|

市場調查報告書

商品編碼

1998829

實驗室設備市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Laboratory Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

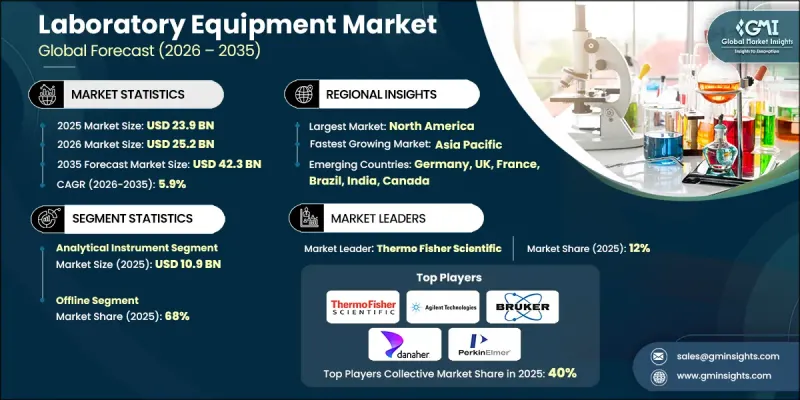

預計到 2025 年,全球實驗室設備市場價值將達到 239 億美元,並以 5.9% 的複合年成長率成長,到 2035 年將達到 423 億美元。

對科學研究,特別是藥物研發、生物技術創新和生命科學探索領域的投資不斷增加,顯著推動了對先進實驗室設備的需求。公共和私營機構都在科學發現、治療方法研究和生物醫學進步方面投入大量資源,而所有這些都需要能夠提供高度精確分析結果的精確工具。開發中地區實驗室基礎設施的擴張也促進了設備需求的成長,因為這些國家優先發展以創新主導的經濟策略。同時,科技的快速發展正透過引入自動化、機器人和人工智慧驅動的診斷系統來重塑實驗室運作。這些技術可幫助實驗室提高營運效率、增強擴充性並降低人工操作帶來的風險。此外,數位監控技術和連網設備的整合使實驗室能夠在多個研究環境中進行遠端監控、預測性維護和進階資料管理。對科學創新的日益關注、實驗室技術的持續改進以及醫學研究活動的活性化,共同推動全球檢測設備市場的變革,並增強了臨床、學術和工業實驗室的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 239億美元 |

| 預計金額 | 423億美元 |

| 複合年成長率 | 5.9% |

預計到2025年,分析儀器市場規模將達到109億美元。該細分市場持續推動整個產業的發展,因為分析儀器在實現精確測量和支持先進科學研究方面發揮著至關重要的作用。高精度儀器對於眾多科學領域的實驗室分析、實驗檢驗和法規遵循至關重要。它們能夠產生可靠的分析數據,使其成為現代實驗室環境中不可或缺的工具。隨著監管機構對研究準確性和品管的要求不斷提高,先進分析儀器的重要性仍然是實驗室儀器市場成長的核心驅動力。

2025年,線下通路將佔據68%的市場。傳統分銷網路在直接為實驗室提供技術專長和專業客戶支援方面仍然發揮著至關重要的作用。供應商和經銷商在設備交付、安裝管理以及為複雜的實驗室設備提供維護服務方面扮演著舉足輕重的角色。由於科學儀器高度專業化且高成本,科研機構、醫療機構和工業實驗室往往更傾向於透過能夠保證可靠服務合約和技術支援的線下管道進行採購。這種方式使客戶能夠獲得關於安裝、校準、維修服務和客製化設備配置的專家指導。

預計到2025年,美國實驗室設備市場佔有率將達到69.3%,這得益於其完善的研究生態系統、數位化實驗室技術的廣泛應用以及對高效實驗室工作流程的強勁需求。美國實驗室設備產業的特點是高度自動化、精密測量儀器和嚴格的合規標準。生物技術、製藥和診斷研究領域的持續需求推動實驗室技術和工作流程最佳化系統的持續創新。此外,該地區還擁有完善的基礎設施,包括先進的物流網路、專業的技術支援服務以及能夠管理複雜實驗室操作的高技能人才。這些因素使得公共和私營研究機構能夠快速部署、維護和擴展實驗室能力。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 活性化研發活動

- 技術進步

- 慢性病增多

- 產業潛在風險與挑戰

- 巨額資本投資

- 監理和合規挑戰

- 機會

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 按地區

- 透過裝置

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 專利趨勢(基於初步調查)

- 按技術領域分類的專利申請趨勢

- 專利的地理分佈

- 主要專利擁有者及其智慧財產權策略分析

- 波特五力分析

- PESTEL 分析

- 貿易數據分析(基於初步調查)

- 進出口數量和價值趨勢(基於初步調查)

- 主要貿易路線及關稅的影響(基於初步調查)

- 對貿易政策和本地化趨勢的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商裝置容量(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依設備類型分類,2021-2034年

- 分析設備

- 光譜儀(紫外-可見光光譜儀、紅外光譜儀、核磁共振波譜儀、質譜儀)

- 層析法設備(高效液相層析儀、氣相層析儀)

- 顯微鏡(光學顯微鏡、電子顯微鏡)

- pH計/電導率計

- 天平/稱重設備

- 實驗室設備

- 培養箱

- 離心機

- 水質淨化系統

- 高壓釜/消毒器

- 冷藏庫和冷凍庫

- 其他

第6章 市場估算與預測:依自動化程度分類,2021-2034年

- 手動的

- 半自動

- 自動的

第7章 市場估計與預測:依應用領域分類,2021-2034年

- 醫學和臨床檢查室

- 製藥和生物技術研究所

- 食品和飲料檢查

- 化學和材料測試

- 學術和教育實驗室

- 其他(學術/研究機構、環境)

第8章 市場估算與預測:依最終用途產業分類,2021-2034年

- 衛生保健

- 食品/飲料

- 製藥

- 學術和研究機構

- 化學品

- 其他(獸醫等)

第9章 市場估價與預測:依通路分類,2021-2034年

- 線上

- 離線

第10章 市場估價與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 3M

- Abbott Laboratories

- Agilent Technologies

- Atom Scientific Industries

- Beckton Dickinson

- Bruker Corporation

- Danaher Corporation

- GEA

- Labman Scientific Instruments

- PerkinElmer

- Roche

- Sartorius

- Siemens Healthineers

- Thermo Fisher Scientific

- Waters Corporation

The Global Laboratory Equipment Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 42.3 billion by 2035.

Increasing investment in scientific research, particularly in pharmaceutical development, biotechnology innovation, and life science exploration, is creating significant demand for advanced laboratory equipment. Public institutions and private organizations are allocating substantial resources toward scientific discovery, therapeutic research, and biomedical advancements, which require sophisticated tools capable of delivering highly accurate analytical results. The expansion of laboratory infrastructure in developing regions is also contributing to rising equipment demand as countries prioritize innovation-driven economic strategies. At the same time, rapid technological advancements are reshaping laboratory operations through the adoption of automation, robotics, and artificial intelligence-enabled diagnostic systems. These technologies are helping laboratories achieve greater operational efficiency, improved scalability, and reduced risks associated with manual processes. Additionally, the integration of digital monitoring technologies and connected devices allows laboratories to perform remote monitoring, predictive maintenance, and advanced data management across multiple research environments. Growing attention toward scientific innovation, continuous improvements in laboratory technology, and increasing healthcare research activities are collectively transforming the global laboratory equipment market while strengthening demand across clinical, academic, and industrial laboratories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $42.3 Billion |

| CAGR | 5.9% |

The analytical instrument segment accounted for USD 10.9 billion in 2025. This segment continues to dominate the industry because analytical instruments play a critical role in delivering accurate measurements and supporting advanced scientific research. High-precision instruments are essential for laboratory analysis, experimental validation, and regulatory compliance across numerous scientific fields. Their ability to produce reliable analytical data makes them fundamental tools in modern laboratory environments. As regulatory expectations surrounding research accuracy and quality control continue to increase, the importance of advanced analytical instruments remains central to the growth of the laboratory equipment market.

The offline distribution segment held 68% share in 2025. Traditional distribution networks remain highly relevant because they provide laboratories with direct access to technical expertise and specialized customer support. Suppliers and distributors play a vital role in delivering equipment, managing installation processes, and providing maintenance services for complex laboratory instruments. Due to the sophisticated nature and high cost associated with scientific equipment, research institutions, healthcare organizations, and industrial laboratories often prefer purchasing through offline channels that ensure dependable service agreements and technical assistance. This approach allows customers to access professional guidance for installation, calibration, repair services, and customized equipment configuration.

United States Laboratory Equipment Market held 69.3% share in 2025, supported by a well-established research ecosystem, extensive adoption of digital laboratory technologies, and strong demand for efficient laboratory workflows. The laboratory equipment industry in the United States is characterized by a high level of automation, precision-driven instrumentation, and strict compliance standards. Continuous demand from the biotechnology, pharmaceutical, and diagnostic research sectors is encouraging ongoing innovation in laboratory technologies and workflow optimization systems. Additionally, the region benefits from a robust infrastructure that includes advanced logistics networks, specialized technical support services, and a highly skilled workforce capable of managing complex laboratory operations. These factors enable research facilities across both public and private sectors to rapidly deploy, maintain, and scale laboratory capabilities.

Major companies operating in the Global Laboratory Equipment Market include 3M, Abbott Laboratories, Agilent Technologies, Atom Scientific Industries, Beckton Dickinson, Bruker Corporation, Danaher Corporation, GEA, Labman Scientific Instruments, PerkinElmer, Roche, Sartorius, Siemens Healthineers, Thermo Fisher Scientific, and Waters Corporation. Companies competing in the Global Laboratory Equipment Market are focusing on several strategic initiatives to strengthen their competitive position and expand their global reach. Many organizations are investing heavily in research and development to introduce advanced laboratory technologies that enhance precision, automation, and data integration capabilities. Product innovation centered on intelligent laboratory systems, connected instruments, and digital workflow management tools is becoming a key competitive differentiator. Leading companies are also expanding manufacturing capacity and strengthening global distribution networks to improve product accessibility across emerging and established markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation (Driven by Primary Research)

- 1.7.1 Primary sources

- 1.7.2 Expert Validation Protocol

- 1.7.3 Region-Specific Primary Interviews

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.1.1 North America

- 2.2.1.2 Europe

- 2.2.1.3 Asia-Pacific

- 2.2.1.4 Middle East and Africa

- 2.2.1.5 Latin America

- 2.2.2 Equipment type

- 2.2.3 Automation level

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.2.1 Regional

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising R&D activities

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Regulatory and compliance challenges

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.6.3 By region

- 3.6.4 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.8.1 Patent Filing Trends by Technology Area

- 3.8.2 Geographic Distribution of Patents

- 3.8.3 Key Patent Holders & IP Strategy Analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by Primary Research)

- 3.11.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11.3 Trade Policy Implications & Localization Trends

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Analytical instruments

- 5.2.1 Spectrometers (UV-Vis, IR, NMR, mass spectrometers)

- 5.2.2 Chromatography equipment (HPLC, GC)

- 5.2.3 Microscopes (optical, electron)

- 5.2.4 pH meters & conductivity meters

- 5.2.5 Balances & weighing equipment

- 5.3 Laboratory instruments

- 5.3.1 Incubators & ovens

- 5.3.2 Centrifuges

- 5.3.3 Water purification systems

- 5.3.4 Autoclaves & sterilizers

- 5.3.5 Refrigerators & freezers

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Automation Level, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Medical & clinical laboratories

- 7.3 Pharmaceutical & biotechnology laboratories

- 7.4 Food & beverage testing

- 7.5 Chemical & material testing

- 7.6 Academic & educational laboratories

- 7.7 Others (academic/research institutions, environmental)

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2021 - 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Healthcare

- 8.3 Food and beverages

- 8.4 Pharmaceuticals

- 8.5 Academic/research institutions

- 8.6 Chemicals

- 8.7 Others (Veterinary, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Abbott Laboratories

- 11.3 Agilent Technologies

- 11.4 Atom Scientific Industries

- 11.5 Beckton Dickinson

- 11.6 Bruker Corporation

- 11.7 Danaher Corporation

- 11.8 GEA

- 11.9 Labman Scientific Instruments

- 11.10 PerkinElmer

- 11.11 Roche

- 11.12 Sartorius

- 11.13 Siemens Healthineers

- 11.14 Thermo Fisher Scientific

- 11.15 Waters Corporation

翻新實驗室設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

翻新實驗室設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 實驗室設備市場規模、佔有率和成長分析:按產品類型、應用、技術、採購方式、最終用戶和地區分類-2026-2033年產業預測

實驗室設備市場規模、佔有率和成長分析:按產品類型、應用、技術、採購方式、最終用戶和地區分類-2026-2033年產業預測 實驗室一次性用品市場:2026-2032年全球市場預測(按產品類型、材料、滅菌方法、最終用戶、分銷管道和應用分類)實驗室設備及服務市場:2026-2032年全球市場預測(依服務類型、設備類型、定價模式、最終用途及銷售管道)實驗室培養板處理系統市場:按類型、功能、應用、分銷管道和最終用戶分類-2026-2032年全球市場預測

實驗室一次性用品市場:2026-2032年全球市場預測(按產品類型、材料、滅菌方法、最終用戶、分銷管道和應用分類)實驗室設備及服務市場:2026-2032年全球市場預測(依服務類型、設備類型、定價模式、最終用途及銷售管道)實驗室培養板處理系統市場:按類型、功能、應用、分銷管道和最終用戶分類-2026-2032年全球市場預測 實驗室設備及耗材市場報告:依產品類型、最終用途及地區分類,2026-2034年實驗室瓶蓋分配器市場:2026-2032年全球市場預測(依最終用戶、應用、產品類型、容量範圍和分銷管道分類)實驗室設備市場:全球市場按產品類型、最終用戶、設備類型和應用分類的預測,2026-2032年

實驗室設備及耗材市場報告:依產品類型、最終用途及地區分類,2026-2034年實驗室瓶蓋分配器市場:2026-2032年全球市場預測(依最終用戶、應用、產品類型、容量範圍和分銷管道分類)實驗室設備市場:全球市場按產品類型、最終用戶、設備類型和應用分類的預測,2026-2032年 全球拖鞋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)耐腐蝕不鏽鋼水泵市場:按泵浦類型、最終用戶、分銷管道和應用分類,全球預測(2026-2032年)

全球拖鞋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)耐腐蝕不鏽鋼水泵市場:按泵浦類型、最終用戶、分銷管道和應用分類,全球預測(2026-2032年)