|

市場調查報告書

商品編碼

1998856

醫療包裝市場機會、成長要素、產業趨勢分析及2026-2035年預測Healthcare Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

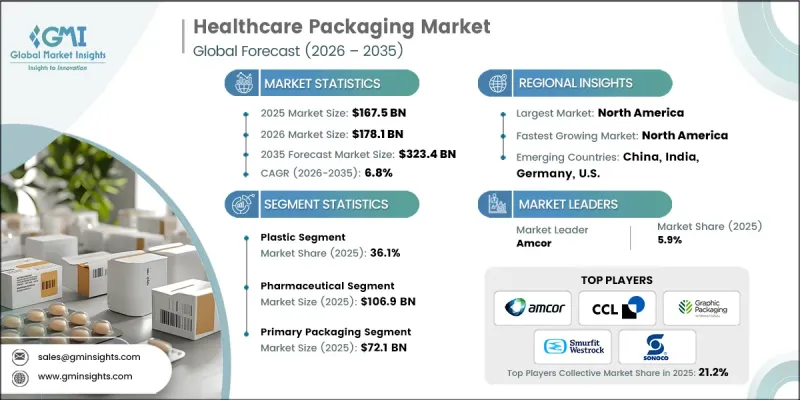

2025年全球醫療保健包裝市場價值為1,675億美元,預計到2035年將以6.8%的複合年成長率成長至3,234億美元。

全球醫藥和生技產業的擴張推動了對先進醫療保健包裝的需求成長,這些包裝能夠確保產品安全、無菌且防篡改。生物製藥、專科藥物和個人化醫療的日益普及,催生了對創新材料和設計的需求,這些材料和設計能夠增強產品完整性、延長保存期限並支持複雜的藥物輸送系統。更嚴格的監管要求和對病人安全的日益重視,正在加速合規包裝解決方案的普及。序列化、防偽措施和防篡改設計正逐漸成為業界標準。疫苗、溫敏藥物和生物製藥需求的成長也增加了對低溫運輸和保溫包裝解決方案的需求,迫使製造商開發既能滿足嚴格的熱穩定性要求,又能確保供應鏈安全和可追溯性的材料。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1675億美元 |

| 預計金額 | 3234億美元 |

| 複合年成長率 | 6.8% |

由於塑膠包裝輕巧、經濟高效且用途廣泛,預計2025年,塑膠包裝將佔據36.1%的市場佔有率。塑膠包裝具有耐用、防碎、防篡改、兒童安全鎖等優點,並且適用於預填充填充設計。其與多種藥品和生物製藥的兼容性使其成為醫院、藥房和居家醫療應用的首選。製造商不斷創新塑膠包裝,以確保符合監管要求、減少環境影響並滿足醫療保健機構不斷變化的需求。

預計到2025年,醫藥應用領域市場規模將達到1,069億美元,主要得益於全球藥品消費量的成長、處方處方箋數量的激增以及生物製藥生產的擴張。日益嚴格的監管合規要求促使製藥公司投資於配備兒童安全鎖的安全可靠的包裝解決方案。醫院、藥房和居家醫療市場對既能保護產品品質又能滿足安全性和營運效率要求的包裝的需求持續成長。

到2025年,北美醫療包裝市場將佔據38.5%的市場。該地區的成長主要得益於對無菌、兒童安全且防篡改包裝的需求不斷成長,以及生物製藥、生物相似藥和居家醫療服務的擴張。嚴格的監管以及先進的標籤、序列化和永續包裝解決方案的採用,進一步推動了市場成長。該地區的製造商致力於開發創新且合規的包裝系統,以滿足嚴格的安全和監管要求,同時兼顧環境問題。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 可回收和永續醫療包裝的創新

- 居家醫療和自我管理的發展趨勢。

- 提高對病人安全和合規包裝的認知

- 生物製藥和生物相似藥的成長需要先進的包裝解決方案。

- 慢性病盛行率的上升推動了對專用包裝解決方案的需求。

- 產業潛在風險與挑戰

- 新興生物製藥包裝開發面臨的挑戰

- 醫療包裝法規的區域差異

- 市場機遇

- 生技藥品和生物相似藥的擴張

- 居家醫療和自我管理的發展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 個人醫療包裝設備

- 塑膠

- 聚對苯二甲酸乙二醇酯(PET)

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚氯乙烯(PVC)

- 玻璃

- 紙張和紙板

- 金屬

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 初級包裝

- 瓶子罐

- 管瓶安瓿

- 泡殼包裝

- 預填充式注射器

- 小袋

- 管子

- 其他

- 二級包裝

- 紙箱

- 標籤和附加檔

- 托盤套

- 重疊和收縮包裝

- 其他

- 三級包裝

- 運輸貨櫃

- 調色盤

- 保護性包裝

- 散裝容器

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 製藥

- 口服藥物

- 注射藥物

- 外用/經皮

- 呼吸系統藥物

- 鼻腔藥物

- 其他

- 醫療設備

- 免洗耗材

- 治療設備

- 監測和診斷設備

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- 主要企業

- Amcor

- Aptar CSP Technologies

- CCL Industries

- Constantia Flexibles

- Gerresheimer

- Graphic Packaging

- Mayr-Melnhof Karton

- Schott Pharma

- Sonoco Products Company

- 按地區分類的主要企業

- 北美洲

- Cold Chain Technologies, LLC

- Nelipak

- Peli BioThermal LLC

- Smurfit WestRock

- 歐洲

- Sofrigam SA

- Korber AG

- August Faller GmbH &Co. KG

- 北美洲

- 特殊玩家/干擾者

- Schreiner Group

- Cryopak Industries Inc.

The Global Healthcare Packaging Market was valued at USD 167.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 323.4 billion by 2035.

The expansion of the global pharmaceutical and biotechnology sectors is driving the demand for advanced healthcare packaging that ensures product safety, sterility, and tamper evidence. The growing adoption of biologics, specialty drugs, and personalized medicine has created a need for innovative materials and designs that enhance product integrity, extend shelf life, and support complex drug delivery systems. Tighter regulatory requirements and heightened emphasis on patient safety are accelerating the adoption of compliant packaging solutions. Serialization, anti-counterfeiting measures, and tamper-evident designs are becoming standard across the industry. Rising demand for vaccines, temperature-sensitive medications, and biologics is also increasing the need for cold chain and insulated packaging solutions, compelling manufacturers to develop materials that meet strict thermal stability requirements while ensuring supply chain security and traceability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $167.5 Billion |

| Forecast Value | $323.4 Billion |

| CAGR | 6.8% |

The plastic segment held a 36.1% share in 2025, driven by its lightweight, cost-effective, and versatile properties. Plastic packaging offers durability, break resistance, and adaptability for tamper-proof, child-resistant, and pre-filled designs. Its compatibility with a wide range of pharmaceutical and biologic products makes it the preferred choice for hospitals, pharmacies, and home healthcare applications. Manufacturers continue to innovate plastic packaging to maintain compliance, reduce environmental impact, and meet the evolving demands of healthcare providers.

The pharmaceutical application segment reached USD 106.9 billion in 2025, due to the global increase in pharmaceutical consumption, high-volume prescriptions, and growing biologics production. Rising regulatory compliance requirements have prompted pharmaceutical companies to invest in safe, secure, and child-resistant packaging solutions. Hospitals, pharmacies, and home healthcare markets are driving continued demand for packaging that meets both safety and operational efficiency needs while protecting product quality.

North America Healthcare Packaging Market accounted for 38.5% share in 2025. The region's growth is fueled by increasing demand for sterile, child-resistant, and tamper-proof packaging, coupled with the expansion of biologics, biosimilars, and home healthcare services. Stringent regulations and the adoption of advanced labeling, serialization, and sustainable packaging solutions are further supporting market growth. Manufacturers in the region are focusing on developing innovative and compliant packaging systems that meet strict safety standards and regulatory requirements while also addressing environmental concerns.

Key players operating in the Global Healthcare Packaging Market include Amcor, Aptar CSP Technologies, August Faller GmbH & Co. KG, CCL Industries, Cold Chain Technologies LLC, Constantia Flexibles, Cryopak Industries Inc, Gerresheimer, Graphic Packaging, Korber AG, Mayr-Melnhof Karton, Nelipak, Peli BioThermal LLC, Schott Pharma, Schreiner Group, Smurfit WestRock, Sofrigam SA, and Sonoco Products Company. Key strategies employed by companies in the healthcare packaging market include investing in research and development to create innovative materials and packaging designs that meet regulatory compliance and enhance product protection. Firms are focusing on developing eco-friendly and sustainable solutions to align with global environmental initiatives. Strategic partnerships with pharmaceutical companies, cold chain providers, and logistics firms are being leveraged to expand distribution networks and improve supply chain efficiency. Companies are also adopting serialization, tamper-evident technologies, and anti-counterfeiting measures to strengthen brand trust and ensure compliance with international regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Innovation in recyclable and sustainable medical packaging

- 3.2.1.2 Expanding home healthcare and self-administration trends

- 3.2.1.3 Rising awareness about patient safety and compliance packaging

- 3.2.1.4 Growth in biologics and biosimilars requiring advanced packaging solutions

- 3.2.1.5 Rising prevalence of chronic diseases boosting demand for specialized packaging solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges in developing packaging for emerging biologic therapies

- 3.2.2.2 Regional disparities in healthcare packaging regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Biologics and Biosimilars

- 3.2.3.2 Growth in Home Healthcare and Self-Administration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete Healthcare Packaging devices

- 5.2.1 Plastic

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polyethylene (PE)

- 5.2.4 Polypropylene (PP)

- 5.2.5 Polyvinyl Chloride (PVC)

- 5.3 Glass

- 5.4 Paper & Paperboard

- 5.5 Metals

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Primary Packaging

- 6.2.1 Bottles & Jars

- 6.2.2 Vials & Ampoules

- 6.2.3 Blister Packs

- 6.2.4 Pre-filled Syringes

- 6.2.5 Pouches

- 6.2.6 Tubes

- 6.2.7 Others

- 6.3 Secondary Packaging

- 6.3.1 Cartons & Boxes

- 6.3.2 Labels & Inserts

- 6.3.3 Trays & Sleeves

- 6.3.4 Overwraps & Shrink Wraps

- 6.3.5 Others

- 6.4 Tertiary Packaging

- 6.4.1 Shipping containers

- 6.4.2 Pallets

- 6.4.3 Protective packaging

- 6.4.4 Bulk container

- 6.4.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Pharmaceuticals

- 7.2.1 Oral Drug

- 7.2.2 Injectable

- 7.2.3 Topical & Dermal Drug

- 7.2.4 Pulmonary Drug

- 7.2.5 Nasal Drugs

- 7.2.6 Others

- 7.3 Medical Device

- 7.3.1 Disposable Consumables

- 7.3.2 Therapeutic Equipment

- 7.3.3 Monitoring & Diagnostic Equipment

- 7.3.4 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Netherlands

- 8.3.8 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia-Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor

- 9.1.2 Aptar CSP Technologies

- 9.1.3 CCL Industries

- 9.1.4 Constantia Flexibles

- 9.1.5 Gerresheimer

- 9.1.6 Graphic Packaging

- 9.1.7 Mayr-Melnhof Karton

- 9.1.8 Schott Pharma

- 9.1.9 Sonoco Products Company

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Cold Chain Technologies, LLC

- 9.2.1.2 Nelipak

- 9.2.1.3 Peli BioThermal LLC

- 9.2.1.4 Smurfit WestRock

- 9.2.2 Europe

- 9.2.2.1 Sofrigam SA

- 9.2.2.2 Korber AG

- 9.2.2.3 August Faller GmbH & Co. KG

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Schreiner Group

- 9.3.2 Cryopak Industries Inc.

全球動物保健包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球動物保健包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 醫療包裝市場-2026-2032年全球市場預測

醫療包裝市場-2026-2032年全球市場預測 醫療保健包裝市場預測(2034 年)—按包裝類型、產品類型、材料、應用、最終用戶和地區分類的全球分析

醫療保健包裝市場預測(2034 年)—按包裝類型、產品類型、材料、應用、最終用戶和地區分類的全球分析 全球PCR包裝市場:預測至2031年醫藥鋁塑管包裝市場:2026-2032年全球市場預測(依材料、管材結構、容量範圍、產品配方類型、藥物類型、生產流程、最終用戶類型及治療應用分類)

全球PCR包裝市場:預測至2031年醫藥鋁塑管包裝市場:2026-2032年全球市場預測(依材料、管材結構、容量範圍、產品配方類型、藥物類型、生產流程、最終用戶類型及治療應用分類) 醫療保健包裝市場:全球產業趨勢、佔有率、規模、成長、機會與預測(2026-2034年)

醫療保健包裝市場:全球產業趨勢、佔有率、規模、成長、機會與預測(2026-2034年) 2026年全球塑膠醫療保健包裝市場報告2026年全球醫療保健包裝市場報告軟包裝鋁塑薄膜市場:依材料成分、包裝類型、厚度分類、印刷設計、應用和最終用途產業分類-全球預測(2026-2032)

2026年全球塑膠醫療保健包裝市場報告2026年全球醫療保健包裝市場報告軟包裝鋁塑薄膜市場:依材料成分、包裝類型、厚度分類、印刷設計、應用和最終用途產業分類-全球預測(2026-2032) 醫療保健包裝市場規模、佔有率和成長分析(按材料類型、包裝、包裝形式、應用和地區分類)-2026-2033年產業預測

醫療保健包裝市場規模、佔有率和成長分析(按材料類型、包裝、包裝形式、應用和地區分類)-2026-2033年產業預測