|

市場調查報告書

商品編碼

1998830

自行車機械碟煞市場機會、成長要素促進因素、產業趨勢分析及2026-2035年預測Bicycle Mechanical Disc Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

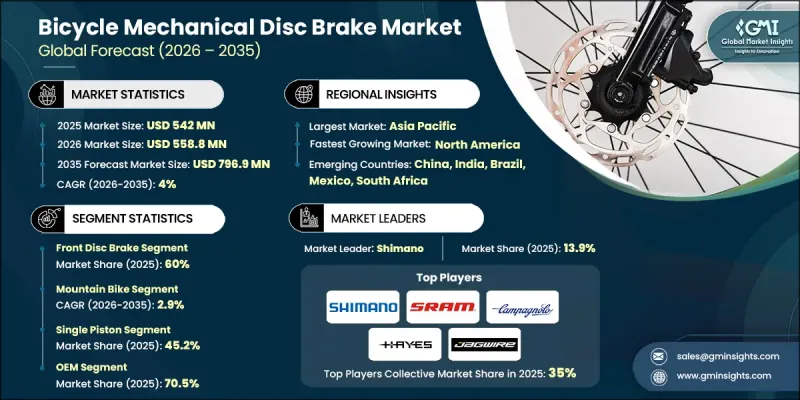

2025 年全球自行車機械碟煞市場規模預計為 5.42 億美元,預計到 2035 年將以 4% 的複合年成長率成長至 7.969 億美元。

全球自行車騎行人口的不斷成長推動了這個市場的發展,都市區通勤、休閒騎行以及日益普及的共享單車項目都促進了這一趨勢。隨著越來越多的城市將自行車納入永續交通規劃,自行車製造商和零件供應商正在為更多車型配備機械碟煞,以滿足日益嚴格的安全和性能標準。不斷增強的環保意識促使騎乘者選擇自行車而非汽車。電動自行車在日常通勤和休閒活動中的快速普及進一步提升了對機械碟煞的需求,因為機械碟煞在各種騎乘條件下都能提供可靠的煞車力道。煞車部件的技術創新也增強了機械碟煞的吸引力。轉子設計、線纜系統和材料的進步提高了耐磨性、散熱性和煞車控制性能,使機械系統即使面對價格更高的液壓系統也能保持競爭力。這些改進使製造商能夠實現產品差異化,並在通勤車、混合動力車、礫石公路車和山地自行車等細分市場中保持領先地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 5.42億美元 |

| 預測金額 | 7.969億美元 |

| 複合年成長率 | 4% |

預計到2025年,前輪碟煞市佔率將達到60%,並在2035年之前以3.4%的複合年成長率成長。前輪碟煞提供大部分煞車力,確保平穩的煞車控制、較短的煞車距離以及在乾濕路面上的可靠性能。為了滿足安全法規的要求,並為山地自行車、礫石路車、公路車、城市車和電動自行車等平台提供高性能煞車解決方案,前輪碟煞已成為整車製造商和零件供應商的首要任務。

預計到2025年,山地自行車市佔率將達到45.7%,並在2026年至2035年間以2.9%的複合年成長率成長。機械式碟煞對於越野路段、陡坡和崎嶇地形至關重要,因為即使在泥濘、潮濕和碎石遍布的路況下,它們也能提供穩定的煞車力道。這種可靠性使其成為山地自行車製造商、專業車手和越野騎行愛好者的必備之選。

預計到2025年,美國自行車機械碟煞市場規模將達到9,420萬美元。該地區的成長主要得益於製造商、電動自行車營運商和零件經銷商對先進煞車解決方案的採用。精密機械碟煞透過確保性能穩定、提升騎乘安全以及與最新車架標準的兼容性,降低了大規模生產市場中煞車失靈的風險。各公司也不斷改進碟片設計和模組化卡鉗平台,以最佳化傳統自行車和電動自行車的煞車性能。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球自行車使用量增加

- 日益增強的環保意識正在推動人們轉向更環保的交通途徑。

- 煞車部件的技術進步

- 政府支持自行車基礎設施的舉措

- 產業潛在風險與挑戰

- 激烈的競爭和對價格的敏感性

- 過渡到液壓碟式煞車

- 市場機遇

- 新興市場需求不斷成長

- 礫石自行車、混合動力自行車和通勤自行車的市場擴張

- 售後升級更換領域

- 都市區通勤和微出行日益成長的趨勢

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國消費品安全委員會(CPSC)

- ASTM國際標準 - 自行車標準(ASTM F2043 和 F1952)

- 加拿大:《加拿大消費品安全法》(CCPSA)

- 歐洲

- EN ISO 4210 - 自行車安全要求

- 歐盟通用產品安全指令(GPSD)/通用產品安全規範(GPSR)

- 亞太地區

- 中國:自行車零件GB標準(GB 3565)

- 印度:印度標準局 (BIS) - IS 1570 和 IS 15602

- 拉丁美洲

- 巴西:ABNT NBR 自行車標準

- 墨西哥:自行車安全NOM標準

- 中東和非洲

- 阿拉伯聯合大公國和海灣國家:ESMA產品安全法規

- 沙烏地阿拉伯:SASO自行車和消費品標準

- 非洲聯盟(非洲聯盟):非洲大陸消費者保護框架

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析(基於初步研究)

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按玩家類型分類的定價策略

- 貿易統計(基於付費資料庫)

- 生產基地

- 消費者群體

- 出口和進口

- 經營模式和獲利框架

- 收入模式

- 價值鍊和生態系統

- 打入市場策略

- 品質標準、合規性和產品風險

- 組件安全性和法規遵從性

- 與產品性能和耐用性相關的風險

- 營運和供應鏈風險

- 煞車系統架構

- 多部件煞車總成機型

- 自行車與基礎設施的融合,以及智慧運輸的融合

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 預測性維護和營運最佳化

- 自動化設計最佳化

- 用於需求預測的供應鏈人工智慧

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 利用人工智慧改造現有經營模式

- 永續性和環境方面

- 永續實踐

- 生產中的能源效率

- 碳足跡考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:煞車系統,2022-2035年

- 前輪碟煞

- 後輪碟煞

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 單活塞

- 雙活塞

- 4個活塞

- 多活塞

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 公路自行車

- 山地自行車

- 賽車

- 礫石自行車

第8章 市場估算與預測:依通路分類,2022-2035年

- OEM

- 售後市場

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 挪威

- 丹麥

- 荷蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 新加坡

- 馬來西亞

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Shimano

- SRAM

- Tektro/TRP(Tektro Racing Products)

- Magura

- Hayes Performance Systems

- Campagnolo

- Formula

- Jagwire

- Hope Technology

- Clarks Cycle Systems

- Promax

- 當地公司

- Nutt Technology

- MTX Braking

- Kool-Stop International

- Cane Creek

- EBC Brakes

- Galfer

- Paul Component Engineering

- Funn Components

- Alligator Cables

The Global Bicycle Mechanical Disc Brake Market was valued at USD 542 million in 2025 and is estimated to grow at a CAGR of 4% to reach USD 796.9 million by 2035.

The market is driven by rising global bicycle adoption, fueled by urban commuting, recreational cycling, and expanding bike-sharing programs. As more cities integrate cycling into sustainable transportation planning, bicycle manufacturers and component suppliers are equipping a wider range of models with mechanical disc brakes to meet increasing safety and performance standards. Growing environmental consciousness is encouraging riders to favor bicycles over motorized vehicles, while the rapid adoption of e-bikes for daily commuting and leisure activities further strengthens demand for mechanical disc brakes that provide dependable stopping power under varying riding conditions. Innovations in brake components are also enhancing the appeal of mechanical disc brakes. Advances in rotor design, cable systems, and materials improve wear resistance, heat dissipation, and braking modulation, keeping mechanical systems competitive against costlier hydraulic alternatives. These improvements allow manufacturers to differentiate products and maintain relevance across commuter, hybrid, gravel, and mountain bike segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $542 Million |

| Forecast Value | $796.9 Million |

| CAGR | 4% |

The front disc brake segment held a 60% share in 2025 and is expected to grow at a CAGR of 3.4% through 2035. Front disc brakes handle the majority of braking force, ensuring smooth modulation, shorter stopping distances, and reliable performance in both wet and dry conditions. Their integration is a top priority for OEMs and component suppliers aiming to meet safety regulations and deliver high-performance braking solutions across mountain, gravel, road, urban, and e-bike platforms.

The mountain bikes segment held a 45.7% share in 2025 and is forecasted to grow at a CAGR of 2.9% from 2026 to 2035. Mechanical disc brakes are essential for off-road trails, steep descents, and uneven terrain because they provide consistent stopping power in mud, water, and debris-laden conditions. This reliability makes them indispensable for mountain bike manufacturers, professional riders, and trail cycling enthusiasts.

U.S. Bicycle Mechanical Disc Brake Market reached USD 94.2 million in 2025. Growth in the region is driven by the adoption of advanced braking solutions by manufacturers, e-bike operators, and component distributors. Precision mechanical disc brakes ensure consistent performance, enhance rider safety, and maintain compatibility with modern frame standards, reducing brake failure risks in high-volume markets. Companies are also upgrading rotor designs and modular caliper platforms to optimize braking across both traditional and electric bicycles.

Major players operating in the Global Bicycle Mechanical Disc Brake Market include Shimano, SRAM, Campagnolo, Hayes, Jagwire, Magura, Cane Creek, Formula, Tektro, and Box Components. Key strategies adopted by companies in the Global Bicycle Mechanical Disc Brake Market include extensive R&D for improved rotor and caliper designs, developing lightweight and corrosion-resistant materials, and enhancing heat dissipation and modulation performance. Firms focus on expanding product portfolios across e-bikes, mountain, commuter, and hybrid segments to meet diverse customer needs. Strategic collaborations with bicycle OEMs and aftermarket distributors help integrate braking systems early in the design process. Market players also leverage marketing campaigns emphasizing safety, durability, and performance reliability, while establishing regional manufacturing hubs to improve supply chain efficiency, reduce costs, and strengthen global market presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Brake

- 2.2.3 Offering

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in bicycle adoption across the world

- 3.2.1.2 Environmental awareness encourages the shift to eco-friendly transport

- 3.2.1.3 Technological advancements in brake components

- 3.2.1.4 Government initiatives supporting cycling infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High competition and price sensitivity

- 3.2.2.2 Shift toward hydraulic disc brakes

- 3.2.3 Market opportunities

- 3.2.3.1 Growing Demand in Emerging Markets

- 3.2.3.2 Expansion of Gravel, Hybrid, and Commuter Bikes

- 3.2.3.3 Aftermarket Upgrades and Replacement Segment

- 3.2.3.4 Rising Urban Commuting and Micro-Mobility Trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Consumer Product Safety Commission (CPSC)

- 3.4.1.2 ASTM International - Bicycle Standards (ASTM F2043 & F1952)

- 3.4.1.3 Canada: Canada Consumer Product Safety Act (CCPSA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO 4210 - Safety Requirements for Bicycles

- 3.4.2.2 EU General Product Safety Directive (GPSD) / General Product Safety Regulation (GPSR)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: GB Standards for Bicycle Components (GB 3565)

- 3.4.3.2 India: Bureau of Indian Standards (BIS) - IS 1570 & IS 15602

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ABNT NBR Standards for Bicycles

- 3.4.4.2 Mexico: NOM Standards for Bicycle Safety

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States: ESMA Product Safety Regulations

- 3.4.5.2 Saudi Arabia: SASO Bicycle and Consumer Product Standards

- 3.4.5.3 African Union (AU): African Continental Consumer Protection Framework

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Trade statistics (Driven by Paid Database)

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Business Models and Monetization Framework

- 3.11.1 Revenue Models

- 3.11.2 Value Chain and Ecosystem

- 3.11.3 Go-to-Market Strategy

- 3.12 Quality Standards, Compliance, and Product Risk

- 3.12.1 Component Safety and Regulatory Compliance

- 3.12.2 Product Performance and Durability Risk

- 3.12.3 Operational and Supply Chain Risks

- 3.13 Braking System Architecture

- 3.13.1 Multi-Component Brake Assembly Models

- 3.13.2 Bicycle-to-Infrastructure and Smart Mobility Integration

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.1.1 Predictive Maintenance & Operations Optimization

- 3.14.1.2 Automated design optimization

- 3.14.1.3 Supply chain AI for demand forecasting

- 3.14.1.4 GenAI use cases & adoption roadmap by segment

- 3.14.1 AI-driven disruption of existing business models

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable Manufacturing Practices

- 3.15.2 Energy efficiency in production

- 3.15.3 Carbon footprint considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Brake, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front disc brake

- 5.3 Rear disc brake

Chapter 6 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Single piston

- 6.3 Dual piston

- 6.4 Four piston

- 6.5 Multi-piston

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Road bike

- 7.3 Mountain bike

- 7.4 Racing bike

- 7.5 Gravel bikes

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Norway

- 9.3.9 Denmark

- 9.3.10 Netherlands

- 9.3.11 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.4.9 Malaysia

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Shimano

- 10.1.2 SRAM

- 10.1.3 Tektro / TRP (Tektro Racing Products)

- 10.1.4 Magura

- 10.1.5 Hayes Performance Systems

- 10.1.6 Campagnolo

- 10.1.7 Formula

- 10.1.8 Jagwire

- 10.1.9 Hope Technology

- 10.1.10 Clarks Cycle Systems

- 10.1.11 Promax

- 10.2 Regional players

- 10.2.1 Nutt Technology

- 10.2.2 MTX Braking

- 10.2.3 Kool-Stop International

- 10.2.4 Cane Creek

- 10.2.5 EBC Brakes

- 10.2.6 Galfer

- 10.2.7 Paul Component Engineering

- 10.2.8 Funn Components

- 10.2.9 Alligator Cables

汽車碟式煞車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

汽車碟式煞車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測 汽車煞車碟盤市場:依產品類型、材料、車輛類型、銷售通路、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測

汽車煞車碟盤市場:依產品類型、材料、車輛類型、銷售通路、國家及地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測 汽車碟式煞車市場分析及預測(至2034年):類型、產品、技術、組件、材料類型、應用、最終用戶、能力、安裝類型、解決方案

汽車碟式煞車市場分析及預測(至2034年):類型、產品、技術、組件、材料類型、應用、最終用戶、能力、安裝類型、解決方案 2032 年汽車碟式煞車市場預測:按類型、材料、車輛類型、技術、銷售管道、應用和地區進行的全球分析

2032 年汽車碟式煞車市場預測:按類型、材料、車輛類型、技術、銷售管道、應用和地區進行的全球分析 全球汽車碟式煞車市場

全球汽車碟式煞車市場 自行車液壓碟式煞車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

自行車液壓碟式煞車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 開槽煞車盤的全球市場:實際成果與預測(2019年~2030年)

開槽煞車盤的全球市場:實際成果與預測(2019年~2030年)