|

市場調查報告書

商品編碼

1998854

柑橘果膠市場機會、成長要素、產業趨勢分析及2026-2035年預測Citrus Pectin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

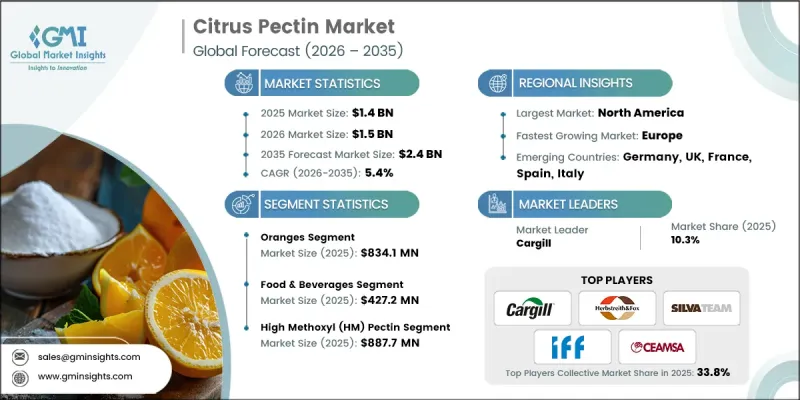

預計到 2025 年,全球柑橘果膠市場價值將達到 14 億美元,並有望以 5.4% 的複合年成長率成長,到 2035 年達到 24 億美元。

市場擴張的驅動力在於食品飲料、營養保健品和藥品領域對天然植物性成分日益成長的需求。柑橘果膠是一種主要從柑橘皮中提取的多醣,因其凝膠、增稠和穩定特性而備受青睞。其在配方中的多功能性使其能夠改善多種產品的質地、黏度和保存期限,同時支援低糖配方和潔淨標示概念。高甲氧基果膠 (HM) 在酸性和醣類條件下形成凝膠,而低甲氧基果膠 (LM) 則需要鈣離子才能形成凝膠,這使其在果醬、果凍、糖果、糖果甜點和機能性食品等應用中柔軟性。消費者對天然來源、非基因改造成分的偏好日益成長,以及對膳食健康益處的意識提升,正在擴大柑橘果膠的應用範圍,使其成為製造商滿足不斷變化的食品和營養補充劑需求的重要功能性成分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 14億美元 |

| 預測金額 | 24億美元 |

| 複合年成長率 | 5.4% |

預計2025年,橙皮果膠市場規模將達8.341億美元。這反映了橙皮果膠的多功能性和優異的性能。橙皮果膠因其天然的增稠、凝膠和穩定特性而被廣泛應用於食品工業,是改善食品質地和品質的關鍵成分。此外,其作為潔淨標示和非基因改造產品的優勢,也吸引了注重健康的消費者,他們追求天然成分和最少的加工。

到2025年,經銷商和批發通路的市場規模將達到5.789億美元。這些管道對於觸達食品製造商、營養補充劑公司和製藥製造商等大宗買家至關重要。它們確保了產品的廣泛供應,促進了定製配方,並支持長期合約的簽訂。同時,線上零售平台正在改善小規模製造商和尋求果膠產品的專業消費者的購買管道。

預計到2025年,北美柑橘果膠市場規模將達到5.629億美元。消費者對機能性食品、低糖產品和膳食補充劑日益成長的需求是推動其成長的主要因素。在美國,柑橘果膠被廣泛用於糖果甜點、飲料和乳製品中,以打造符合健康意識消費者需求的「潔淨標示」產品。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 對潔淨標示原料的需求不斷成長

- 機能性食品和膳食補充劑的擴張

- 加工食品和簡便食品的消費量增加

- 陷阱與挑戰

- 原料供應波動

- 高昂的採礦和加工成本

- 機會

- 開發低糖和無糖產品

- 在製藥和營養保健品(營養功能性食品)領域的應用

- 永續且可生物分解的包裝

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 來源

- 未來市場趨勢

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依來源分類,2022-2035年

- 橘子

- 檸檬

- 柚子

- 其他

第6章 市場估算與預測:依等級分類,2022-2035年

- 高甲氧基果膠

- 低甲氧基(LM)果膠

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 飲食

- 麵包糖果甜點

- 製藥

- 化妝品和個人保健產品

- 營養補充品

- 機能性食品

- 其他

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 銷售代理商和批發商

- 線上零售

- 便利商店

- 專賣店

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Cargill

- Ingredion

- Herbstreith &Fox KG Pektin-Fabriken

- Tate &Lyle

- Compania Espanola de Algas Marinas(CEAMSA)

- Quadra Chemicals

- Silvateam

- CEAMSA

- Fiberstar

- Krishna Pectins Pvt Ltd

- Labh Ingredients

- IFF

The Global Citrus Pectin Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 2.4 billion by 2035.

Market expansion is driven by the growing demand for natural, plant-based ingredients in food, beverages, nutraceuticals, and pharmaceuticals. Citrus pectin, a polysaccharide extracted primarily from citrus fruit peels, is highly valued for its gelling, thickening, and stabilizing properties. Its versatility in formulation allows it to enhance texture, consistency, and shelf life across various products while supporting reduced-sugar formulations and clean-label initiatives. High methoxyl (HM) pectin forms gels under acidic and sugary conditions, whereas low methoxyl (LM) pectin requires calcium ions, enabling flexibility in application for jams, jellies, confectionery, dairy, and functional foods. Increasing consumer preference for natural, non-GMO ingredients and rising awareness of dietary health benefits are reinforcing the use of citrus pectin, making it a critical functional ingredient for manufacturers seeking to meet evolving food and supplement demands.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 5.4% |

The oranges segment accounted for USD 834.1 million in 2025, reflecting the versatility and functional performance of pectin derived from this source. Orange-based pectin is widely used in food systems for its natural thickening, gelling, and stabilizing characteristics, making it essential for improving texture and product quality. Its clean-label appeal and non-GMO status enhance demand among health-conscious consumers seeking natural and minimally processed ingredients.

The distributors and wholesalers segment reached USD 578.9 million in 2025. These channels are vital for reaching bulk buyers, including food manufacturers, dietary supplement companies, and pharmaceutical producers. They ensure widespread availability, facilitate customized formulations, and support long-term contracts, while online retail platforms are improving access for smaller manufacturers and specialty consumers seeking pectin products.

North America Citrus Pectin Market generated USD 562.9 million in 2025. Rising interest in functional foods, low-sugar products, and dietary supplements is driving adoption. In the United States, citrus pectin is widely incorporated into confectionery, beverages, and dairy products to create clean-label offerings that satisfy health-conscious consumer demands.

Leading companies operating in the Global Citrus Pectin Market include Cargill, Ingredion, Herbstreith & Fox KG Pektin-Fabriken, Tate & Lyle, Compania Espanola de Algas Marinas (CEAMSA), Quadra Chemicals, Silvateam, Fiberstar, Krishna Pectins Pvt Ltd, Labh Ingredients, and IFF. Key strategies adopted by companies in the Citrus Pectin Market focus on product innovation, including developing high-quality, low-sugar, and functional formulations to cater to health-conscious consumers. Strategic partnerships with food and beverage manufacturers help expand distribution channels and secure long-term contracts. Companies also invest in R&D to improve extraction efficiency, enhance purity, and create customized pectin solutions. Geographic expansion, especially into high-growth regions, strengthens market presence, while marketing campaigns emphasize natural, clean-label, and sustainable attributes to build brand loyalty and differentiate products in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Grade

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean-label ingredients

- 3.2.1.2 Expansion of functional foods and supplements

- 3.2.1.3 Increased processed and convenience food consumption

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Raw material supply fluctuations

- 3.2.2.2 High extraction and processing costs

- 3.2.3 Opportunities

- 3.2.3.1 Low-sugar and sugar-free product development

- 3.2.3.2 Pharmaceutical and nutraceutical applications

- 3.2.3.3 Sustainable and biodegradable packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oranges

- 5.3 Lemon

- 5.4 Grapefruit

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Grade, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 High Methoxyl (HM) Pectin

- 6.3 Low Methoxyl (LM) Pectin

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & Beverages

- 7.3 Bakery and Confectionery

- 7.4 Pharmaceutical

- 7.5 Cosmetic and Personal Care Products

- 7.6 Dietary Supplements

- 7.7 Functional Food

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct Sales

- 8.3 Distributors and Wholesalers

- 8.4 Online Retail

- 8.5 Convenience Stores

- 8.6 Specialty Stores

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Cargill

- 10.2 Ingredion

- 10.3 Herbstreith & Fox KG Pektin-Fabriken

- 10.4 Tate & Lyle

- 10.5 Compania Espanola de Algas Marinas (CEAMSA)

- 10.6 Quadra Chemicals

- 10.7 Silvateam

- 10.8 CEAMSA

- 10.9 Fiberstar

- 10.10 Krishna Pectins Pvt Ltd

- 10.11 Labh Ingredients

- 10.12 IFF

柑橘果膠市場:按產品類型、應用和地區分類

柑橘果膠市場:按產品類型、應用和地區分類 柑橘果膠市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032)

柑橘果膠市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032) 柑橘果膠的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年)

柑橘果膠的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年)