Solar Power System Market include Longi Green Energy Technology Co., Ltd., Jinko Solar Holding Co., Ltd., JA Solar Technology Co., Ltd., Trina Solar Co., Ltd., Tongwei Solar Co., Ltd., Canadian Solar Inc., Aiko Solar, First Solar, Inc., Huawei Technologies Co., Ltd. (Digital Power Business), Sungrow Power Supply Co., Ltd., SMA Solar Technology AG, Fronius International GmbH, GoodWe Technologies Co., Ltd., Nextracker Inc., and Array Technologies, Inc. Companies operating in the Global Industrial Solar Power System Market are strengthening their positions through a combination of technological innovation, strategic partnerships, and global expansion initiatives. They are investing heavily in research and development to improve module efficiency, enhance durability, and integrate smart monitoring solutions. Many firms are also focusing on expanding their production capacities and optimizing supply chains to reduce costs and improve delivery timelines. Collaborations with industrial clients and energy solution providers are helping companies offer customized and scalable systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 System configuration

- 2.2.4 Grid connection status

- 2.2.5 System scale

- 2.2.6 End scale

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing focus on sustainability and carbon reduction

- 3.2.1.2 Rising energy costs and need for cost optimization

- 3.2.1.3 Advancements in solar technology and integration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and financing barriers

- 3.2.2.2 Space and infrastructure limitations

- 3.2.3 Opportunities

- 3.2.3.1 Integration with energy storage and smart grids

- 3.2.3.2 Government incentives and policy support

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 by technology type

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Consumer buying behaviour analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology Type, 2022-2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Crystalline silicon PV

- 5.3 Thin-film PV

- 5.4 Solar thermal (ship)

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By System Configuration, 2022-2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Pv-only systems

- 6.3 Hybrid pv+storage

Chapter 7 Market Estimates & Forecast, By Grid Connection Status, 2022-2035 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Grid-connected (on-grid)

- 7.3 Off-grid (standalone)

Chapter 8 Market Estimates & Forecast, By System Scale, 2022-2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Small industrial

- 8.3 Medium industrial

- 8.4 Large industrial/utility-scale

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022-2035 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 Heavy manufacturing

- 9.3 Process industries

- 9.4 Mining & metals

- 9.5 Food & beverage

- 9.6 Textiles & apparel

- 9.7 Data centers & IT

- 9.8 Building materials

- 9.9 Pulp & paper

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2022-2035 (USD Billion) (Tons)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Malaysia

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Longi Green Energy Technology Co., Ltd.

- 12.2 Jinko Solar Holding Co., Ltd.

- 12.3 JA Solar Technology Co., Ltd.

- 12.4 Trina Solar Co., Ltd.

- 12.5 Tongwei Solar Co., Ltd.

- 12.6 Canadian Solar Inc.

- 12.7 Aiko Solar

- 12.8 First Solar, Inc.

- 12.9 Huawei Technologies Co., Ltd. (Digital Power Business)

- 12.10 Sungrow Power Supply Co., Ltd.

- 12.11 SMA Solar Technology AG

- 12.12 Fronius International GmbH

- 12.13 GoodWe Technologies Co., Ltd.

- 12.14 Nextracker Inc.

- 12.15 Array Technologies, Inc.

商業和工業現場電源解決方案市場預測至2034年—按所有權類型、容量範圍、技術、應用、最終用戶和地區分類的全球分析

商業和工業現場電源解決方案市場預測至2034年—按所有權類型、容量範圍、技術、應用、最終用戶和地區分類的全球分析 全球電力系統分析軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球工業電力可靠性解決方案市場:預測(至2034年)-按解決方案類型、組件、電源、部署方式、技術、最終用戶和地區進行分析

全球電力系統分析軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球工業電力可靠性解決方案市場:預測(至2034年)-按解決方案類型、組件、電源、部署方式、技術、最終用戶和地區進行分析 工業電力系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依產品類型、輸出功率、垂直市場、地區及競爭格局分類,2021-2031年)

工業電力系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依產品類型、輸出功率、垂直市場、地區及競爭格局分類,2021-2031年) 全球工業電力系統市場

全球工業電力系統市場 工業電力系統銷售市場報告:2031 年趨勢、預測與競爭分析

工業電力系統銷售市場報告:2031 年趨勢、預測與競爭分析 電力系統分析軟體市場:按部署模型、應用程式和地區分類

電力系統分析軟體市場:按部署模型、應用程式和地區分類