|

市場調查報告書

商品編碼

1998844

水性丙烯酸樹脂市場機會、成長要素、產業趨勢分析及2026-2035年預測。Waterborne Acrylic Resin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

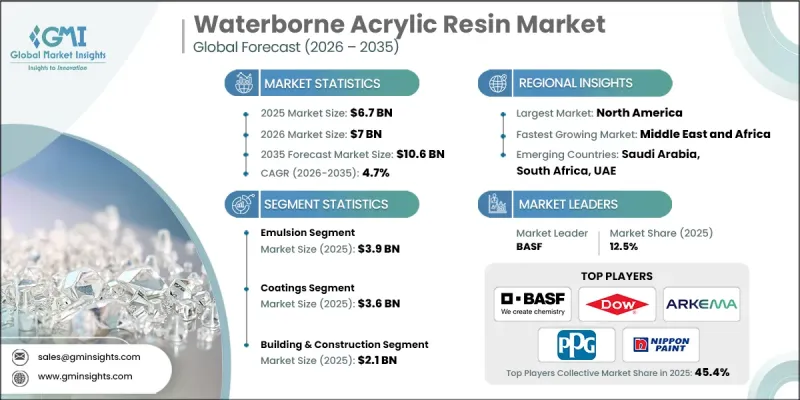

2025 年全球水性丙烯酸樹脂市場價值為 67 億美元,預計到 2035 年將達到 106 億美元,年複合成長率為 4.7%。

塗料、黏合劑和油漆製造業對環保聚合物解決方案的需求不斷成長,推動了市場成長。水性丙烯酸樹脂採用水性聚合物系統配製而成,與傳統的溶劑型產品相比,其揮發性有機化合物 (VOC)排放更低,因此適用於對環境和室內空氣品質標準要求更高的應用。這些樹脂透過丙烯酸單體的乳液聚合反應而製得,形成穩定的水性分散體,具有強黏合力、柔軟性和耐久性。其優異的性能使其成為保護性表面、裝飾性塗料以及對法規合規性和長期可靠性要求極高的工業應用的理想選擇。隨著各行業日益重視永續生產方式,水性丙烯酸技術在現代配方策略中扮演越來越重要的角色。樹脂化學的持續創新進一步提升了產品性能,使製造商能夠滿足多個終端應用領域不斷變化的技術和環境要求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 67億美元 |

| 預測金額 | 106億美元 |

| 複合年成長率 | 4.7% |

塗料產業正經歷著從溶劑型技術轉向水性丙烯酸樹脂系統的明顯轉變。這一轉變使製造商能夠在滿足日益嚴格的環保標準的同時,最大限度地減少排放並保持塗料的優異性能。顆粒工程、交聯方法和混合樹脂開發的進步提高了塗料的硬度、耐化學性和耐候性。因此,水性丙烯酸體系的性能如今已達到甚至超過傳統配方,從而推動了其在行業內的廣泛應用。

預計2025年,乳液樹脂市場規模將達39億美元。其成長主要得益於配方的多樣性及其對廣泛應用的適用性。乳液樹脂技術的不斷改進提高了乾燥效率、表面保護性能和整體使用壽命,從而增強了其在永續產品開發中的作用。

預計到2025年,塗料應用領域的市場規模將達到36億美元。這一成長主要得益於市場對符合環保法規的低VOC建築和工業塗料的需求不斷成長。建設活動的活性化以及溶劑型塗料向水性塗料的穩定轉變,也推動了該領域的成長。為了滿足日益嚴格的裝飾和防護標準,製造商正優先提升塗料的耐久性、耐化學性和長期性能。

預計北美水性丙烯酸樹脂市場規模將從2025年的24億美元增加到2035年的37億美元。該地區的需求成長得益於嚴格的環境政策、房屋維修工程以及永續的工業生產。在美國,基礎設施投資、住宅維修和持續的工業維護活動維持了低排放量塗料的穩定消費。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 嚴格的環境法規正在推動樹脂的採用。

- 建築和裝飾塗料的需求不斷成長

- 提高樹脂性能的技術進步

- 產業潛在風險與挑戰

- 生產成本高是一個阻礙因素。

- 嚴苛條件下的性能限制

- 市場機遇

- 混合式和高性能配方創新

- 在黏合劑和特殊塗料領域不斷拓展應用

- 策略夥伴關係可加速市場成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 乳液

- 解決方案

- 胺甲酸乙酯和丙烯酸

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 塗層

- 黏合劑

- 纖維整理

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 建築/施工

- 車

- 家具

- 包裝

- 纖維

- 黏合劑和密封劑

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- AkzoNobel

- Arkema

- BASF

- Dow Chemical

- Eastman Chemical

- Evonik Industries

- Huntsman

- Nippon Paint

- Nippon Shokubai

- PPG Industries

The Global Waterborne Acrylic Resin Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 10.6 billion by 2035.

Market growth is driven by increasing demand for environmentally responsible polymer solutions across coatings, adhesives, and paint manufacturing. Waterborne acrylic resins are formulated as aqueous polymer systems that offer reduced volatile organic compound emissions compared to conventional solvent-based alternatives, making them suitable for applications that require improved environmental and indoor air quality standards. These resins are produced through emulsion polymerization of acrylic monomers, resulting in stable water-based dispersions with strong adhesion, flexibility, and durability. Their performance characteristics make them well suited for protective surfaces, decorative finishes, and industrial applications that require both regulatory compliance and long-term reliability. As industries place greater emphasis on sustainable production methods, waterborne acrylic technologies are becoming increasingly central to modern formulation strategies. Ongoing innovation in resin chemistry is further strengthening product performance, enabling manufacturers to meet evolving technical and environmental requirements across multiple end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $10.6 Billion |

| CAGR | 4.7% |

The coatings sector is undergoing a clear transition from solvent-based technologies toward waterborne acrylic resin systems. This shift allows manufacturers to comply with tightening environmental standards while minimizing emissions and maintaining competitive coating performance. Advances in particle engineering, crosslinking methods, and hybrid resin development have enhanced hardness, chemical resistance, and weather durability. As a result, waterborne acrylic systems now deliver performance levels comparable to or exceeding traditional formulations, driving broader industrial acceptance.

The emulsion segment reached USD 3.9 billion in 2025. Its growth is supported by formulation versatility and compatibility with a wide range of applications. Continuous improvements in emulsion resin technology are enhancing drying efficiency, surface protection, and overall service life, reinforcing their role in sustainable product development.

The coatings application segment generated USD 3.6 billion in 2025. Expansion is fueled by rising demand for low-VOC architectural and industrial coatings aligned with environmental regulations. Increased construction activity and the steady replacement of solvent-borne systems with water-based alternatives are contributing to segment growth. Manufacturers are prioritizing improvements in durability, chemical resistance, and long-term performance to meet stringent decorative and protective standards.

North America Waterborne Acrylic Resin Market is projected to grow from USD 2.4 billion in 2025 to USD 3.7 billion by 2035. Regional demand is supported by strict environmental policies, renovation activities, and sustained industrial output. In the United States, infrastructure investments, housing upgrades, and ongoing industrial maintenance are sustaining consistent consumption of low-emission coating materials.

Major companies operating in the Global Waterborne Acrylic Resin Market include BASF, Dow Chemical, AkzoNobel, Arkema, PPG Industries, Eastman Chemical, Evonik Industries, Nippon Paint, Huntsman, and Nippon Shokubai. Companies in the Global Waterborne Acrylic Resin Market are strengthening their market position through innovation, sustainability initiatives, and strategic expansion. Leading manufacturers are investing in advanced polymer research to enhance durability, weather resistance, and chemical stability while maintaining low VOC performance. Capacity expansion and modernization of production facilities are improving operational efficiency and supply reliability. Strategic collaborations with coatings and adhesive formulators are broadening application reach and accelerating product commercialization. Firms are also focusing on regulatory compliance and eco-certifications to align with global environmental standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strict environmental regulations boosting resin adoption

- 3.2.1.2 Rising demand in architectural and decorative coatings

- 3.2.1.3 Technological advancements improving resin performance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs limiting

- 3.2.2.2 Performance limitations in extreme conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Innovation in hybrid and high-performance formulations

- 3.2.3.2 Expanding applications in adhesives and specialty coatings

- 3.2.3.3 Strategic collaborations to accelerate market growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Emulsion

- 5.3 Solution

- 5.4 Urethane-acrylic

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coating

- 6.3 Adhesives

- 6.4 Textile finishes

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building & construction

- 7.3 Automotive

- 7.4 Furniture

- 7.5 packaging

- 7.6 Textile

- 7.7 Adhesives & sealants

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AkzoNobel

- 9.2 Arkema

- 9.3 BASF

- 9.4 Dow Chemical

- 9.5 Eastman Chemical

- 9.6 Evonik Industries

- 9.7 Huntsman

- 9.8 Nippon Paint

- 9.9 Nippon Shokubai

- 9.10 PPG Industries

丙烯酸樹脂市場:2026-2032年全球市場按產品類型、形態、最終用戶和分銷管道分類的預測

丙烯酸樹脂市場:2026-2032年全球市場按產品類型、形態、最終用戶和分銷管道分類的預測 實心熱塑性丙烯酸(珠狀)樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)銦環市場按類型、純度、包裝、製程、厚度、應用和最終用途產業分類 - 全球預測(2026-2032 年)

實心熱塑性丙烯酸(珠狀)樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)銦環市場按類型、純度、包裝、製程、厚度、應用和最終用途產業分類 - 全球預測(2026-2032 年) 丙烯酸樹脂市場規模、佔有率和成長分析(按化學成分、溶劑強度、應用、最終用戶和地區分類)—產業預測,2026-2033年

丙烯酸樹脂市場規模、佔有率和成長分析(按化學成分、溶劑強度、應用、最終用戶和地區分類)—產業預測,2026-2033年 固態環氧樹脂:全球市佔率及排名、總收入及需求預測(2025-2031年)

固態環氧樹脂:全球市佔率及排名、總收入及需求預測(2025-2031年) 全球丙烯酸樹脂市場(依化學性質、性質、溶解度、應用、最終用途產業及地區分類)- 預測至2030年

全球丙烯酸樹脂市場(依化學性質、性質、溶解度、應用、最終用途產業及地區分類)- 預測至2030年 全球固體熱塑性丙烯酸珠粒樹脂市場

全球固體熱塑性丙烯酸珠粒樹脂市場