|

市場調查報告書

商品編碼

1998811

升糖素市場機會、成長要素、產業趨勢分析及2026-2035年預測Glucagon Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

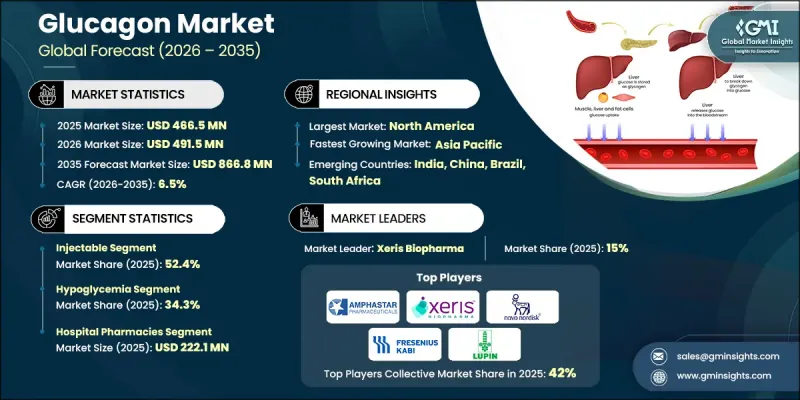

2025 年全球升糖素市值為 4.665 億美元,預計到 2035 年將以 6.5% 的複合年成長率成長至 8.668 億美元。

市場擴張的促進因素是糖尿病盛行率的上升和低血糖發作頻率的增加,這持續對全球醫療保健帶來沉重負擔。除了糖尿病相關緊急情況所帶來的需求成長外,升糖素給藥系統的創新也正在改變市場格局。糖尿病護理領域正日益採用由數位健康生態系統支援的整合、自動化和以患者為中心的解決方案。升糖素製劑的進步正在革新嚴重低血糖的治療,使其從多步驟的配製試劑盒轉變為即用型、穩定且便捷的選擇。穩定的液體升糖素製劑現在可以在室溫下儲存,並透過自動注射器或預填充式注射器,無需複雜的配製步驟。這些創新縮短了給藥時間,提高了看護者和急救人員的便利性,並增加了在嚴重低血糖發作期間獲得適當治療的可能性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 4.665億美元 |

| 預計金額 | 8.668億美元 |

| 複合年成長率 | 6.5% |

到2025年,注射劑藥物將佔據52.4%的市場。注射用胰高升糖素對於預防嚴重低血糖引起的癲癇發作、意識喪失或長期神經損傷至關重要,因為它通常在幾分鐘內即可起效。注射劑藥物給藥途徑柔軟性,包括皮下、肌肉和靜脈注射,從而能夠在家庭、診所和醫院等各種環境中實現以患者為中心的治療。這種適應性滿足了不同患者的需求和緊急醫療要求,使該細分市場能夠保持主導地位。

預計到2025年,醫院藥局市場規模將達到2.221億美元,確保急診室、加護病房和檢查室中升糖素的持續供應和安全使用。醫院藥劑師負責監督升糖素的正確儲存、配製和使用,維持其穩定性,並訓練護理人員和輔助人員在緊急情況下正確使用。這些場所也是重要的教育中心,強調準確劑量、給藥程序和治療後監測,以確保病人安全。

2025年,北美胰升糖素市場佔最大佔有率。這主要得益於先進的醫療基礎設施、糖尿病急救治療方法的高普及率以及速效升糖素製劑的廣泛應用。完善的醫院網路、便捷的藥房管道以及健全的法規結構,為創新型升糖素產品的快速分銷和核准提供了有力支持。醫院藥房將胰升糖素作為重要的急救藥物進行管理,確保其在嚴重低血糖的即時應對、兒童劑量配製以及診斷程序中的應用。零售藥局和線上藥局則作為醫院分銷的補充,為病患提供方便的處方胰高升糖素家用購買管道。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 全球糖尿病盛行率正在上升。

- 胰升糖素給藥方法的技術進步

- 研發活動活性化

- 產業潛在風險與挑戰

- 藥物高成本

- 與升糖素相關的副作用

- 市場機遇

- 擴大緊急應變系統的應用範圍

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術格局

- 目前技術

- 新興技術

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 注射藥物

- 吸入劑

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 低血糖

- 診斷輔助

- 消化系統疾病

- 心源性休克

- 其他用途

第7章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Amphastar Pharmaceuticals

- Avalon Pharma

- Eli Lilly and Company

- Fresenius Kabi

- Hanmi Pharmaceutical

- Lupin Limited

- Novo Nordisk A/S

- Taj Pharmaceuticals

- Xeris Biopharma Holdings

- Zealand Pharma

The Global Glucagon Market was valued at USD 466.5 million in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 866.8 million by 2035.

Market expansion is fueled by the rising prevalence of diabetes and the increasing frequency of hypoglycemic episodes, which continue to impose a significant healthcare burden worldwide. Beyond the growing demand driven by diabetes-related emergencies, innovations in glucagon delivery systems are reshaping the market landscape. The diabetes care sector is increasingly adopting integrated, automated, and patient-friendly solutions supported by digital health ecosystems. Advances in glucagon formulations have transformed severe hypoglycemia management, moving away from multi-step reconstitution kits to ready-to-use, highly stable, and convenient options. Stable liquid glucagon formulations now remain usable at room temperature and can be delivered via autoinjectors or prefilled syringes, eliminating complicated preparation. These innovations reduce administration time, enhance ease of use for caregivers and emergency responders, and improve the likelihood of timely treatment during critical hypoglycemia events.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $466.5 Million |

| Forecast Value | $866.8 Million |

| CAGR | 6.5% |

The injectable segment held 52.4% share in 2025. Injectable glucagon provides a rapid onset of action, often within minutes, making it crucial in severe hypoglycemia scenarios to prevent seizures, unconsciousness, or long-term neurological damage. Injectable formulations offer flexibility in administration routes, including subcutaneous, intramuscular, and intravenous options, allowing tailored treatment across home, clinical, and hospital settings. This adaptability ensures the segment retains leadership by meeting diverse patient needs and urgent care requirements.

The hospital pharmacies segment contributed USD 222.1 million in 2025, ensuring continuous availability and safe handling of glucagon across emergency departments, inpatient wards, intensive care units, and diagnostic suites. Hospital pharmacists oversee the correct storage, preparation, and administration of glucagon, maintain its stability, and train nursing and support staff on proper emergency use. These environments also serve as critical educational hubs, emphasizing accurate dosage, administration steps, and post-treatment monitoring to ensure patient safety.

North America Glucagon Market held the largest share in 2025, driven by advanced healthcare infrastructure, high adoption of emergency diabetes therapies, and widespread use of ready-to-use glucagon formulations. Well-established hospital networks, pharmacy accessibility, and robust regulatory frameworks support rapid distribution and approval of innovative glucagon products. Hospital pharmacies maintain glucagon as a vital emergency medication, ensuring immediate access for severe hypoglycemia, preparation of pediatric doses, and use in diagnostic procedures. Retail and online pharmacies complement hospital distribution, providing convenient access to prescription glucagon for home use.

Prominent companies operating in the Global Glucagon Market include Amphastar Pharmaceuticals, Avalon Pharma, Eli Lilly and Company, Fresenius Kabi, Hanmi Pharmaceutical, Lupin Limited, Novo Nordisk A/S, Taj Pharmaceuticals, Xeris Biopharma Holdings, and Zealand Pharma. Companies in the Global Glucagon Market are strengthening their presence through multiple strategic approaches. Firms are investing in research and development to innovate stable, ready-to-use formulations and advanced autoinjector devices that improve ease of administration and patient compliance. Expanding distribution channels, including hospitals, retail, and online pharmacies, ensures broad product availability. Strategic collaborations with healthcare providers, emergency response networks, and patient advocacy organizations enhance education and awareness about timely hypoglycemia management. Regulatory engagement and fast-track approvals for innovative products help accelerate market entry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.5 Forecast model

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of diabetes worldwide

- 3.2.1.2 Technological advancements in glucagon delivery methods

- 3.2.1.3 Increasing research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of medications

- 3.2.2.2 Side effects associated with glucagon

- 3.2.3 Market opportunity

- 3.2.3.1 Growing adoption in emergency response systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Impact of AI and generative AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Injectable

- 5.3 Inhalation

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hypoglycemia

- 6.3 Diagnostic aid

- 6.4 Gastrointestinal disorders

- 6.5 Cardiogenic shock

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amphastar Pharmaceuticals

- 9.2 Avalon Pharma

- 9.3 Eli Lilly and Company

- 9.4 Fresenius Kabi

- 9.5 Hanmi Pharmaceutical

- 9.6 Lupin Limited

- 9.7 Novo Nordisk A/S

- 9.8 Taj Pharmaceuticals

- 9.9 Xeris Biopharma Holdings

- 9.10 Zealand Pharma

2026-2034年全球升糖素市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球升糖素市場規模、佔有率、趨勢和成長分析報告 升糖素市場規模、佔有率和成長分析(按適應症、給藥途徑、劑型、最終用戶和地區分類)-2026-2033年產業預測

升糖素市場規模、佔有率和成長分析(按適應症、給藥途徑、劑型、最終用戶和地區分類)-2026-2033年產業預測 全球GLP-1類似物市場

全球GLP-1類似物市場 GLP-1類比的全球市場:各適應症,各用途,各流通管道,各地區,機會,預測,2018年~2032年

GLP-1類比的全球市場:各適應症,各用途,各流通管道,各地區,機會,預測,2018年~2032年 GLP-1 市場:依分子類型、所用活性化合物、GLP-1 促效劑藥物類型、促效劑類型、給藥途徑、目標適應症和關鍵區域分:至2035年的行業趨勢和全球預測

GLP-1 市場:依分子類型、所用活性化合物、GLP-1 促效劑藥物類型、促效劑類型、給藥途徑、目標適應症和關鍵區域分:至2035年的行業趨勢和全球預測 GLP-1類比市場,規模,佔有率,趨勢,產業分析報告:各給藥途徑,各產品,各用途,各流通管道,各地區 - 市場預測,2025年~2034年

GLP-1類比市場,規模,佔有率,趨勢,產業分析報告:各給藥途徑,各產品,各用途,各流通管道,各地區 - 市場預測,2025年~2034年