|

市場調查報告書

商品編碼

1998831

醫用床市場機會、成長要素、產業趨勢分析及2026-2035年預測。Medical Bed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

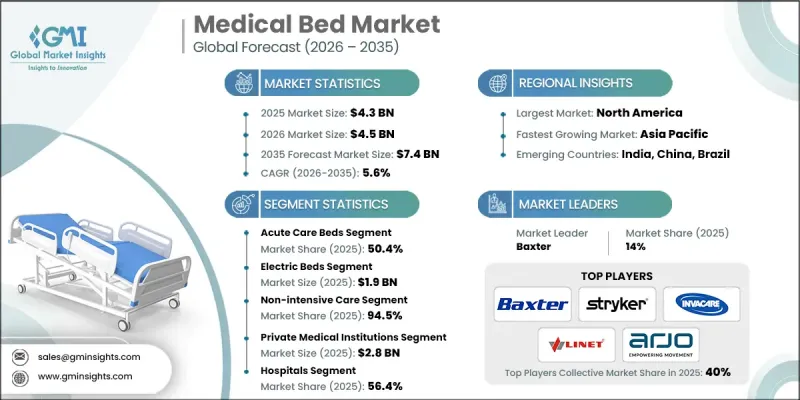

全球醫用床市場預計到 2025 年將價值 43 億美元,預計到 2035 年將以 5.6% 的複合年成長率成長至 74 億美元。

推動市場擴張的關鍵因素包括全球老年人口的成長、開發中國家醫療基礎設施投資的增加,以及慢性病和文明病導致的住院人數上升。新興市場的私人醫療機構正在迅速增加床位,以滿足不斷成長的患者群體、支持醫療旅遊並服務日益壯大的中產階級。醫院現代化建設以及重症監護室(ICU)和重症監護病房基礎設施的改善,進一步刺激了市場需求。私立醫院致力於提供高品質、舒適且標準化的床位解決方案,以提升病患體驗和品牌聲譽。對綜合醫院和連鎖醫院的需求不斷成長,推動了普通病房、重症監護室和復健病房床位的大規模採購。醫用床是專為醫院、療養院和居家照護環境設計的專用醫療設備,其功能旨在滿足患者照護、舒適度和復健需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 43億美元 |

| 預測金額 | 74億美元 |

| 複合年成長率 | 5.6% |

到2025年,急性護理病床市佔率將達到50.4%。這些病床主要用於內科和外科病房、急診科和重症監護室(ICU)的短期治療。全電動可調節急性護理病床因其便於患者體位調整、簡化臨床操作以及具備全天候監測功能而備受青睞。這些功能在現代醫療機構中需求旺盛,因為它們可以減輕看護者的負擔並節省時間。

預計2025年,電動床市場規模將達到19億美元。電動床採用馬達驅動機制,看護者可透過電子或手動控制面板調整患者的高度和體位,從而最大限度地減少看護者的工作量,同時提高患者的舒適度。這些床廣泛應用於醫院、長期照護機構和私人醫療機構。低位設定、體位鎖定功能以及與監測系統的整合等安全特性,提高了臨床療效和病人安全性。

預計到2025年,美國醫用床市場規模將達到15.7億美元,主要得益於先進的醫療基礎設施、較高的醫院床位更換率以及先進技術設備的普及應用。醫院正優先考慮床位升級,以提高病人安全、減輕看護者的工作負擔並支持以價值為導向的醫療服務模式。在急診和重症監護環境中,電動床、ICU床和智慧床的需求尤其旺盛。人口老化和慢性病盛行率的上升持續推動著住院治療和長期住院需求的成長,從而支撐著市場的穩定成長。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策及對資料完整性的承諾

- 資訊來源一致性通訊協定

- GMI人工智慧政策及對資料完整性的承諾

- 調查過程和可靠性評分

- 研究路徑的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 全球老化進程

- 增加對開發中國家醫療衛生基礎建設的投資

- 慢性病住院人數急遽增加。

- 開發中國家私立醫院床位數量的增加

- 產業潛在風險與挑戰

- 特殊病床高成本

- 機會

- 居家照護和遠端患者監護的快速發展

- 將物聯網和人工智慧技術應用於病床

- 促進因素

- 成長潛力分析

- 監理情勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 政策環境

- 供應鏈分析

- 智慧床功能基準測試

- 按床型分類的價格分析(基於初步調查)

- 租賃模式分析(基於初步研究)

- 對環境和永續發展的承諾

- 波特五力分析

- PESTEL 分析

- 差距分析

- 消費者洞察(基於初步研究)

- 未來市場趨勢(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析(基於初步研究)

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 主要市場參與者的競爭分析(基於初步研究)

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 急性期床

- 一般外科和內科病床

- 重症加護病床

- 兒童床

- 產床

- 其他急診室

- 長期照護床位

- 精神科病床

- 肥胖患者的床位

- 其他產品

第6章 市場估計與預測:依床型分類,2022-2035年

- 手動床

- 電動床

- 半電動床

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 重症監護

- 普通病房

第8章 市場估算與預測:依醫療機構分類,2022-2035年

- 私立醫療機構

- 公立醫療機構

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 居家照護設施

- 老年護理機構

- 其他最終用戶

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- ANTANO Group

- Arjo

- Baxter

- BESCO

- DiaMedical

- DRIVE DEVILBISS HEALTHCARE

- GENDRON

- HARD Manufacturing Company

- INVACARE

- LINET

- MALVESTIO

- Midmark

- PARAMOUNT BED

- Savaria

- STIEGELMEYER

- Stryker

- Umano Medical

The Global Medical Bed Market was valued at USD 4.3 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 7.4 billion by 2035.

The market expansion is driven by several key factors, including a rising global geriatric population, growing investments in healthcare infrastructure across developing nations, and increasing hospital admissions due to chronic and lifestyle-related illnesses. Private healthcare facilities in emerging markets are rapidly adding hospital beds to meet rising patient volumes, support medical tourism, and cater to the expanding middle-class population. ICU and critical care infrastructure improvements, along with hospital modernization initiatives, further stimulate demand. Private hospitals focus on offering high-quality, comfortable, and standardized bed solutions to enhance patient experience and brand reputation. Increasing demand for multispecialty hospitals and hospital chains has led to large-scale procurement of beds for general wards, ICUs, and recovery units. Medical beds are specialized healthcare equipment designed for hospitals, nursing homes, and home care settings, incorporating features that support patient care, comfort, and rehabilitation needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 5.6% |

The acute care beds segment held a 50.4% share in 2025. These beds are primarily used for short-term treatment of patients in medical-surgical units, emergency departments, and ICUs. Fully electric and adjustable acute care beds are preferred due to their ease of patient repositioning, simplified clinical procedures, and 24/7 monitoring capabilities. These features reduce caregiver stress and save time, making them highly sought after in modern healthcare facilities.

The electric beds segment reached USD 1.9 billion in 2025. Electric beds feature motorized mechanisms that allow caregivers to adjust patient height and position via electronic or hand controls, enhancing patient comfort while minimizing caregiver effort. These beds are widely used across hospitals, long-term care centers, and private healthcare facilities. Safety features such as low-height settings, lockable positions, and integration with monitoring systems enhance clinical effectiveness and patient security.

U.S. Medical Bed Market reached USD 1.57 billion in 2025, fueled by advanced healthcare infrastructure, high hospital bed replacement rates, and adoption of technologically advanced equipment. Hospitals prioritize bed upgrades to improve patient safety, reduce caregiver workload, and support value-based care initiatives. Demand for electric, ICU, and smart beds is especially strong in acute and critical care settings. An aging population and rising prevalence of chronic diseases continue to drive inpatient care and long-term hospitalization needs, supporting consistent market growth.

Key players in the Global Medical Bed Market include ANTANO Group, Arjo, Baxter, BESCO, DiaMedical, DRIVE DEVILBISS HEALTHCARE, GENDRON, HARD Manufacturing Company, INVACARE, LINET, MALVESTIO, Midmark, PARAMOUNT BED, Savaria, STIEGELMEYER, Stryker, and Umano Medical. Companies in the medical bed industry are strengthening their market presence through strategic innovation, global expansion, and partnerships with healthcare institutions. Manufacturers focus on developing advanced electric and smart beds with integrated monitoring and safety features to differentiate their offerings. Collaboration with hospitals and long-term care providers ensures product customization and adoption. R&D investments enable the creation of ergonomically designed, technologically advanced beds that improve patient outcomes and caregiver efficiency. Expanding distribution networks, entering emerging markets, and providing maintenance and training services further enhance market foothold.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Bed type trends

- 2.2.4 Application trends

- 2.2.5 Medical facilities trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population worldwide

- 3.2.1.2 Increasing funding on healthcare infrastructure in developing economies

- 3.2.1.3 Surging hospital admissions due to chronic diseases

- 3.2.1.4 Rising volume of hospital beds in private hospitals in developing countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of specialty beds

- 3.2.3 Opportunities

- 3.2.3.1 Rapid expansion of home care and remote patient monitoring

- 3.2.3.2 Integration of IoT and AI in patient beds

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy landscape

- 3.7 Supply chain analysis

- 3.8 Smart bed feature benchmarking

- 3.9 Pricing analysis by bed type (Driven by Primary Research)

- 3.10 Rental and leasing model analysis (Driven by Primary Research)

- 3.11 Environmental and sustainability initiatives

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Consumer insights (Driven by Primary Research)

- 3.16 Future market trends (Driven by Primary Research)

- 3.17 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players (Driven by Primary Research)

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Acute care beds

- 5.2.1 MedSurg beds

- 5.2.2 ICU beds

- 5.2.3 Pediatric beds

- 5.2.4 Birthing beds

- 5.2.5 Other acute care beds

- 5.3 Long-term care beds

- 5.4 Psychiatric care beds

- 5.5 Bariatric care beds

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Bed Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Manual beds

- 6.3 Electric beds

- 6.4 Semi-electric beds

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Intensive care

- 7.3 Non-intensive care

Chapter 8 Market Estimates and Forecast, By Medical Facilities, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Private medical institutions

- 8.3 Public medical institutions

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Home care settings

- 9.4 Elderly care facilities

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ANTANO Group

- 11.2 Arjo

- 11.3 Baxter

- 11.4 BESCO

- 11.5 DiaMedical

- 11.6 DRIVE DEVILBISS HEALTHCARE

- 11.7 GENDRON

- 11.8 HARD Manufacturing Company

- 11.9 INVACARE

- 11.10 LINET

- 11.11 MALVESTIO

- 11.12 Midmark

- 11.13 PARAMOUNT BED

- 11.14 Savaria

- 11.15 STIEGELMEYER

- 11.16 Stryker

- 11.17 Umano Medical

肥胖症患者病床市場:依產品類型、最終用戶、通路和應用分類-2026-2032年全球預測

肥胖症患者病床市場:依產品類型、最終用戶、通路和應用分類-2026-2032年全球預測 2026年全球醫用床市場報告

2026年全球醫用床市場報告 全球醫用床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醫用床市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 肥胖症患者病床市場-全球產業規模、佔有率、趨勢、機會、預測:承重能力、最終用途、地區和競爭格局,2021-2031年醫用床解決方案市場(按床型、技術、最終用戶和分銷管道分類)—2026-2032年全球預測

肥胖症患者病床市場-全球產業規模、佔有率、趨勢、機會、預測:承重能力、最終用途、地區和競爭格局,2021-2031年醫用床解決方案市場(按床型、技術、最終用戶和分銷管道分類)—2026-2032年全球預測 全球減肥床市場

全球減肥床市場 全球醫療床市場:成長、未來展望與競爭分析(2025-2033)全球醫療床市場:2024-2029 年預測

全球醫療床市場:成長、未來展望與競爭分析(2025-2033)全球醫療床市場:2024-2029 年預測 醫療床市場:依產品類型、最終用戶、地區:2024-2031 年全球產業分析、規模、佔有率、成長、趨勢、預測

醫療床市場:依產品類型、最終用戶、地區:2024-2031 年全球產業分析、規模、佔有率、成長、趨勢、預測