|

市場調查報告書

商品編碼

1998834

運動醫學市場機會、成長要素、產業趨勢分析及2026-2035年預測Sports Medicine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

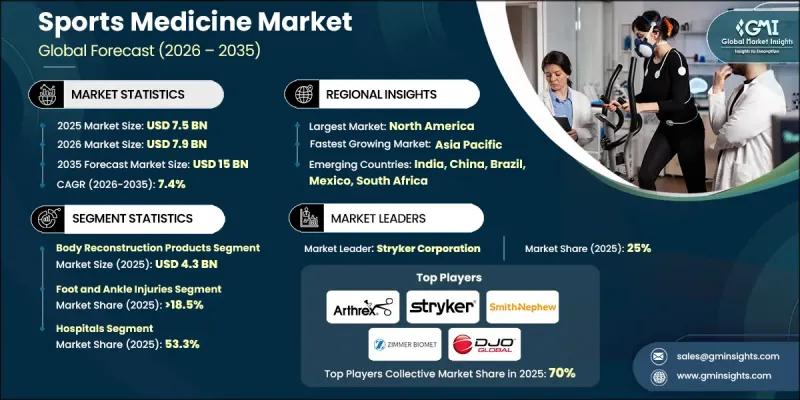

全球運動醫學市場預計到 2025 年將價值 75 億美元,預計到 2035 年將以 7.4% 的複合年成長率成長至 150 億美元。

受全球運動傷害率上升以及植入、穿戴式裝置和微創手術等技術進步的推動,運動醫學市場正在蓬勃發展。由於關節鏡手術和其他微創技術相比傳統手術具有許多優勢,例如恢復更快、疼痛更輕、併發症率更低,因此醫療專業人員正擴大採用這些技術。運動醫學涵蓋旨在預防、診斷和治療運動相關傷害的產品和服務,包括醫療設備、植入、復健設備和運動表現監測工具。此外,運動參與度的提高、健身意識的增強以及損傷管理技術的創新也進一步推動了該市場的發展。採用生物相容性材料、3D列印和智慧塗層的先進植入能夠加速癒合,同時最大限度地降低感染風險。感測器和智慧手環等穿戴式裝置能夠即時監測肌肉活動、動態和壓力水平,從而支持個人化治療並改善康復效果。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 75億美元 |

| 預計金額 | 150億美元 |

| 複合年成長率 | 7.4% |

預計2025年,人體重組產品市場規模將達43億美元。這些產品包括用於修復、替換或重組運動傷害後受損的骨骼、關節和組織的醫療設備和生物製藥。它們在恢復活動能力、穩定性和功能方面發揮著至關重要的作用,使運動員能夠更快地重返賽場。運動相關損傷數量的增加以及對先進治療方法日益成長的需求正在推動人體重組產品的普及。諸如3D列印植入、生物可吸收材料和再生醫學生物製劑等創新技術正在改善手術效果、縮短恢復時間並提高患者滿意度。

到2025年,足踝損傷市場將佔市場佔有率的18.5%。這些部位的損傷包括骨折、扭傷、斷裂和應力性骨折,這些損傷會對活動能力和運動表現產生顯著影響。高強度運動、過度使用和穿著不合適的鞋子是導致這些傷害的主要因素。隨著患者和醫療專業人員越來越重視早期療育和有效的復健策略,損傷預防、診斷和復健技術的不斷進步正在推動該細分市場的成長。

到2025年,北美運動醫學市佔率將達到36.4%。該地區市場成長的驅動力包括先進的醫療基礎設施、技術創新以及日益成長的體育參與。青少年和成人中骨折、韌帶斷裂、腦震盪和過度使用綜合症等損傷發生率的上升,使得先進治療方法、復健服務和預防醫學的需求強勁。該地區受益於完善的醫療設施、技術精湛的醫護人員以及旨在推廣安全運動的宣傳活動。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 全球運動傷害病例呈上升趨勢。

- 植入和穿戴式裝置的技術進步

- 對微創手術的需求日益成長,以及運動醫學中心的增加。

- 人們對身體健康和體育活動的認知不斷提高

- 產業潛在風險與挑戰

- 開發中國家訓練有素的醫護人員短缺

- 運動醫學費用高昂

- 市場機遇

- 遠端醫療和遠距復健服務的發展將使混合護理模式成為可能。

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術進步

- 當前技術趨勢

- 新興技術

- 2025年價格分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

- 人工智慧和生成式人工智慧對市場的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 身體重組產品

- 整形外科植入

- 骨折和韌帶修復產品

- 關節鏡設備

- 軟組織修復產品

- 義肢

- 正交生物製品

- 身體支持和恢復

- 矯正器具和支架

- 壓力衣

- 物理治療設備

- 熱療

- 電刺激

- 其他實體支撐和恢復產品

- 配件

- 繃帶

- 磁帶

- 消毒劑

- 裹

- 其他配件

- 其他產品

第6章 市場估計與預測:依傷害類型分類,2022-2035年

- 膝傷

- 肩部受傷

- 足部和踝部損傷

- 背部和脊椎損傷

- 髖部和鼠蹊部損傷

- 其他損害

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 物理治療中心

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Stryker

- Arthrex, Inc.

- Wright Medical Technology

- Otto Bock Healthcare

- Zimmer Biomet

- Smith &Nephew Plc

- Breg, Inc.

- Muller Sports, Inc.

- RTI Surgical

- Performance Health International Limited

- KARL STORZ

- Bauerfeind AG

- CONMED Corporation

- Johnson &Johnson

- Ossur Corporate

- Creamer Product, Inc.

- DJO Global

- Anika Therapeutics, Inc.

The Global Sports Medicine Market was valued at USD 7.5 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 15 billion by 2035.

The market's growth is fueled by the rising prevalence of sports injuries worldwide, coupled with technological advancements in implants, wearable devices, and minimally invasive surgical procedures. Healthcare providers are increasingly adopting arthroscopic and other minimally invasive techniques due to their advantages, including faster recovery, reduced pain, and lower complication rates compared to traditional surgeries. Sports medicine encompasses products and services designed to prevent, diagnose, and treat sports-related injuries, including medical devices, implants, rehabilitation equipment, and performance monitoring tools. The market is further driven by growing sports participation, heightened fitness awareness, and innovations in injury management technologies. Advanced implants using biocompatible materials, 3D printing, and smart coatings accelerate healing while minimizing infection risks. Wearable devices such as sensors and smart bands provide real-time monitoring of muscle activity, biomechanics, and stress levels, supporting personalized treatment and enhanced recovery outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.5 Billion |

| Forecast Value | $15 Billion |

| CAGR | 7.4% |

The body reconstruction products segment generated USD 4.3 billion in 2025. These products include medical devices and biologics designed to repair, replace, or reconstruct damaged bones, joints, and tissues following sports injuries. They play a vital role in restoring mobility, stability, and functionality, enabling athletes to return to their activities faster. Growing sports-related injuries and demand for advanced treatment options drive the adoption of body reconstruction products. Innovations like 3D-printed implants, bioresorbable materials, and regenerative biologics enhance surgical outcomes, reduce recovery time, and improve patient satisfaction.

The foot and ankle injuries segment generated 18.5% share in 2025. Injuries in these areas include fractures, sprains, tendon tears, and stress fractures, which significantly impact mobility and athletic performance. High-impact activities, overuse, and improper footwear contribute to their prevalence. Continuous advancements in injury prevention, diagnostics, and rehabilitation technologies support market growth in this segment, as patients and healthcare providers prioritize early intervention and effective recovery strategies.

North America Sports Medicine Market held a 36.4% share in 2025. Market growth in the region is driven by advanced healthcare infrastructure, technological innovation, and rising sports participation. Increasing incidences of injuries such as fractures, ligament tears, concussions, and overuse conditions among youth and adults have created a strong demand for advanced treatment options, rehabilitation services, and preventive care. The region benefits from a combination of highly equipped medical facilities, skilled healthcare professionals, and awareness campaigns promoting safe athletic practices.

Key companies operating in the Global Sports Medicine Market include Wright Medical Technology, DJO Global, Arthrex, Inc., Johnson & Johnson, Performance Health International Limited, Zimmer Biomet, Stryker, CONMED Corporation, Anika Therapeutics, Inc., Otto Bock Healthcare, Smith & Nephew Plc, Muller Sports, Inc., Creamer Product, Inc., KARL STORZ, Breg, Inc., and Bauerfeind AG. Companies in the Sports Medicine Market are expanding their presence by investing in research and development of innovative implants, wearable devices, and regenerative biologics. Manufacturers are forming strategic partnerships with hospitals, clinics, and sports organizations to integrate products into treatment and rehabilitation programs. Geographic expansion into emerging markets allows access to a growing base of athletes and recreational participants. Firms are also focusing on minimally invasive solutions to improve recovery outcomes and patient satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Injury type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of sports injuries globally

- 3.2.1.2 Technological advancements in implants and wearable devices

- 3.2.1.3 Growing demand for minimal invasive surgeries and rising number of sports medical centres

- 3.2.1.4 Increasing awareness regarding physical fitness and sports activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of trained healthcare professional in developing countries

- 3.2.2.2 Inflated cost of sports medicine

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in telehealth and remote rehabilitation services, enabling hybrid care models.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Body reconstruction products

- 5.2.1 Orthopedic implants

- 5.2.2 Fracture and ligament repair products

- 5.2.3 Arthroscopy devices

- 5.2.4 Soft tissue repair products

- 5.2.5 Prosthetics

- 5.2.6 Orthobiologics

- 5.3 Body support & recovery

- 5.3.1 Braces and supports

- 5.3.2 Compression clothing

- 5.3.3 Physiotherapy equipment

- 5.3.4 Thermal therapy

- 5.3.5 Electrostimulation

- 5.3.6 Other body support & recovery products

- 5.4 Accessories

- 5.4.1 Bandages

- 5.4.2 Tapes

- 5.4.3 Disinfectants

- 5.4.4 Wraps

- 5.4.5 Other accessories

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Injury Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Knee injuries

- 6.3 Shoulder injuries

- 6.4 Foot and ankle injuries

- 6.5 Back and spine injuries

- 6.6 Hip and groin injuries

- 6.7 Other injuries

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Physiotherapy centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Stryker

- 9.2 Arthrex, Inc.

- 9.3 Wright Medical Technology

- 9.4 Otto Bock Healthcare

- 9.5 Zimmer Biomet

- 9.6 Smith & Nephew Plc

- 9.7 Breg, Inc.

- 9.8 Muller Sports, Inc.

- 9.9 RTI Surgical

- 9.10 Performance Health International Limited

- 9.11 KARL STORZ

- 9.12 Bauerfeind AG

- 9.13 CONMED Corporation

- 9.14 Johnson & Johnson

- 9.15 Ossur Corporate

- 9.16 Creamer Product, Inc.

- 9.17 DJO Global

- 9.18 Anika Therapeutics, Inc.

運動醫學市場規模、佔有率和成長分析:按產品類型、最終用戶、應用、分銷管道和地區分類-2026-2033年產業預測

運動醫學市場規模、佔有率和成長分析:按產品類型、最終用戶、應用、分銷管道和地區分類-2026-2033年產業預測 運動醫學市場:依產品類型、應用程式、最終用戶和通路分類-2026-2032年全球市場預測運動醫學與物理治療市場:依產品、運動項目、應用及最終用戶分類-2026-2032年全球市場預測

運動醫學市場:依產品類型、應用程式、最終用戶和通路分類-2026-2032年全球市場預測運動醫學與物理治療市場:依產品、運動項目、應用及最終用戶分類-2026-2032年全球市場預測 2026年全球運動醫學市場報告

2026年全球運動醫學市場報告 日本運動醫學市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年運動醫學市場規模、佔有率、趨勢及預測(按產品、應用、最終用戶及地區分類),2026-2034年

日本運動醫學市場規模、佔有率、趨勢和預測:按產品、應用、最終用戶和地區分類,2026-2034年運動醫學市場規模、佔有率、趨勢及預測(按產品、應用、最終用戶及地區分類),2026-2034年 運動醫學市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年

運動醫學市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、地區和競爭對手分類,2021-2031年 運動醫學市場:2025-2030 年預測

運動醫學市場:2025-2030 年預測 運動醫學市場規模、佔有率、趨勢分析報告:按產品類型、應用、地區、細分市場預測,2025-2033 年

運動醫學市場規模、佔有率、趨勢分析報告:按產品類型、應用、地區、細分市場預測,2025-2033 年 運動醫學市場評估:設備類型·用途·終端用戶·各地區的機會及預測 (2018-2032年)

運動醫學市場評估:設備類型·用途·終端用戶·各地區的機會及預測 (2018-2032年)