|

市場調查報告書

商品編碼

2019023

鐵路煞車皮市場機會、成長要素、產業趨勢分析及2026-2035年預測。Railway Brake Pads Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

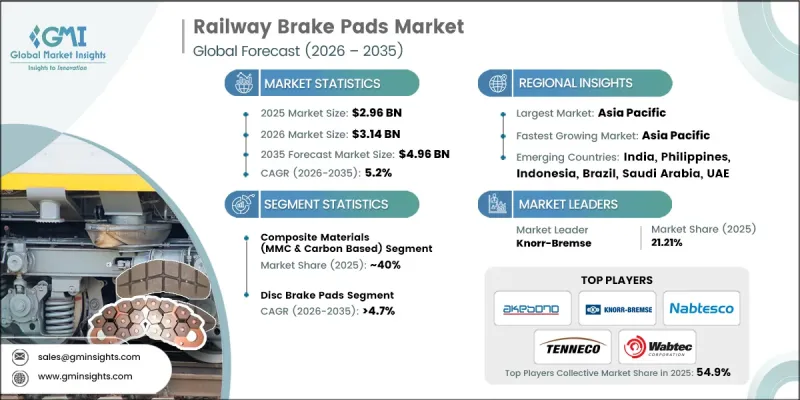

預計到 2025 年,全球鐵路煞車皮市場價值將達到 29.6 億美元,年複合成長率為 5.2%,到 2035 年將達到 49.6 億美元。

由於更嚴格的安全要求、更高的軸重和不斷提高的鐵路運輸密度,人們對煞車系統的期望也隨之改變,鐵路煞車皮產業正經歷重大變革時期。煞車皮不再被視為普通的替換零件,而是被視為關鍵的安全部件,直接影響煞車性能、車輪耐久性、噪音水平和合規性。隨著鐵路系統在更高速度和更大負載容量等更嚴苛的條件下持續運作,煞車零件的性能對於確保營運效率和長期資產保護至關重要。技術進步的重點在於提高耐久性、減少磨損並滿足更嚴格的環保要求。同時,隨著預測性維護和基於狀態的維護實踐的日益普及,煞車皮在生命週期管理中的重要性也日益凸顯。鐵路營運商正擴大利用性能數據和維護洞察來提高可靠性、減少停機時間並最佳化更換週期,從而進一步提升先進煞車解決方案在全球鐵路網路中的戰略價值。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 29.6億美元 |

| 預測金額 | 49.6億美元 |

| 複合年成長率 | 5.2% |

預計到2025年,複合材料(金屬基複合材料和碳基材料)市佔率將達到40%,並在2035年之前以4.9%的複合年成長率成長。這些材料因其高熱穩定性、低損耗率以及在高負荷運作環境下穩定的摩擦性能而廣受歡迎。它們即使在極端溫度下也能有效運作,並能最大限度地降低噪音和環境影響,這有助於滿足不斷變化的監管標準,並促進其在現代鐵路系統中的廣泛應用。

預計到2025年,碟式煞車皮片市佔率將達到60%,並在2026年至2035年間以4.7%的複合年成長率成長。該細分市場憑藉其卓越的煞車效率、運行可靠性和與先進車輛系統的兼容性,持續保持主導地位。碟式煞車皮能夠提供穩定、精準的煞車性能,尤其是在高速和重載工況下,同時還能降低振動和噪音。隨著鐵路營運商將安全性、成本效益和系統性能的提升置於優先地位,向更先進的煞車系統轉型的趨勢正在加速。

預計到2025年,北美鐵路煞車皮市佔率將達到32%,並在2035年之前以4.9%的複合年成長率成長。這一成長主要得益於完善的鐵路基礎設施、活躍的貨運以及鐵路車輛的持續使用。高運作頻率和頻繁的維護需求推動了對兼具耐用性和高性能的煞車皮的持續需求。此外,鐵路現代化和對城市交通系統的持續投資也促進了全部區域需求的穩定成長。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球客貨鐵路運輸量增加

- 加強鐵路安全和煞車性能方面的法規

- 高鐵和城市交通項目的激增

- 擴大預防性維護和狀態監測維護的採用範圍

- 產業潛在風險與挑戰

- 鐵路網利用率低下,更新周期長

- 價格敏感性和成本主導採購慣例

- 市場機遇

- 對低噪音、低排放煞車皮材料的需求日益成長

- 新興國家鐵路基礎建設投資快速成長

- 長期維護和生命週期服務合約增加

- 重型貨物運輸對高耐用煞車皮的需求增加。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國:《聯邦鐵路安全法》(FRSA)和聯邦鐵路管理局(FRA)煞車系統安全標準(49 CFR 第 232 部分)

- 歐洲

- 德國:鐵路建設和運營條例(EBO)

- 英國:鐵路及其他軌道運輸系統(安全)條例(ROGS)

- 法國:鐵路安全條例(Decret relatifala securiteferroviaire)

- 亞太地區

- 中國:中華人民共和國鐵路安全管理條例

- 日本:鐵路技術標準條例(國土交通省)

- 韓國:鐵路安全法

- 新加坡:快速交通系統法案

- 拉丁美洲

- 巴西:國家鐵路運輸安全法規 (ANTT)

- 墨西哥:鐵路服務管理法(ARTF)

- 智利:鐵路安全與營運條例(MTT)

- 中東和非洲(MEA)

- 阿拉伯聯合大公國:2020年第8號聯邦鐵路法案

- 沙烏地阿拉伯:鐵路安全法律規範(沙烏地阿拉伯鐵路安全局)

- 南非:《2002年鐵路安全條例》/波特分析

- 北美洲

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 生產統計

- 生產基地

- 消費者群體

- 出口和進口

- 價格分析

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響分析

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 未來前景與機遇

- 維護、修理和更換(MRO)週期分析

- 煞車皮壽命週期和磨損特性

- 按列車類型和運行條件分類的換乘間隔

- 預測性維護技術及其應用

- 成本分析:預防性維護與矯正性維護

- 庫存管理和準時制 (JIT) 實施

- 延壽方案及成本效益分析

- 數位化和智慧鐵路一體化的影響

- 基於物聯網的煞車皮狀態監測系統

- 即時磨損感測器技術

- 與列車管理系統 (TMS) 整合

- 用於預測性交易的巨量資料分析

- 數位雙胞胎在煞車系統最佳化的應用

- 區塊鏈輔助供應鏈可追溯性

- 工業4.0對製造業和分銷的影響

- 客戶購買行為與採購分析

- 鐵路營運商的採購流程和決策標準

- OEM與售後市場產品的採購決策因素

- 總擁有成本 (TCO) 評估框架

- 供應商資格認證和核准程序

- 長期供應合約和夥伴關係模式

- 大型鐵路項目的競標和招標分析

- 永續性和ESG標準對採購的影響

- 各地區採購政策的差異

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依材料分類,2022-2035年

- 有機/無石棉有機物 (NAO)

- 燒結金屬

- 半金屬

- 複合材料(MMC 和碳基材料)

- 其他

第6章 市場估算與預測:依產品分類,2022-2035年

- 碟式煞車皮

- 胎面煞車塊/煞車蹄

第7章 市場估算與預測:列車類型,2022-2035年

- 客運列車

- 貨車

- 地鐵/城市交通

- 輕軌/路面電車

- 機車

- 單軌列車

第8章 市場估算與預測:依銷售管道分類,2022-2035年

- OEM

- 售後市場

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Akebono Brake Industry

- Alstom

- CRRC

- DAKO-CZ

- Hitachi Rail.

- Knorr-Bremse

- Miba

- Nabtesco

- SGL Carbon

- Siemens Mobility

- Tenneco

- Wabtec

- 本地公司

- Brakes India Private

- Hindustan Composites

- Jurid Railway Solutions

- Railway Equipment Company(REC)

- SAB WABCO India

- Tenmat

- Tribo Rail Group

- TSE Brakes

- 新興企業

- Advanced Material Labs

- BrakeWear Analytics

- EcoBrake Systems

- GreenBrake Technologies

- Rail Friction Innovations

- Smart Rail Solutions

- TMD Friction

- Youcai

The Global Railway Brake Pads Market was valued at USD 2.96 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 4.96 billion by 2035.

The railway brake pads industry is undergoing a significant transformation as safety requirements, increasing axle loads, and rising rail traffic density reshape braking system expectations. Brake pads are no longer treated as standard replacement parts but are now engineered as critical safety components that directly affect stopping performance, wheel durability, acoustic output, and regulatory compliance. As rail systems continue to operate under more demanding conditions, including higher speeds and heavier freight loads, the performance of braking components has become essential to ensuring operational efficiency and long-term asset protection. Technological progress is focused on improving durability, reducing wear, and meeting stricter environmental requirements. At the same time, the growing adoption of predictive and condition-based maintenance practices is elevating the importance of brake pads in lifecycle management. Operators are increasingly relying on performance data and maintenance insights to improve reliability, reduce downtime, and optimize replacement cycles, reinforcing the strategic value of advanced braking solutions across global rail networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.96 Billion |

| Forecast Value | $4.96 Billion |

| CAGR | 5.2% |

The composite materials (MMC and carbon-based) segment held 40% share in 2025 and is projected to grow at a CAGR of 4.9% through 2035. These materials are widely preferred due to their enhanced thermal stability, reduced wear rates, and consistent friction performance under high-stress operating environments. Their ability to function effectively under extreme temperatures while minimizing noise and environmental impact supports compliance with evolving regulatory standards, driving their widespread use across modern rail systems.

The disc brake pads segment held a 60% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. This segment continues to lead due to its superior braking efficiency, operational reliability, and compatibility with advanced rolling stock systems. Disc brake pads deliver stable and precise braking performance, especially in high-speed and heavy-load conditions, while also reducing vibration and noise levels. The transition toward more advanced braking systems is accelerating as rail operators prioritize safety, cost efficiency, and improved system performance.

North America Railway Brake Pads Market held 32% share in 2025 and is anticipated to grow at a CAGR of 4.9% through 2035. The region's growth is supported by extensive rail infrastructure, high freight movement, and continuous utilization of rolling stock. Sustained demand for durable and high-performance brake pads is driven by operational intensity and the need for frequent maintenance cycles. Additionally, ongoing investments in rail modernization and urban transit systems are contributing to consistent demand growth across the region.

Key companies operating in the Global Railway Brake Pads Market include Alstom, Knorr-Bremse, Wabtec, Hitachi Rail, Siemens, Tenneco, Akebono Brake Industry, Nabtesco, SGL Carbon, and Miba. Companies in the Global Railway Brake Pads Market are strengthening their competitive position by focusing on product innovation, material advancement, and strategic expansion. They are investing in research and development to enhance braking efficiency, durability, and environmental performance. Manufacturers are also adopting advanced composite technologies to meet evolving regulatory and operational requirements. Strategic collaborations and long-term supply agreements with rail operators are helping companies secure consistent demand and expand their market presence. In addition, firms are leveraging digital solutions and predictive maintenance capabilities to improve product reliability and lifecycle performance. Expanding global production networks and optimizing supply chains are further enabling companies to meet rising demand while maintaining cost efficiency and operational scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Product

- 2.2.4 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global passenger and freight rail traffic volumes

- 3.2.1.2 Increase in railway safety and braking performance regulations

- 3.2.1.3 Surge in high-speed rail and urban transit projects

- 3.2.1.4 Rise in adoption of preventive and condition-based maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long replacement cycles in low-utilization rail networks

- 3.2.2.2 Price sensitivity and cost-driven procurement practices

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in demand for low-noise and low-emission brake pad materials

- 3.2.3.2 Surge in rail infrastructure investments in emerging economies

- 3.2.3.3 Increase in long-term maintenance and lifecycle service contracts

- 3.2.3.4 Rise in demand for high-durability brake pads for heavy-haul freight

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: Federal Railroad Safety Act (FRSA) & FRA Brake System Safety Standards (49 CFR Part 232)

- 3.4.2 Europe

- 3.4.2.1 Germany: Eisenbahn-Bau- und Betriebsordnung (EBO)

- 3.4.2.2 United Kingdom: Railways and Other Guided Transport Systems (Safety) Regulations (ROGS)

- 3.4.2.3 France: Railway Safety Decree (Decret relatif a la securite ferroviaire)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Railway Safety Management Regulations of the People’s Republic of China

- 3.4.3.2 Japan: Ministerial Ordinance on Technical Standards for Railways (MLIT)

- 3.4.3.3 South Korea: Railway Safety Act

- 3.4.3.4 Singapore: Rapid Transit Systems Act

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Railway Transport Safety Regulations (ANTT)

- 3.4.4.2 Mexico: Railway Service Regulatory Law (ARTF)

- 3.4.4.3 Chile: Railway Safety and Operations Regulations (MTT)

- 3.4.5 MEA

- 3.4.5.1 United Arab Emirates: Federal Railway Law No. 8 of 2020

- 3.4.5.2 Saudi Arabia: Railway Safety Regulatory Framework (Saudi Railway Safety Authority)

- 3.4.5.3 South Africa:Railway Safety Regulator Act, 2002Porter's analysis

- 3.4.1 North America

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing Analysis

- 3.9.1 By region

- 3.9.2 By Product

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Maintenance, repair & replacement cycle analysis

- 3.13.1 Brake pad lifecycle & wear characteristics

- 3.13.2 Replacement interval by train type & operating conditions

- 3.13.3 Predictive maintenance technologies & adoption

- 3.13.4 Cost analysis: preventive vs corrective maintenance

- 3.13.5 Inventory management & just-in-time practices

- 3.13.6 Extended life solutions & cost-benefit analysis

- 3.14 Digitalization & smart rail integration impact

- 3.14.1 Iot-enabled brake pad condition monitoring systems

- 3.14.2 Real-time wear sensor technologies

- 3.14.3 Integration with train management systems (tms)

- 3.14.4 Big data analytics for predictive replacement

- 3.14.5 Digital twin applications in brake system optimization

- 3.14.6 Blockchain for supply chain traceability

- 3.14.7 Impact of industry 4.0 on manufacturing & distribution

- 3.15 Customer buying behavior & procurement analysis

- 3.15.1 Railway operator procurement processes & decision criteria

- 3.15.2 Oem vs aftermarket purchase decision drivers

- 3.15.3 Total cost of ownership (tco) evaluation framework

- 3.15.4 Supplier qualification & approval procedures

- 3.15.5 Long-term supply agreements & partnership models

- 3.15.6 Tender & rfp analysis for major railway projects

- 3.15.7 Influence of sustainability & esg criteria on procurement

- 3.15.8 Regional procurement policy variations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Organic / Non-Asbestos Organic (NAO)

- 5.3 Sintered Metal

- 5.4 Semi-Metallic

- 5.5 Composite Materials (MMC & Carbon-Based)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Disc Brake Pads

- 6.3 Tread Brake Blocks / Shoes

Chapter 7 Market Estimates & Forecast, By Train Type, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Passenger Trains

- 7.3 Freight Trains

- 7.4 Metro / Urban Transit

- 7.5 Light Rail / Trams

- 7.6 Locomotives

- 7.7 Monorail

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Akebono Brake Industry

- 10.1.2 Alstom

- 10.1.3 CRRC

- 10.1.4 DAKO-CZ

- 10.1.5 Hitachi Rail.

- 10.1.6 Knorr-Bremse

- 10.1.7 Miba

- 10.1.8 Nabtesco

- 10.1.9 SGL Carbon

- 10.1.10 Siemens Mobility

- 10.1.11 Tenneco

- 10.1.12 Wabtec

- 10.2 Regional Players

- 10.2.1 Brakes India Private

- 10.2.2 Hindustan Composites

- 10.2.3 Jurid Railway Solutions

- 10.2.4 Railway Equipment Company (REC)

- 10.2.5 SAB WABCO India

- 10.2.6 Tenmat

- 10.2.7 Tribo Rail Group

- 10.2.8 TSE Brakes

- 10.3 Emerging Players

- 10.3.1 Advanced Material Labs

- 10.3.2 BrakeWear Analytics

- 10.3.3 EcoBrake Systems

- 10.3.4 GreenBrake Technologies

- 10.3.5 Rail Friction Innovations

- 10.3.6 Smart Rail Solutions

- 10.3.7 TMD Friction

- 10.3.8 Youcai

汽車煞車系統市場規模、佔有率和成長分析:按系統類型、組件、車輛類型、技術、銷售管道、最終用戶和地區分類-2026-2033年產業預測

汽車煞車系統市場規模、佔有率和成長分析:按系統類型、組件、車輛類型、技術、銷售管道、最終用戶和地區分類-2026-2033年產業預測 煞車系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、煞車皮材料類型、需求類別、車輛類型、地區和競爭格局分類,2021-2031年

煞車系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、煞車皮材料類型、需求類別、車輛類型、地區和競爭格局分類,2021-2031年 2026年全球鼓式煞車蹄片市場報告

2026年全球鼓式煞車蹄片市場報告 汽車煞車系統市場:按煞車類型、煞車技術、煞車零件、車輛類型、最終用戶和分銷管道分類-2026-2032年全球市場預測煞車系統及零件市場:2026-2032年全球市場預測(按零件類型、技術、推進系統、材料、車輛類型和銷售管道)

汽車煞車系統市場:按煞車類型、煞車技術、煞車零件、車輛類型、最終用戶和分銷管道分類-2026-2032年全球市場預測煞車系統及零件市場:2026-2032年全球市場預測(按零件類型、技術、推進系統、材料、車輛類型和銷售管道) 汽車煞車系統市場規模、佔有率、趨勢和預測:按類型、組件、技術、車輛類型、銷售管道和地區分類,2026-2034年越野車煞車系統市場:按車輛類型、煞車類型、材料、銷售管道和應用分類-2026-2032年全球市場預測煞車系統市場:2026-2032年全球市場預測(依產品類型、組件、驅動方式、車輛類型、最終用戶和銷售管道分類)2026年全球坡道起步輔助系統市場報告2026年全球汽車煞車系統市場報告

汽車煞車系統市場規模、佔有率、趨勢和預測:按類型、組件、技術、車輛類型、銷售管道和地區分類,2026-2034年越野車煞車系統市場:按車輛類型、煞車類型、材料、銷售管道和應用分類-2026-2032年全球市場預測煞車系統市場:2026-2032年全球市場預測(依產品類型、組件、驅動方式、車輛類型、最終用戶和銷售管道分類)2026年全球坡道起步輔助系統市場報告2026年全球汽車煞車系統市場報告