|

市場調查報告書

商品編碼

1998850

2026 年至 2035 年低功耗下一代顯示器的市場機會、成長要素、產業趨勢與預測。Low Power Next Generation Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球低功耗下一代顯示器市場預計到 2025 年將價值 1.32 億美元,並以 6.5% 的複合年成長率成長,到 2035 年達到 2.568 億美元。

市場成長主要得益於節能型下一代顯示技術(例如OLED和microLED)在家用電子電器、穿戴式裝置和汽車數位駕駛座等領域的廣泛應用。此外,對採用緊湊型、低功耗微型顯示器的AR、VR和MR應用的需求不斷成長,也推動了市場擴張。電子產業的節能舉措,以及行動裝置和工業設備向常亮型高亮度顯示器的轉變,進一步促進了這些技術的普及。區域擴張,得益於消費性電子產品滲透率的提高、智慧汽車的普及以及節能顯示技術在工業領域的整合,為超小型、高性能和環保面板的創新創造了機會。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1.32億美元 |

| 預計金額 | 2.568億美元 |

| 複合年成長率 | 6.5% |

智慧型手機和平板電腦採用LTPO OLED技術顯著提升了電池效率和效能,從而大大促進了市場發展。市場對AR/VR設備和配備常亮顯示器的穿戴式設備的需求不斷成長,推動了節能型微型顯示器的發展,製造商們正致力於創新緊湊型、高亮度顯示解決方案。新一代顯示器在數位汽車儀錶板中的應用也促進了全球市場成長,這反映出整個產業在消費性電子、工業和汽車應用領域對節能環保技術的關注。

到2025年,OLED市佔率將達到40.6%。 OLED顯示器憑藉其自發光技術、卓越的亮度和高能效,在市場上佔據主導地位,使其成為行動裝置、平板電腦和車載顯示器的理想之選。其支援自適應刷新率和最大限度降低能耗的能力,使其成為家用電子電器、汽車面板和工業應用領域的首選,並推動了其在全球範圍內的普及。

預計到2025年,小尺寸面板(2-7吋對角線)市場規模將達到4,530萬美元。這些面板廣泛應用於智慧型手機、穿戴式裝置和平板電腦,在緊湊的外形規格和顯示性能之間實現了理想的平衡。節能型LCD和LTPO OLED的融合,實現了常亮顯示功能和更長的電池續航時間,使得小尺寸面板成為對能源效率和視覺性能要求極高的消費性電子產品和行動裝置的理想選擇。

到2025年,北美低功耗下一代顯示器市佔率將達到36%。該地區市場成長的主要驅動力是家用電子電器、汽車、工業和智慧基礎設施等應用領域對節能顯示技術的強勁需求。 OLED、microLED和量子點顯示器的普及應用是支撐該地區銷售的關鍵因素,這些顯示器在提供卓越影像品質的同時,還能比傳統LCD降低功耗。主要顯示器製造商的入駐以及對創新低功耗技術的早期應用,進一步鞏固了該地區在北美市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- LTPO OLED在智慧型手機中的快速普及

- 在穿戴式健康監測設備的應用範圍擴大

- 需要節能型微型顯示器的AR/VR設備

- 支援低功耗電子設備的永續發展法規

- 汽車產業向數位化駕駛座顯示器的轉變

- 產業潛在風險與挑戰

- 低溫聚合物氧化物(LTPO)製造中產量比率最佳化的複雜性

- 微型LED的大規模量產受到限制。

- 市場機遇

- 折疊式OLED面板,具備自適應刷新功能

- 適用於物聯網邊緣設備的低功耗顯示器

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依技術分類,2022-2035年

- OLED

- MicroLED

- 電子紙

- 先進的低功耗液晶顯示器

第6章 市場估價與預測:依面板尺寸分類,2022-2035年

- 微型顯示器(對角線小於2英吋)

- 小面板(對角線2-7吋)

- 中等尺寸面板(對角線7-17吋)

- 大尺寸面板(對角線17-43吋)

- 超大尺寸面板(對角線尺寸 43 吋或更大)

第7章 市場估計與預測:依外形規格,2022-2035年

- 剛性顯示器

- 軟性顯示器

- 折疊式顯示器

- 捲軸式/滑軌式顯示器

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 家用電子電器

- 汽車顯示器

- 穿戴式裝置

- AR/VR/XR 設備(擴增實境)

- 工業和商業用途

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- LG Display

- Samsung Display

- BOE Technology Group

- Universal Display Corporation(UDC)

- 按地區分類的主要企業

- 北美洲

- QUALCOMM Incorporated

- Nanosys

- Planar Systems

- 亞太地區

- AU Optronics Corporation

- AUO Corporation

- Sharp Corporation

- Sony Corporation

- Panasonic Corporation

- Tianma

- Visionox Technology

- Futaba Corporation

- Doosan Group

- 歐洲

- Novaled GmbH

- Philips

- 北美洲

- 特殊玩家/干擾者

- Dupont

- RitDisplay

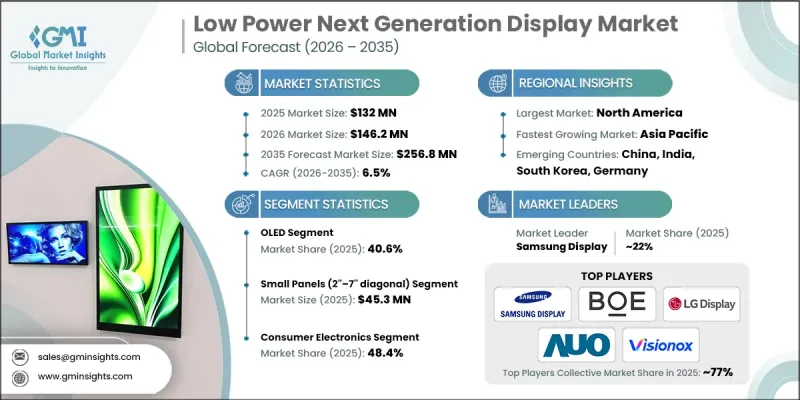

The Global Low Power Next Generation Display Market was valued at USD 132 million in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 256.8 million in 2035.

Market growth is driven by the rising adoption of energy-efficient next-generation display technologies such as OLED and microLED across consumer electronics, wearable devices, and automotive digital cockpits. Increasing demand for AR, VR, and MR applications utilizing compact low-power microdisplays is also propelling expansion. Energy-saving initiatives in the electronics sector, coupled with the shift to always-on and high-brightness displays in mobile devices and industrial equipment, are further boosting adoption. Geographic expansion is supported by rising consumer electronics penetration, smart vehicle adoption, and industrial integration of energy-efficient display technologies, creating opportunities for innovation in ultra-compact, high-performance, and eco-friendly panels.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $132 Million |

| Forecast Value | $256.8 Million |

| CAGR | 6.5% |

The market is significantly benefiting from the adoption of LTPO OLED technology in smartphones and tablets, which enhances battery efficiency and performance. Growing demand for AR/VR devices and wearables with always-on displays is driving the development of energy-efficient microdisplays, encouraging manufacturers to innovate in compact, high-brightness display solutions. The integration of next-generation displays in digital automotive dashboards is also contributing to global market growth, reflecting the industry's focus on energy-saving, eco-friendly technologies across consumer, industrial, and automotive applications.

The OLED segment accounted for a 40.6% share in 2025. OLED displays dominate due to their self-emissive technology, superior brightness, and energy efficiency, making them highly suitable for mobile devices, tablets, and automotive displays. Their ability to support adaptive refresh rates and minimize energy consumption has made them a preferred choice in consumer electronics, automotive panels, and industrial applications, driving widespread adoption globally.

The small panel segment (2"-7" diagonal) reached USD 45.3 million in 2025. These panels are widely used in smartphones, wearables, and tablets, offering an ideal balance between compact form factor and display performance. Power-efficient LCD and LTPO OLED integration enables always-on functionality and extended battery life, positioning small panels as the most suitable option for consumer electronics and portable devices where energy efficiency and visual performance are critical.

North America Low Power Next Generation Display Market held a 36% share in 2025. Market growth in the region is driven by strong demand for energy-efficient display technologies in consumer electronics, automotive, industrial, and smart infrastructure applications. Adoption of OLED, microLED, and quantum dot displays, which deliver enhanced visual quality with lower power consumption compared to traditional LCDs, is a key factor supporting regional revenue. The presence of major display manufacturers and early adoption of innovative low-power technologies further reinforces North America's leading market position.

Leading players in the Global Low Power Next Generation Display Market include AU Optronics Corporation, AUO Corporation, BOE Technology Group, Doosan Group, DuPont, Futaba Corporation, LG Display, Nanosys, Novaled GmbH, Panasonic Corporation, Philips, Planar Systems, QUALCOMM Incorporated, RitDisplay, Samsung Display, Sharp Corporation, Sony Corporation, Tianma, Universal Display Corporation (UDC), and Visionox Technology. Companies in the Low Power Next Generation Display Market are adopting multiple strategies to strengthen their presence and expand market share. They are heavily investing in R&D to develop high-brightness, ultra-compact, and energy-efficient OLED, microLED, and LTPO technologies. Strategic partnerships with consumer electronics, automotive, and wearable device manufacturers ensure integration of their display solutions into next-generation devices. Firms are expanding production capacity and manufacturing footprints in key regions to meet growing global demand. Additionally, technology licensing, joint ventures, and targeted marketing campaigns emphasizing energy efficiency and sustainability are being leveraged to enhance brand visibility and maintain competitive advantage in this rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Panel size trends

- 2.2.3 Form factor trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid adoption of LTPO OLED in smartphones

- 3.2.1.2 Expanding use in wearable health monitoring devices

- 3.2.1.3 AR/VR devices requiring energy-efficient microdisplays

- 3.2.1.4 Sustainability regulations favoring lower power electronics

- 3.2.1.5 Automotive shift toward digital cockpit displays

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 LTPO fabrication yield optimization complexities

- 3.2.2.2 Limited large-scale microLED mass production

- 3.2.3 Market opportunities

- 3.2.3.1 Foldable OLED panels with adaptive refresh

- 3.2.3.2 Low-power displays for IoT edge devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 OLED

- 5.3 MicroLED

- 5.4 E-paper

- 5.5 Advanced low-power LCD

Chapter 6 Market Estimates and Forecast, By Panel Size, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Microdisplays (< 2 inches diagonal)

- 6.3 Small panels (2" - 7" diagonal)

- 6.4 Medium panels (7" - 17" diagonal)

- 6.5 Large panels (17" - 43" diagonal)

- 6.6 Extra large panels (≥ 43" diagonal)

Chapter 7 Market Estimates and Forecast, By Form Factor, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Rigid displays

- 7.3 Flexible displays

- 7.4 Foldable displays

- 7.5 Rollable / slidable displays

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive displays

- 8.4 Wearable devices

- 8.5 AR / VR / XR devices (extended reality)

- 8.6 Industrial & commercial applications

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 LG Display

- 10.1.2 Samsung Display

- 10.1.3 BOE Technology Group

- 10.1.4 Universal Display Corporation (UDC)

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 QUALCOMM Incorporated

- 10.2.1.2 Nanosys

- 10.2.1.3 Planar Systems

- 10.2.2 Asia Pacific

- 10.2.2.1 AU Optronics Corporation

- 10.2.2.2 AUO Corporation

- 10.2.2.3 Sharp Corporation

- 10.2.2.4 Sony Corporation

- 10.2.2.5 Panasonic Corporation

- 10.2.2.6 Tianma

- 10.2.2.7 Visionox Technology

- 10.2.2.8 Futaba Corporation

- 10.2.2.9 Doosan Group

- 10.2.3 Europe

- 10.2.3.1 Novaled GmbH

- 10.2.3.2 Philips

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Dupont

- 10.3.2 RitDisplay