|

市場調查報告書

商品編碼

1998824

車輛掃描器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Vehicle Scanner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

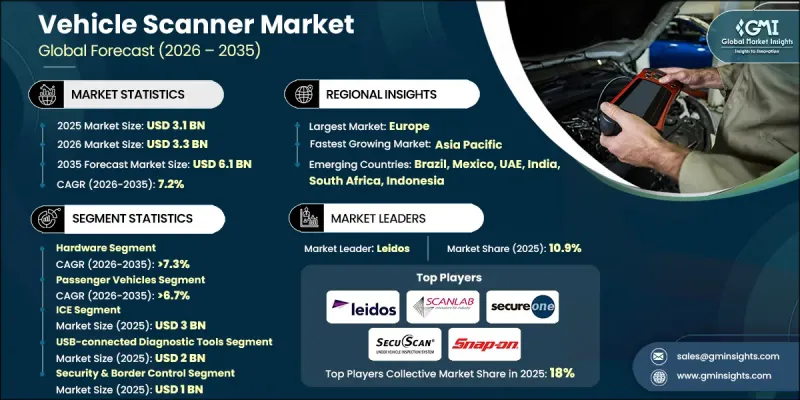

全球車輛掃描儀市場預計到 2025 年將價值 31 億美元,預計到 2035 年將以 7.2% 的複合年成長率成長至 61 億美元。

全球安全情勢日益嚴峻、物流基礎設施不斷擴張,以及打擊走私、恐怖主義和車載爆炸物等威脅的需求不斷成長,是推動市場成長的主要因素。各國政府、國防機構、關鍵基礎設施營運商和私人企業都在投資先進的車輛偵測技術,以提高安全性、加強合規性並簡化檢查站操作。智慧城市、城市交通網路和保全升級的商業設施的快速發展,進一步推動了自動化和人工智慧驅動的車輛掃描系統的應用。邊境管制、國防安全保障、機場和物流業者面臨越來越大的壓力,需要提高威脅偵測的準確性、縮短檢查時間並最大限度地減少營運中斷,這加速了市場需求。現代車輛掃描器提供非侵入式偵測、底盤威脅偵測、自動車牌辨識 (ALPR) 和即時分析功能。高能量 X 光成像、3D 平台、人工智慧驅動的異常檢測、雲端連接以及整合指揮控制軟體等創新技術正在重新定義全球傳統的檢測流程。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 31億美元 |

| 預計金額 | 61億美元 |

| 複合年成長率 | 7.2% |

預計到2025年,硬體部分將佔據59%的市場佔有率,並在2035年之前以7.3%的複合年成長率成長。硬體在高解析度影像處理、精準威脅偵測和提升營運效率方面繼續發揮至關重要的作用。部署在邊境、港口、物流樞紐和關鍵基礎設施的固定式、移動式和免下車掃描系統依賴X光掃描器、紫外線掃描系統(UVSS)、多感測器成像單元和免下車平台等組件,以確保可靠的性能和合規性。

預計到2025年,乘用車市佔率將達到76%,並在2035年之前以6.7%的複合年成長率成長。為因應邊防安全問題和非侵入式偵測需求,乘用車、SUV和混合動力汽車的安檢系統正被廣泛部署。固定式X光掃描儀、UVSS和人工智慧分析等先進技術的應用,以及標準化掃描通訊協定的推廣,正在鞏固北美、歐洲和亞太地區乘用車應用領域的主導地位。

預計到2025年,歐洲車輛掃描器市場規模將達到2.489億美元,佔21%的市佔率。該地區成熟的安全基礎設施、強大的物流網路以及行動式、固定式和免下車式掃描解決方案的普及,是推動市場強勁需求的主要因素。各國政府和關鍵基礎設施營運商都高度重視營運效率、威脅偵測準確性、合規性以及人工智慧分析技術的整合。嚴格的安全法規、先進的研發投入以及對標準化的堅持,進一步鞏固了歐洲的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加強邊防安全和打擊走私

- 關鍵基礎設施保護的成長

- 全球貿易和物流網路的擴張

- 人工智慧和影像處理技術的進步

- 產業潛在風險與挑戰

- 高昂的初始成本和維修成本

- 對法規和輻射合規性的擔憂

- 市場機遇

- 行動式和可攜式掃描器的迅速普及

- 智慧城市與人工智慧一體化安全平台

- 行動和可攜式掃描解決方案

- 電動和混合動力汽車汽車的普及

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國:EPA、CARB、NHTSA 標準

- 加拿大:加拿大運輸部和加拿大邊境服務局 (CBSA) 的標準

- 歐洲

- 德國:BMI、BMDV 標準

- 法國:內政部標準

- 英國:內政部和運輸部(DfT) 的標準

- 義大利:基礎設施和運輸部製定的標準

- 亞太地區

- 中國:公共安全和工業和資訊化部(工信部)標準

- 日本:國土交通省標準

- 韓國:行政安全部所訂定的標準

- 印度:MoRTH指南

- 拉丁美洲

- 巴西:DENATRAN 標準

- 墨西哥:交通運輸部部所訂定的標準

- 中東和非洲

- 阿拉伯聯合大公國:RTA 和 ESMA 標準

- 2. 沙烏地阿拉伯:運輸部,SASO 標準

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 區域價格波動分析

- 成本細分分析

- 專利趨勢(基於初步調查)

- 人工智慧(AI)的影響

- 利用人工智慧改造現有經營模式

- 人工智慧在預測性維護和車隊管理的應用

- 自動化設計最佳化

- 用於需求預測的供應鏈人工智慧

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 使用案例場景

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 硬體

- 掃描器

- 程式碼讀取器

- 胎壓監測系統工具

- 電池分析儀

- 數位壓力表

- 萬用電表和電工測試儀

- 其他

- 軟體

- ECU診斷和編程軟體

- 車輛追蹤和車隊管理軟體

- 排放分析軟體

- 車輛系統測試和調整軟體

- 基於雲端的診斷平台

- 服務

- 車輛保養及維修服務

- 客製化培訓和技術人員認證

- 技術支援和整合服務

- 基於訂閱的軟體更新服務

第6章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第7章 市場估計與預測:以連結方式分類,2022-2035年

- USB連接的診斷工具

- 具備藍牙功能的診斷工具

- Wi-Fi 相容性診斷工具

第8章 市場估計與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- 混合動力汽車

- 電動車(EV)

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 安全和邊境管制

- 關鍵基礎設施保護

- 商業的

- 停車設施

- 物流中心

- 娛樂中心

- 其他

- 活動管理

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第11章:公司簡介

- Global Player

- BorgWarner

- Denso

- Gatekeeper Security

- Leidos

- Omnitec

- Robert Bosch

- Scanlab

- SecureOne

- SecuScan

- Snap-On

- Regional Player

- Artec Security Systems

- Astrophysics

- Autoscope Technologies

- EvoScan Technologies

- Nuctech Company

- ProVision Systems

- Rapiscan Systems

- Smith Detection

- Votex Security

- VTI Security Solutions

The Global Vehicle Scanner Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 6.1 billion by 2035.

The market growth is driven by rising global security concerns, the expansion of logistics infrastructure, and the growing need to counter threats such as smuggling, terrorism, and vehicle-borne explosives. Governments, defense organizations, critical infrastructure operators, and private enterprises are investing in advanced vehicle inspection technologies to enhance safety, improve regulatory compliance, and streamline checkpoint operations. The rapid development of smart cities, urban transportation networks, and high-security commercial facilities is further boosting the adoption of automated and AI-enabled vehicle scanning systems. Increasing pressure on border control, homeland security, airports, and logistics operators to improve threat detection accuracy, reduce inspection times, and minimize operational disruption is accelerating demand. Modern vehicle scanners offer non-intrusive inspection, under-vehicle threat detection, automated license plate recognition (ALPR), and real-time analytics. Innovations such as high-energy X-ray imaging, 3D platforms, AI-powered anomaly detection, cloud connectivity, and integrated command-and-control software are redefining traditional inspection processes worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 7.2% |

The hardware segment held 59% share in 2025 and is expected to grow at a CAGR of 7.3% through 2035. Hardware remains critical for high-resolution imaging, accurate threat detection, and operational efficiency. Fixed, mobile, and drive-through scanning systems deployed at borders, ports, logistics hubs, and critical infrastructure rely on components like X-ray scanners, UVSS, multi-sensor imaging units, and drive-through platforms to deliver reliable performance and regulatory compliance.

The passenger vehicles segment held 76% share in 2025 and is projected to grow at a CAGR of 6.7% through 2035. Security and inspection systems for personal cars, SUVs, and hybrid vehicles are widely deployed to address border security concerns and non-intrusive inspection requirements. The adoption of advanced technologies such as fixed X-ray scanners, UVSS, and AI-enabled analytics, along with standardized scanning protocols, reinforces the leadership of passenger vehicle applications in North America, Europe, and Asia Pacific.

Europe Vehicle Scanner Market reached USD 248.9 million in 2025, holding 21% share. The region's mature security infrastructure, robust logistics networks, and adoption of mobile, fixed, and drive-through scanning solutions support high demand. Governments and critical infrastructure operators focus on operational efficiency, threat detection accuracy, regulatory compliance, and AI-enabled analytics integration. Strong security regulations, advanced R&D, and standardization efforts further strengthen Europe's market position.

Key companies driving the Global Vehicle Scanner Market include BorgWarner, Denso Corporation, Robert Bosch, Leidos, Gatekeeper Security, Omnitec, Snap-On, Scanlab, SecureOne, and SecuScan. Companies in the Vehicle Scanner Market are implementing several strategies to strengthen their presence and market foothold. They are investing heavily in AI, machine learning, and advanced sensor technologies to improve threat detection and real-time analytics. Partnerships with governments, defense agencies, and critical infrastructure operators enable collaboration on custom scanning solutions and integrated security platforms. Firms are also focusing on developing scalable, modular systems suitable for different vehicle types and operational scenarios. Expanding geographically, enhancing after-sales support, and offering cloud-connected monitoring services are key strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Vehicle

- 2.2.4 Connectivity

- 2.2.5 Propulsion

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Border Security & Anti-Smuggling Measures

- 3.2.1.2 Growth in Critical Infrastructure Protection

- 3.2.1.3 Expansion of Global Trade & Logistics Networks

- 3.2.1.4 Technological Advancements in AI & Imaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Installation & Maintenance Costs

- 3.2.2.2 Regulatory & Radiation Compliance Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid Adoption of Mobile & Portable Scanners

- 3.2.3.2 Smart City & AI-Based Integrated Security Platforms

- 3.2.3.3 Mobile and portable scanning solutions

- 3.2.3.4 Electric and hybrid vehicle adaptation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CBSA Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: BMI, BMDV Standards

- 3.4.2.2 France: Ministry of the Interior Standards

- 3.4.2.3 UK: Home Office, DfT Standards

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Public Security, MIIT Standards

- 3.4.3.2 Japan: MLIT Standards

- 3.4.3.3 South Korea: Ministry of the Interior and Safety Standards

- 3.4.3.4 India: MoRTH Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport Standards

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Standards

- 3.4.5. 2 Saudi Arabia: Ministry of Transport, SASO Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.8.3 Regional Price Variation Analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of Artificial Intelligence (AI)

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Predictive maintenance & fleet management AI

- 3.11.3 Automated design optimization

- 3.11.4 Supply chain AI for demand forecasting

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and Environmental Aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Scanners

- 5.2.2 Code Readers

- 5.2.3 TPMS Tools

- 5.2.4 Battery Analyzers

- 5.2.5 Digital Pressure Testers

- 5.2.6 Multimeters & Electrical Testers

- 5.2.7 Others

- 5.3 Software

- 5.3.1 ECU Diagnosis & Programming Software

- 5.3.2 Vehicle Tracking & Fleet Management Software

- 5.3.3 Emission Analysis Software

- 5.3.4 Vehicle System Testing & Calibration Software

- 5.3.5 Cloud-Based Diagnostic Platforms

- 5.4 Services

- 5.4.1 Vehicle Maintenance & Repair Services

- 5.4.2 Custom Training & Technician Certification

- 5.4.3 Technical Support & Integration Services

- 5.4.4 Subscription-Based Software Update Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 USB-Connected Diagnostic Tools

- 7.3 Bluetooth-Enabled Diagnostic Tools

- 7.4 Wi-Fi-Enabled Diagnostic Tools

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Hybrid Vehicles

- 8.4 Electric Vehicles (EVs)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Security & border control

- 9.3 Critical infrastructure protection

- 9.4 Commercial

- 9.4.1 Parking facilities

- 9.4.2 Logistics hubs

- 9.4.3 Entertainment centers

- 9.4.4 Others

- 9.5 Event management

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 BorgWarner

- 11.1.2 Denso

- 11.1.3 Gatekeeper Security

- 11.1.4 Leidos

- 11.1.5 Omnitec

- 11.1.6 Robert Bosch

- 11.1.7 Scanlab

- 11.1.8 SecureOne

- 11.1.9 SecuScan

- 11.1.10 Snap-On

- 11.2 Regional Player

- 11.2.1 Artec Security Systems

- 11.2.2 Astrophysics

- 11.2.3 Autoscope Technologies

- 11.2.4 EvoScan Technologies

- 11.2.5 Nuctech Company

- 11.2.6 ProVision Systems

- 11.2.7 Rapiscan Systems

- 11.2.8 Smith Detection

- 11.2.9 Votex Security

- 11.2.10 VTI Security Solutions