|

市場調查報告書

商品編碼

1998838

流感疫苗市場機會、成長要素、產業趨勢分析及2026-2035年預測。Influenza Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

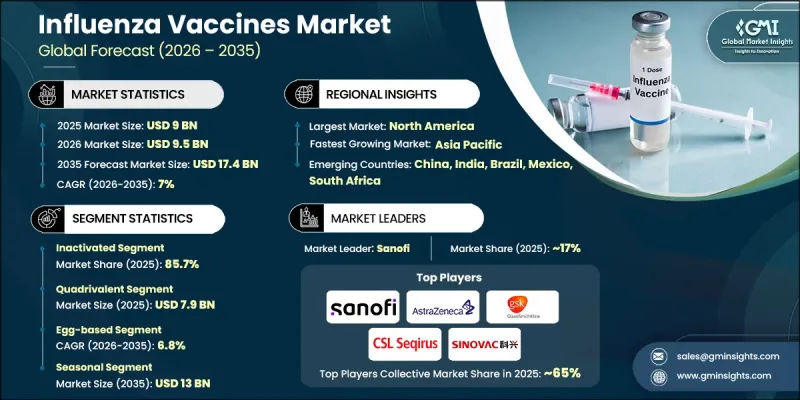

預計到 2025 年,全球流感疫苗市場價值將達到 90 億美元,並有望以 7% 的複合年成長率成長,到 2035 年達到 174 億美元。

流感疫苗市場是指致力於研發、生產和分發疫苗以保護人們免受流行流感病毒侵害的全球生態系統。這些疫苗旨在降低感染率、減輕疾病嚴重程度並增強群體免疫力,尤其是在併發症高風險族群中。整個產業採用多種疫苗技術,包括為增強免疫保護和應對病毒變異株而開發的多種免疫平台。一個顯著的行業趨勢是轉向先進的疫苗研發技術,旨在提高生產效率和免疫免疫抗原性。傳統生產方法擴大得到現代製造平台的支持,這些平台能夠提高抗原相容性、增加產量並提高生產計劃的靈活性。政府主導的免疫接種舉措和機構採購計劃也支持長期需求成長。促進年度免疫接種的公共衛生政策,加上國家儲備計劃和擴大醫療保險覆蓋範圍,正在推動疫苗接種的持續進行。這些政策框架持續刺激對研發和生產能力的投資,同時應對與疫苗效力和生產計畫相關的長期挑戰。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 90億美元 |

| 預計金額 | 174億美元 |

| 複合年成長率 | 7% |

預計到2025年,去活化疫苗市場佔有率將達到85.7%,並在2026年至2035年間以6.9%的複合年成長率成長。該細分市場憑藉其良好的安全性記錄和對不同人群的廣泛適用性,保持著主導地位。去活化流感疫苗在免疫規劃中持續廣泛應用,因為它們能夠在不引入可複製病毒顆粒的情況下誘發保護性免疫反應。其安全性使其適用於包括不同健康狀況人群在內的各類人群,這也推動了其在國家免疫戰略中的廣泛應用。

預計2025年,四價流感疫苗市場規模將達到79億美元。這類疫苗之所以在該市場佔據主導地位,是因為它們能夠在單一配方中提供多種流行流感病毒株的廣泛保護。更廣泛的病毒株覆蓋範圍降低了疫苗成分與季節性病毒模式不匹配的風險,從而提高了免疫宣傳活動的整體有效性。這種更全面的保護能力使四價疫苗成為大規模免疫接種舉措的首選。此外,這些疫苗能夠適應季節性變化,有助於改善臨床療效,降低住院率,並在流感流行季節更好地保護公眾健康。

預計到2025年,北美流感疫苗市佔率將達到44.9%。該地區憑藉其先進的醫療基礎設施、完善的法規結構以及公眾對預防醫學的高度重視,保持著強勁的市場地位。美國完善的疾病監測系統和鼓勵常規疫苗接種的醫療政策進一步鞏固了其在區域市場的主導地位。針對廣大民眾推廣年度流感疫苗接種的公共衛生計畫持續支撐著強勁的需求,並推動了兒童、成人和高風險族群疫苗市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 流感疫情蔓延

- 政府擴大衛生舉措和免疫接種計劃

- 疫苗技術的進步

- 產業潛在風險與挑戰

- 疫苗研發高成本

- 疫苗生產週期延長

- 市場機遇

- 擴大通用型和頻譜流感疫苗的接種範圍

- 擴大兒童和孕婦免疫接種計劃。

- 促進因素

- 成長潛力分析

- 監理情勢(基於初步調查)

- 管道分析

- 專利分析

- 技術與創新趨勢(基於初步調查)

- 目前技術

- 新興技術

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:疫苗類型,2022-2035年

- 失活

- 減毒活病毒疫苗

- 重組

第6章 市場估計與預測:依適應症分類,2022-2035年

- 四價

- 三價

第7章 市場估計與預測:依技術分類,2022-2035年

- 蛋製品

- 基於細胞

- 重組技術

第8章 市場估計與預測:依流感類型分類,2022-2035年

- 季節性

- 大流行

第9章 市場估計與預測:依年齡層別分類,2022-2035年

- 兒童

- 成人

第10章 市場估計與預測:依給藥途徑分類,2022-2035年

- 注射

- 鼻噴霧

第11章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 民眾

- 私人的

- 診所

- 其他最終用戶

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- AstraZeneca

- Bharat Biotech

- Cadila Healthcare(Zydus Lifesciences)

- CSL Seqirus

- Denka Seiken

- GlaxoSmithKline

- Sanofi

- Serum Institute of India

- Sinovac Biotech

- SK bioscience

- Viatris

- GC Biopharma

- Bio Farma

The Global Influenza Vaccines Market was valued at USD 9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 17.4 billion by 2035.

The influenza vaccines market represents the global ecosystem dedicated to the development, production, and distribution of vaccines that help protect populations from circulating influenza viruses. These vaccines are designed to lower infection rates, minimize the severity of illness, and strengthen community-level immunity, particularly among individuals who are more vulnerable to complications. Various vaccine technologies are utilized across the industry, including multiple immunization platforms developed to improve immune protection and respond to evolving viral strains. A notable industry trend involves the transition toward advanced vaccine development technologies aimed at improving production efficiency and immunogenic performance. Traditional production methods are increasingly supported by modern manufacturing platforms that enable improved antigen matching, higher output levels, and more flexible production timelines. Government-backed immunization initiatives and institutional procurement programs are also supporting long-term demand growth. Public health policies that promote annual vaccination, combined with national stockpiling programs and broader healthcare coverage, are encouraging consistent vaccine uptake. These policy frameworks continue to stimulate investment in research, development, and manufacturing capacity while addressing longstanding challenges related to vaccine effectiveness and production timelines.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7% |

The inactivated segment held 85.7% share in 2025 and is projected to grow at a CAGR of 6.9% throughout 2026-2035. This segment maintains a leading position due to its well-established safety record and broad applicability across diverse population groups. Inactivated influenza vaccines remain widely utilized in immunization programs because they generate protective immune responses without introducing replicating viral particles. Their safety profile makes them suitable for use across a wide demographic range, including individuals with varying health conditions, which reinforces their widespread adoption within national vaccination strategies.

The quadrivalent vaccine segment generated USD 7.9 billion in 2025. These vaccines dominate the segment because they provide expanded protection against multiple circulating influenza virus strains within a single formulation. Broader strain coverage helps reduce the risk of mismatch between vaccine composition and seasonal viral patterns, which improves the overall effectiveness of vaccination campaigns. This expanded protective capability has made quadrivalent vaccines a preferred choice for large-scale immunization initiatives. In addition, the ability of these vaccines to address seasonal variability contributes to improved clinical outcomes, lower hospitalization rates, and stronger public health protection during influenza seasons.

North America Influenza Vaccines Market accounted for 44.9% share in 2025. The region maintains its strong position due to its advanced healthcare infrastructure, supportive regulatory frameworks, and high public awareness regarding preventive healthcare practices. The leadership of United States within the regional market is reinforced by well-established disease surveillance systems and healthcare policies that encourage routine vaccination. Public health programs that promote annual influenza vaccination across broad population groups continue to support strong demand, contributing to consistent market expansion across pediatric, adult, and high-risk populations.

Key participants operating in the Global Influenza Vaccines Market include Sanofi, GlaxoSmithKline, AstraZeneca, CSL Seqirus, Serum Institute of India, Sinovac Biotech, SK Bioscience, Viatris, GC Biopharma, Bharat Biotech, Cadila Healthcare (Zydus Lifesciences), Denka Seiken, and Bio Farma. Companies operating in the Global Influenza Vaccines Market are implementing several strategies to strengthen their competitive presence and expand market share. Leading vaccine manufacturers are investing heavily in research and development to advance next-generation vaccine platforms that offer improved immune responses and faster production capabilities. Strategic partnerships with government health agencies and international health organizations are helping companies secure large procurement contracts and strengthen supply networks. Firms are also expanding manufacturing capacity and adopting advanced production technologies to support large-scale vaccination programs. In addition, companies are increasing their focus on global distribution infrastructure and regional market expansion to improve vaccine accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Indication trends

- 2.2.4 Flu type trends

- 2.2.5 Age group trends

- 2.2.6 Route of administration trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of influenza

- 3.2.1.2 Rising government health initiatives and immunization programs

- 3.2.1.3 Advancements in vaccine technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with vaccine development

- 3.2.2.2 Longer vaccine production timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of universal and broader-spectrum influenza vaccines

- 3.2.3.2 Growth in pediatric and maternal immunization programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Patent analysis

- 3.7 Technology and innovation landscape (Driven by Primary Research)

- 3.7.1 Current technologies

- 3.7.2 Emerging technologies

- 3.8 Future market trends (Driven by Primary Research)

- 3.9 Impact of AI and generative AI on the market

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Inactivated

- 5.3 Live attenuated

- 5.4 Recombinant

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Quadrivalent

- 6.3 Trivalent

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Egg-based

- 7.3 Cell-based

- 7.4 Recombinant technology

Chapter 8 Market Estimates and Forecast, By Flu Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Seasonal

- 8.3 Pandemic

Chapter 9 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Pediatric

- 9.3 Adults

Chapter 10 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Injection

- 10.3 Nasal spray

Chapter 11 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 Hospitals

- 11.2.1 Public

- 11.2.2 Private

- 11.3 Clinics

- 11.4 Other end users

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 AstraZeneca

- 13.2 Bharat Biotech

- 13.3 Cadila Healthcare (Zydus Lifesciences)

- 13.4 CSL Seqirus

- 13.5 Denka Seiken

- 13.6 GlaxoSmithKline

- 13.7 Sanofi

- 13.8 Serum Institute of India

- 13.9 Sinovac Biotech

- 13.10 SK bioscience

- 13.11 Viatris

- 13.12 GC Biopharma

- 13.13 Bio Farma

流感疫苗市場:2026-2032年全球市場預測(依疫苗類型、年齡層、劑量、配方、通路和最終用戶分類)

流感疫苗市場:2026-2032年全球市場預測(依疫苗類型、年齡層、劑量、配方、通路和最終用戶分類) 全球豬流感疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球豬流感疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 流感疫苗市場規模、佔有率和趨勢分析報告:按疫苗類型、適應症、年齡層、給藥途徑、分銷管道、地區和細分市場預測(2026-2033 年)

流感疫苗市場規模、佔有率和趨勢分析報告:按疫苗類型、適應症、年齡層、給藥途徑、分銷管道、地區和細分市場預測(2026-2033 年) 流感疫苗市場分析及預測(至2035年):類型、產品、技術、適應性、劑型、通路、給藥途徑

流感疫苗市場分析及預測(至2035年):類型、產品、技術、適應性、劑型、通路、給藥途徑 流感疫苗市場規模、佔有率和趨勢:按疫苗類型、技術、年齡層、給藥途徑、地區分類,並預測至 2026-2034 年。

流感疫苗市場規模、佔有率和趨勢:按疫苗類型、技術、年齡層、給藥途徑、地區分類,並預測至 2026-2034 年。 流感疫苗市場:依疫苗類型、價數、給藥途徑、年齡層、技術、通路和地區分類。流感疫苗市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測犬流感疫苗市場:依疫苗類型、病毒類型、通路和地區分類。

流感疫苗市場:依疫苗類型、價數、給藥途徑、年齡層、技術、通路和地區分類。流感疫苗市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測犬流感疫苗市場:依疫苗類型、病毒類型、通路和地區分類。 H7N9疫苗市場規模、佔有率和成長分析:按疫苗類型、配方、給藥途徑、應用、最終用戶、通路、地區和行業預測,2026-2033年全球流感疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

H7N9疫苗市場規模、佔有率和成長分析:按疫苗類型、配方、給藥途徑、應用、最終用戶、通路、地區和行業預測,2026-2033年全球流感疫苗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)